Here is the honest answer: some credit changes show up in 30 to 60 days, and some take months to years – and nobody can promise you a specific number of points on a specific date. If you are buying a house in a few months, the fastest levers are paying down credit card balances and correcting a genuine reporting error; those can move a score within a billing cycle or two. Rebuilding after a bankruptcy, aging a late payment until it stops hurting, or simply building enough credit history are the slow ones – measured in months and years. The mortgage-specific shortcut that most buyers do not know about is a lender-ordered rapid rescore, which can capture a legitimate change in a matter of days once you are already in a loan. This guide sorts every common move into a realistic timeline and, more importantly, shows you how to fix the right things for a mortgage instead of guessing.

Last updated: June 30, 2026. All point ranges and timelines below are general and situational – confirm your current numbers with a licensed loan officer.

Why “how long” is the wrong first question

Before you spend a single month working on your credit, get the target right. The score you nurture on a free consumer app is usually a different model and a different number than the mortgage score a lender actually uses to price and qualify your loan. Chasing the wrong number can waste the exact weeks you do not have. The smartest first move is to have a mortgage broker pull your real tri-merge mortgage score early, so the plan you build targets the score that decides your approval – not a marketing number.

Once you know your true starting point, timing becomes a math problem instead of a guessing game. The Consumer Financial Protection Bureau (CFPB) and FICO both make the same core point: there is no quick, guaranteed fix, and how fast a change appears depends on when your creditors report and which lever you pull. FICO puts it plainly – there is no quick way to fix a credit score, and most people may start noticing small changes within three to six months of consistent good behavior. That is the baseline reality. The rest of this article is about which levers beat that baseline and which do not.

What actually moves your score – the five factors

Every credit action you take pushes on one of five factors. Knowing which factor you are touching tells you roughly how fast it can move. FICO weights them, in general, as payment history 35%, amounts owed (mostly credit utilization) 30%, length of credit history 15%, new credit 10%, and credit mix 10%. FICO is careful to note these are general weights for the overall population – the exact importance of each category can be different for different credit profiles.

Here is the useful reframe for a home buyer: two of these factors respond fast, and three of them barely move on a 30-to-60-day timeline. That single distinction is what separates a plan that works before closing from a plan that does not.

