A rapid rescore is a mortgage-only tool your lender can use to push a real, already-completed credit change — like a paid-down credit card or a corrected reporting error — to the credit bureaus in roughly two to five business days, instead of waiting a full billing cycle for the update to show up on its own. It does not invent points or delete accurate information. It simply re-pulls your credit after a genuine change so your mortgage file reflects reality faster. And here is the part most borrowers never hear: you cannot buy a rapid rescore yourself — only a lender or broker can order one through the credit vendor. That makes it one of the few credit levers that lives entirely inside the loan transaction.

Below we break down what a rapid rescore actually does, why the timing matters when you are under contract, and how it pairs with a smart utilization paydown or a dispute cleanup to potentially move you across a pricing tier. Ranges here are general — confirm current figures with your loan officer.

A rapid rescore is a lender-only process, not a FICO product. It reflects only real, documented changes – it cannot invent points or remove accurate information. Timing is general – confirm current.

What a rapid rescore actually is

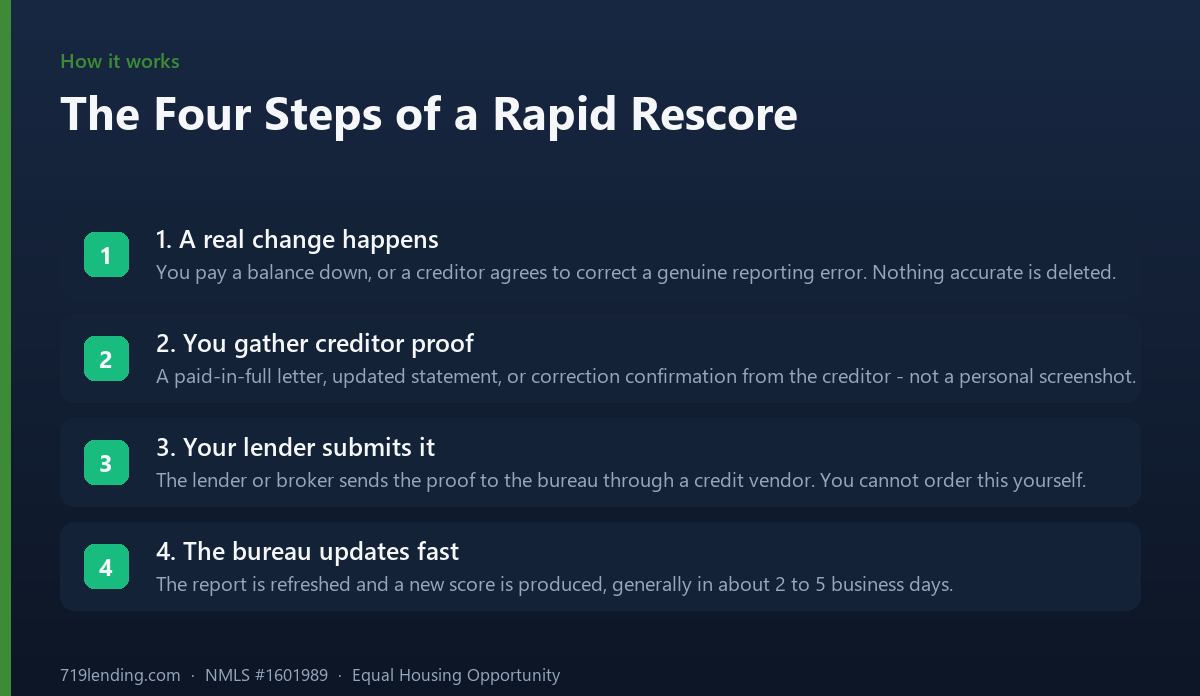

When you pay down a credit card or a creditor corrects an error, that change does not hit your credit report instantly. Creditors typically report to the bureaus on their own monthly cycle, so a payment you made today might not show up for 30 days or more — long after your rate lock or closing date. A rapid rescore compresses that wait.

Here is the mechanism. You make a real change (pay a balance down, or a furnisher agrees to fix inaccurate data). You give your lender documented proof from the creditor — a paid-in-full letter, an updated statement, or a correction confirmation. Your lender submits that proof to the credit reporting agency through a specialized credit vendor, and the bureau updates your file and produces a fresh score, usually within about 2 to 5 business days. The Consumer Financial Protection Bureau describes it plainly: it is “a pay-to-play service where mortgage loan officers can, for an extra fee, get consumer credit files reviewed and updated quickly.”