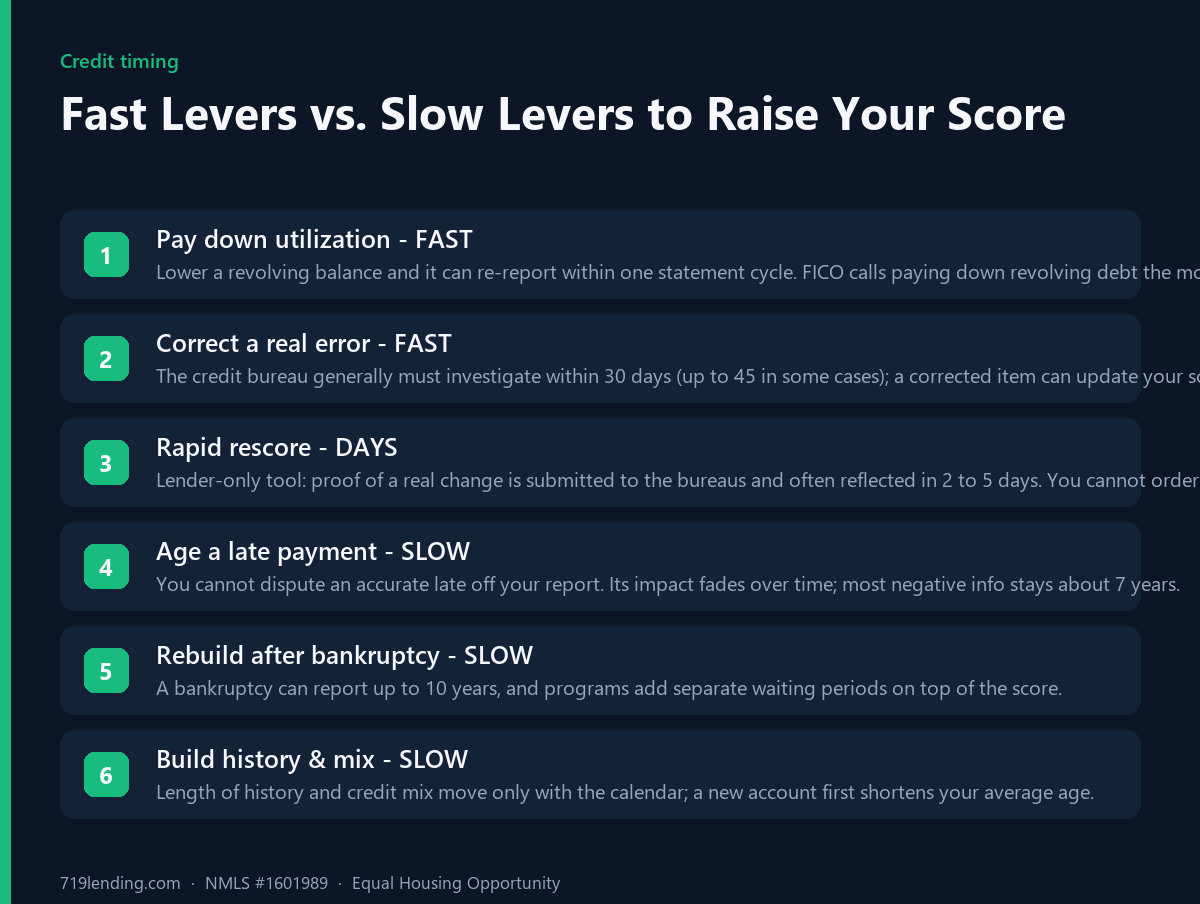

Amounts owed / utilization (30%) – FAST. Pay down a revolving balance and it can re-report within one statement cycle. FICO calls paying down revolving debt the most effective way to improve your credit scores in this area.

Payment history (35%) – MIXED. Correcting an error is fast; erasing the sting of a real late payment is slow. The line matters, so we split it below.

Length of history (15%), new credit (10%), credit mix (10%) – SLOW. These are aging problems. You cannot rush the calendar.

Fast levers vs. slow levers when raising your credit score before a mortgage. General – confirm current.

What moves fast: 30 to 60 days (sometimes days)

These are the levers worth pulling when you are already house-hunting or under contract.

Paying down credit card utilization. Utilization – your balances divided by your limits – is recalculated every time your card issuer reports a new balance, typically once a month around your statement date. Pay balances down and the lower number can show up on your next report. The CFPB’s general guidance is to keep your use of credit at no more than 30 percent of your total credit limit, and it confirms you don’t need to carry a balance on credit cards to get a good score. One nuance that trips up buyers: the balance that reports is usually the one on your statement date, not your due date – so paying before the statement closes is what lowers the reported number. Point gains here are real but situational; no one can promise you a set amount.

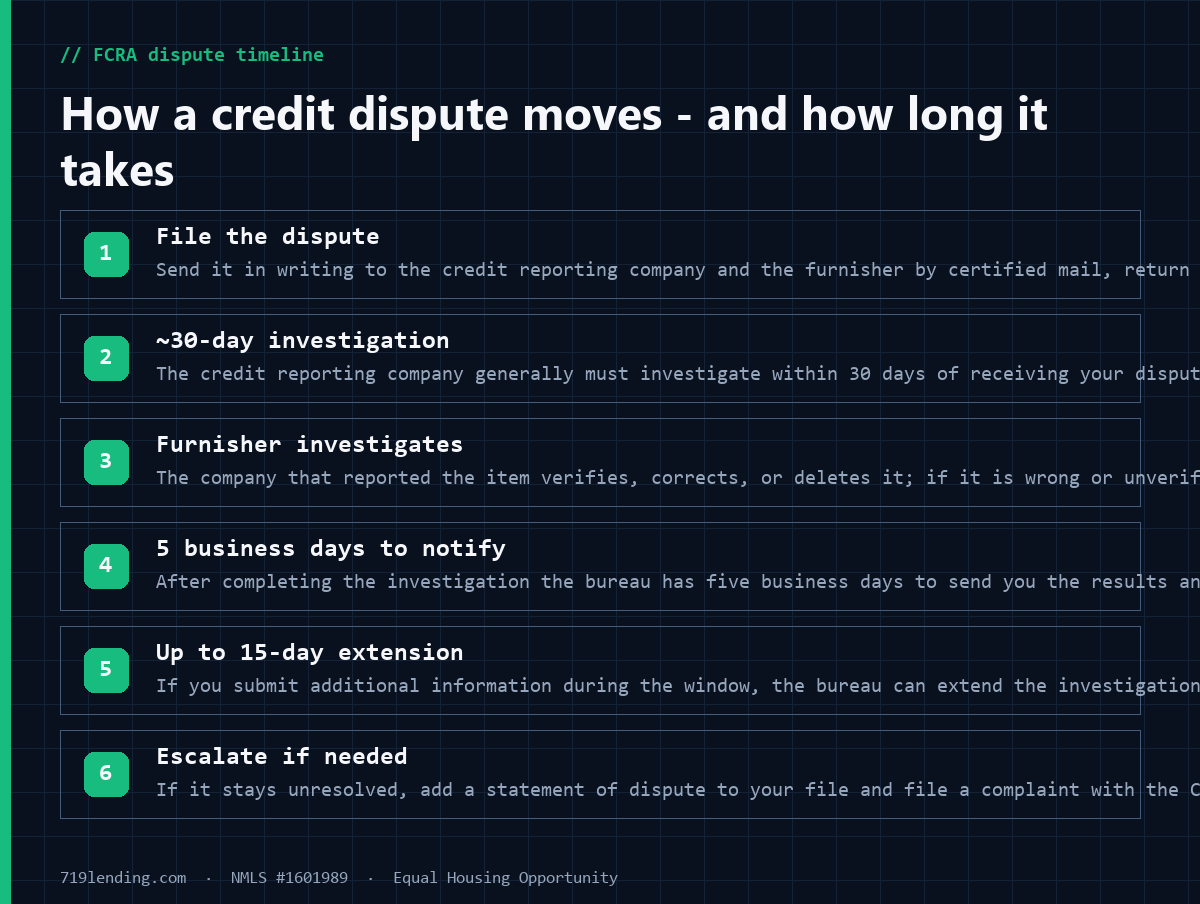

Correcting a genuine reporting error. If something on your report is factually wrong – a payment marked late that was on time, an account that is not yours, a balance that is inflated – disputing it can help quickly. By law the credit reporting company generally must investigate the dispute within 30 days of receiving it (up to 45 days in certain cases), and then has five business days after completing an investigation to notify you of the results. If the item is corrected or removed, your score can update as soon as the file changes.

Rapid rescore – the in-transaction shortcut. This is the mortgage-only tool. Once you are in a loan, your lender can order a rapid rescore: they submit proof of a recent change (like a paid-down card) directly to the bureaus, and the update is often completed within two to five days instead of the usual 30-to-60-day reporting lag. Two things to know: you cannot order it yourself – only your mortgage lender can – and the lender is not allowed to directly pass the fees it incurs to you. It also requires documented proof of a real change; it does not invent points. Rapid rescore is why the same paydown that would take a month on your own can count in days inside a transaction. Learn more in our guide to why your lender’s credit score is different.

What takes months to years (and cannot be rushed)

These are the levers that make “just fix it before closing” impossible. If any of these is your situation, the honest plan is to start early or adjust your timeline.

Aging a late payment. You cannot dispute an accurate late payment off your report. The CFPB is blunt: you generally cannot have negative information removed from your credit report if it is accurate, and most negative information will remain in your report for seven years. What helps is time – FICO notes the impact of past credit problems on your FICO Score fades as time passes and as recent good payment patterns appear. A fresh late costs the most and heals the slowest.

Rebuilding after a bankruptcy, foreclosure, or major derogatory. A bankruptcy can stay on your report for up to ten years, and rebuilding a score from that low point is a multi-month-to-multi-year project. On top of the score itself, mortgage programs impose separate waiting periods – a pure mortgage construct, covered in the next section.

Building credit history and mix. Length of history and credit mix are the definition of slow. A brand-new account actually shortens your average age at first. The CFPB frames it directly: credit scores are based largely on how you manage credit accounts over time. There is no 30-day version of “more history.”

For a fuller picture of what a lender needs to see, our pillar on what credit score you need to buy a house breaks down program minimums versus what actually gets approved.