Notice what is not happening. There is no negotiation over what your score “should” be. Nothing accurate is being erased. The rapid rescore only reflects a change that has genuinely already occurred — it just gets that change on the record in days rather than weeks.

Why only a lender can order a rapid rescore

This is the single most important thing to understand: a consumer cannot buy a rapid rescore. It is not a product you can order from Equifax, Experian, or TransUnion directly, and it is not something a credit-repair company can legitimately sell you. It is a service that flows through a mortgage lender or broker and their credit vendor.

That is also why it is a genuine differentiator. Most credit advice you read is written for consumers doing it alone, on the bureaus’ timeline. A rapid rescore is a lever a borrower literally cannot pull on their own — it only exists because you are inside a live mortgage. When you work with a broker who knows how to time it, a paydown that would otherwise take a full cycle to register can be reflected before your file goes to underwriting.

One more consumer protection worth knowing: under the Fair Credit Reporting Act, you have a legal right to dispute credit-report errors yourself for free, and you never have to pay a credit-repair company to do it for you. The rescore vendor still charges a fee for the speed — the CFPB notes it can run roughly $25 to $40 per credit file, per credit reporting company. How that cost is handled varies by lender, so ask your loan officer directly before you assume you will owe it.

A rapid rescore does not change what gets reported; it changes how fast a real, already-completed change reaches your mortgage file. Timing figures are general – confirm current.

Rapid rescore vs. waiting for the normal cycle

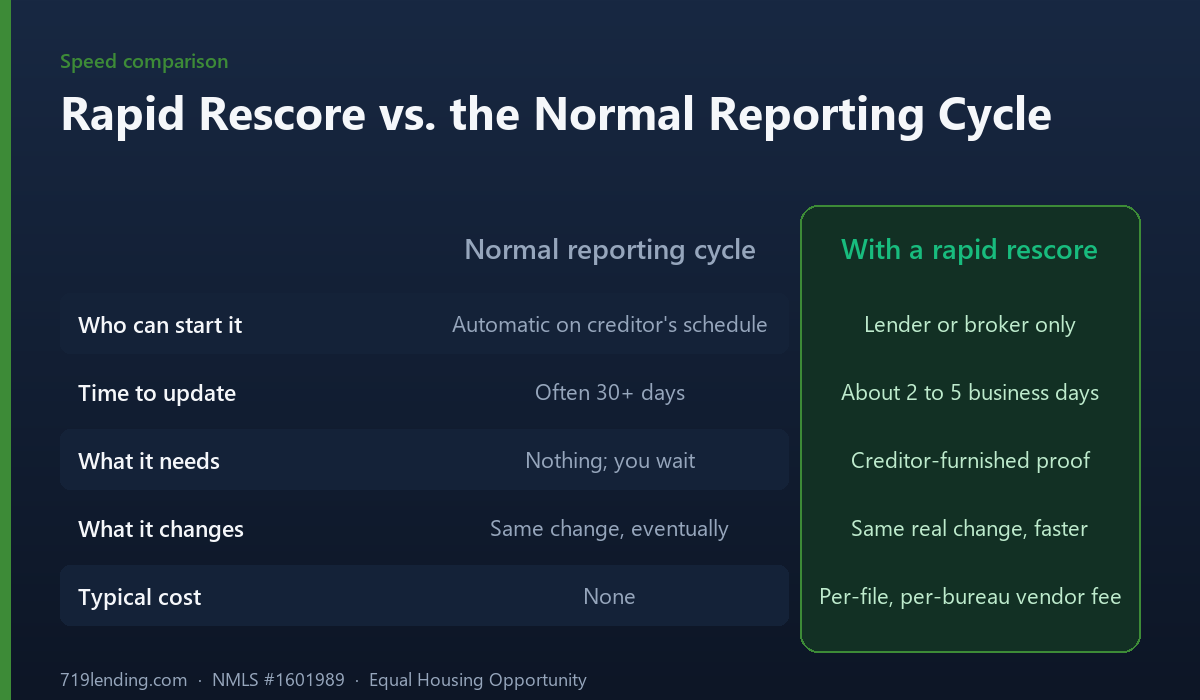

The whole value of a rapid rescore is speed, and the contrast is easiest to see side by side.

What happens

Normal reporting cycle

With a rapid rescore

Who can start it

Automatic — the creditor reports on its own schedule

Lender or broker only (you cannot order it)

Time to update

Often 30 days or more until the next report date

About 2 to 5 business days

What it needs

Nothing — you wait

Creditor-furnished proof of a real change

What it changes

Reflects the change eventually

Reflects the same real change, just faster

Typical cost

None

A per-file, per-bureau vendor fee

If you are not under contract and have months to spare, the free route is to simply pay the balance and wait. The rescore earns its keep when the clock matters — a rate lock expiring, a closing date approaching, or a score sitting just below a pricing threshold.

What a rapid rescore is not: it is not a FICO product

A rapid rescore does not “boost” your score, and it is not a shortcut FICO or the bureaus offer as a scoring gimmick. It is a lender process for pushing already-true information through faster. The score that comes out the other side is calculated by the same scoring model on the same rules — the only thing that changed is that your report now shows the paydown or the correction you already made.

It also cannot remove accurate, negative information. A legitimate late payment, an accurate collection, or a real charge-off will not vanish through a rescore, because there is nothing to correct — the data is true. Anyone promising to delete accurate, recent items is not describing a rapid rescore; they are describing something you should walk away from. A rescore only captures changes that are real: a balance that genuinely came down, or an error a furnisher genuinely agreed to fix.

Pairing a rescore with a utilization paydown

Rapid rescore is the delivery mechanism; a smart paydown is the change worth delivering. Credit utilization — how much of your available revolving credit you are using — is one of the fastest-moving factors in a credit score, and it is recalculated with each new balance the bureaus receive. Pay balances down and get the lower numbers reported, and the utilization portion of your score can respond quickly.

The catch outside a mortgage is timing: the balance that gets reported is usually the one on your statement closing date, not what you owe after you pay. So a paydown made mid-cycle might not show up until the next statement posts. Inside a live loan, a rapid rescore removes that waiting game — you pay the balance, document it, and your lender pushes the lower utilization through in days. A few practical notes:

Spread a limited paydown to drop the most individual cards under their thresholds, rather than dumping everything onto one big balance — both per-card and overall utilization are scored.

Get creditor-furnished proof of the new balances; a screenshot of your own banking app generally will not satisfy the bureau — it needs documentation from the creditor.

Coordinate with your loan officer before you move money, so the paydown lines up with when the lender re-pulls credit.