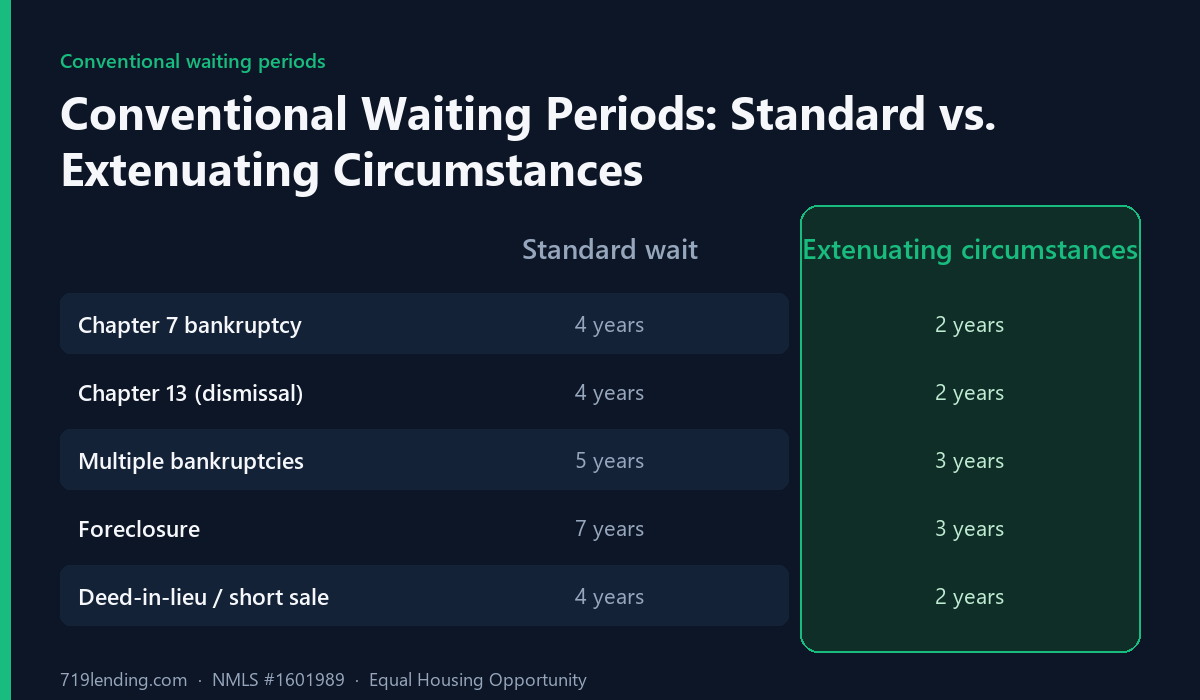

General conventional (Fannie Mae) waiting periods after major credit events, vs. the reduced period with documented extenuating circumstances. General – confirm current.

The mortgage timeline your score does not control: waiting periods

Even with a rebuilt score, a past bankruptcy or foreclosure comes with a required waiting period before a program will finance you. These are set by the loan programs, not your score, and they are the single biggest reason “raise my score fast” sometimes cannot solve the problem. Below are the general conventional (Fannie Mae) waiting periods, measured from the discharge, dismissal, or completion date; FHA is often shorter. These are general – confirm current with a licensed loan officer, because programs and exceptions change.

Event

Conventional standard wait

With documented extenuating circumstances

Chapter 7 bankruptcy

4 years from discharge/dismissal

2 years

Chapter 13 bankruptcy

2 years from discharge / 4 years from dismissal

2 years (from dismissal)

Multiple bankruptcies (in 7 yrs)

5 years from most recent

3 years

Foreclosure

7 years from completion

3 years

Deed-in-lieu / short sale

4 years from completion

2 years

For comparison, FHA generally allows a home purchase two years after a Chapter 7 discharge (and, with documented extenuating circumstances, as little as 12 months). That is why two borrowers with the same score can get two different answers – the program, not just the number, decides. If a derogatory is in your recent past, read our detailed guide on how long after bankruptcy you can buy a house and, if a traditional loan is off the table for now, our overview of non-QM lenders in Colorado.

A realistic plan by how much time you have

Match the lever to your calendar. Every figure below is general and situational – not a guarantee.

Under contract / weeks away: Pay down cards before the statement date and ask your lender about a rapid rescore. Do not open new accounts or make large purchases on credit – both can hurt at the worst moment.

2 to 3 months out: Pay down utilization, correct any genuine errors, and keep every payment on time. FICO’s “three to six months” window for noticeable change starts here.

6 to 12 months out: Add on-time history, keep old accounts open to preserve length, and avoid new debt. This is enough runway to fix a thin file or let a single old late fade in impact.

After a bankruptcy or foreclosure: Your gating factor is the waiting period, not the score. Rebuild clean credit during the wait so you are ready the day the clock runs out.

Whatever your window, the highest-leverage move is the same: get your real mortgage score pulled early. A number you get from a broker before you shop tells you which of these plans you are actually on. Compare our current Colorado Springs mortgage rates once you know where you stand, and if you are a first-time buyer, review Colorado first-time home buyer programs.

A word on credit-repair promises

If a company promises to raise your score by a fixed number of points, or to delete accurate, current negative items, be skeptical. The CFPB warns that anyone claiming to remove information from your credit report that is current, accurate, and negative is probably running a credit repair scam – because only the passage of time removes accurate items. Legitimate work is fixing genuine errors and paying down balances, both of which you or your lender can do. Inside a mortgage, your broker coordinates the timing – dispute cleanup, paydowns, and rapid rescore – so the right fixes land before your file is priced.

Frequently asked questions

How long does it take to raise your credit score to buy a house? It depends entirely on the lever. Paying down credit card balances or correcting a reporting error can show up in 30 to 60 days – or in days via a lender-ordered rapid rescore. Aging a late payment, rebuilding after bankruptcy, or building credit history takes months to years. FICO says most people notice small changes within three to six months of consistent effort. All timelines are general and situational.

What is the single fastest way to raise my score before a mortgage? Paying down revolving credit card balances is generally the most effective fast lever – FICO calls it the most effective way to improve your credit scores in the amounts-owed category. Pay before your statement closes so the lower balance reports, and ask your lender whether a rapid rescore can capture it in days.

Can I pay someone to remove accurate late payments quickly? No. The CFPB states you generally cannot have negative information removed from your credit report if it is accurate, and warns that firms promising to delete accurate, current, negative items are likely scams. Only time removes accurate items – most negative information falls off after seven years.

What is a rapid rescore and can I order one? A rapid rescore is a lender-ordered service that submits proof of a recent credit change to the bureaus and updates your report, often within two to five days. You cannot order it yourself – only your mortgage lender can – and the lender cannot directly charge you for it. It requires documented proof of a real change; it does not create points out of nothing.

How long after a bankruptcy or foreclosure can I buy a house? Beyond rebuilding your score, programs set waiting periods. Conventionally, that is generally four years after a Chapter 7 discharge (two with documented extenuating circumstances) and seven years after a foreclosure (three with extenuating circumstances). FHA is often shorter – generally two years after a Chapter 7 discharge. These are general – confirm current with a loan officer.

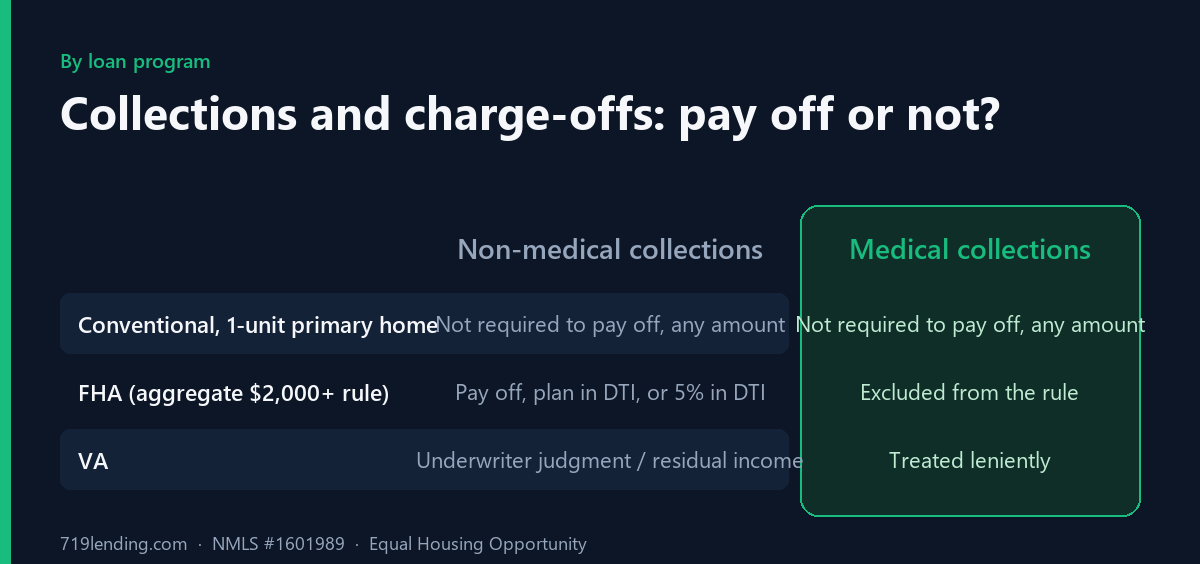

Does paying off a collection instantly raise my score? Not necessarily, and it can even backfire by re-aging the debt. Whether to pay a collection before a mortgage depends heavily on your loan program, so coordinate it with your loan officer rather than paying blindly. The safest move is to get your mortgage score pulled first and build the plan around it.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, endorsed by, or acting on behalf of any government agency, including FHA, VA, USDA, or CHFA. This article is educational and not a commitment to lend or a guarantee of any credit score change, approval, rate, or timeline. All score ranges, point estimates, and waiting periods are general – confirm current figures with a licensed loan officer. Program guidelines and credit-scoring outcomes vary by individual profile and are subject to change.

Can you get a mortgage with collections, charge-offs, or medical debt? Usually yes, often without paying them off. Here is how the answer changes by loan program, plus the paying-a-collection trap to avoid. General - confirm current.

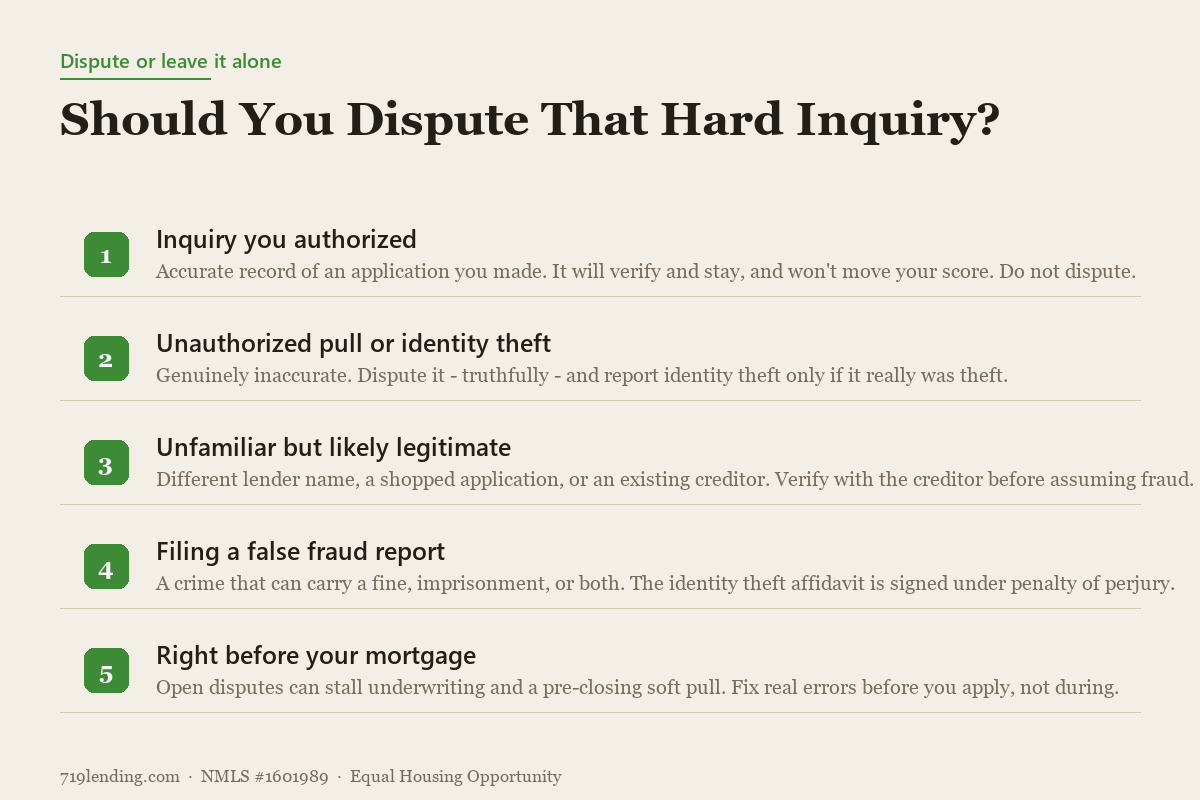

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.