Pairing a rescore with a dispute cleanup

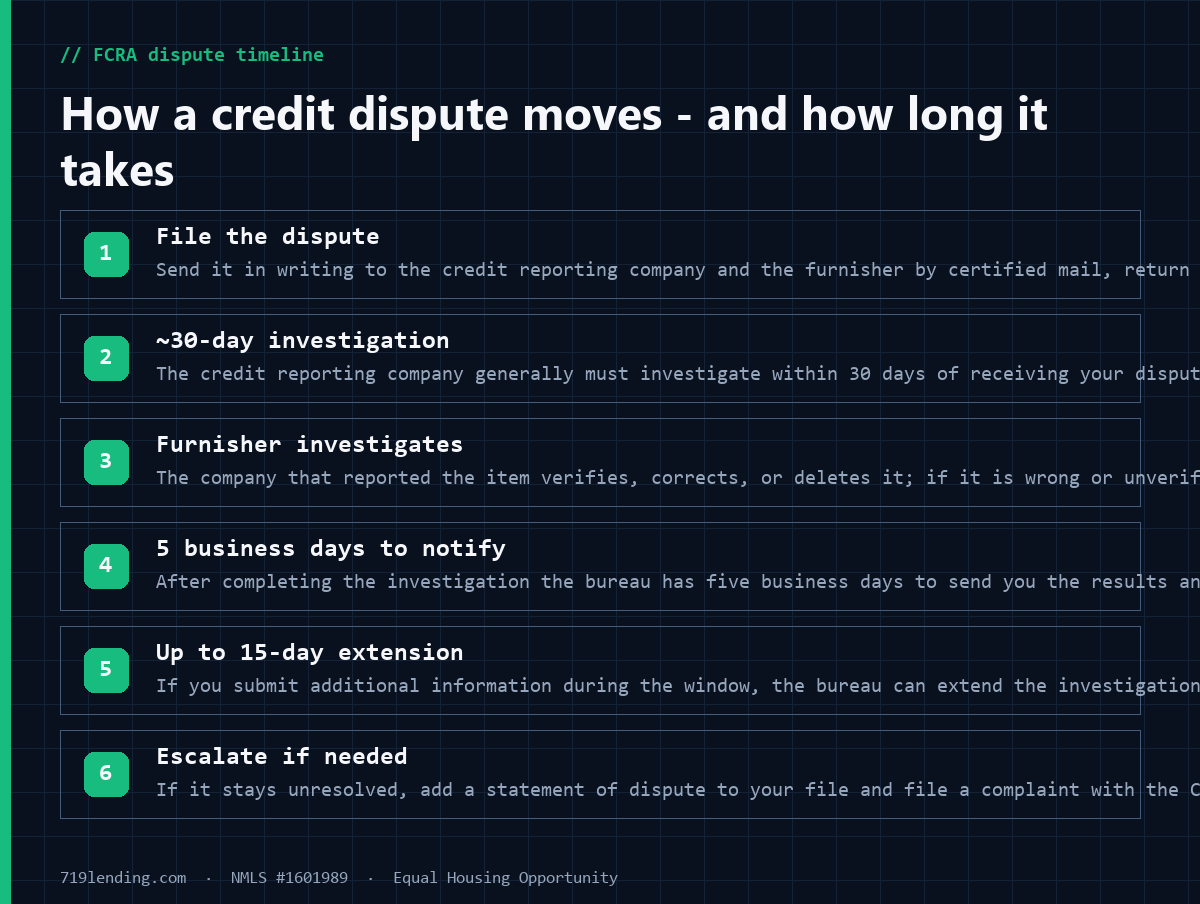

The other change a rescore can deliver fast is a corrected error. If your report shows something genuinely inaccurate — a balance that is wrong, an account that is not yours, a payment marked late that was on time — the standard fix is slow. The CFPB explains that when you dispute an error, the credit reporting company “generally must investigate the dispute within 30 days,” and that window can stretch to 45 days in some cases. That is the reinvestigation the FCRA requires, and it runs on its own statutory timeline regardless of your closing date.

A rapid rescore works differently. It does not replace the dispute investigation — it captures the result once a furnisher has already agreed the information was wrong and corrected it. As the CFPB puts it, if an investigation shows the furnisher provided wrong information, “the furnisher must update or remove the information and notify all the credit reporting companies after correcting it.” Once that correction exists and you have proof of it, a rescore gets it onto your mortgage file in days instead of waiting for the correction to propagate on its own. The sequence matters: verify the error is genuine and get it corrected first, then rescore to capture it.

How crossing a pricing tier can lower your rate or PMI

Here is where a few points can matter far more than they seem to. Mortgage pricing is tiered: lenders price loans by risk, and your credit score falls into a band. Fannie Mae assesses loan-level price adjustments — LLPAs — based on what its Selling Guide calls the “representative credit score for the loan.” Those adjustments generally move in bands (for example, 760+, 740–759, 720–739, and so on), so a score sitting just below a boundary can be paying for the tier below it.

That is why crossing a boundary — not just “looking better” — is the real prize. If a documented paydown lifts your representative score from, say, 738 to 740, or from 718 to 720, and a rapid rescore gets that across before your file is priced, you may land in a better pricing tier. That can translate to a lower interest rate or reduced mortgage insurance cost over the life of the loan. Two important guardrails: no one can promise a specific point gain or a specific tier jump — it depends entirely on your file — and for conventional loans with more than one borrower, the representative credit score used for pricing is the lowest of the borrowers’ qualifying scores, so a rescore on the right borrower is what counts.

Score is only half the equation, too. Paying a revolving balance down also lowers the monthly obligation that feeds your debt-to-income ratio, which is the co-equal qualifier alongside your score. A good broker looks at both when deciding whether a rescore is worth ordering.

When a rapid rescore makes sense — and when it does not

A rescore is a precision tool, not a cure-all. It shines when there is a real, documentable change and a deadline. It does nothing when the underlying problem is time.

Good fit: you paid a card down and need the lower balance reflected before pricing; a furnisher corrected a genuine error and you need it captured before underwriting; your score is a hair under a pricing tier and a documented change could cross it.

Poor fit: you are trying to remove an accurate late payment or a legitimate collection (a rescore cannot do that); you have months before you buy (the free waiting route works fine); the change has not actually happened yet or you have no creditor-furnished proof.

The move that ties it together is talking to your loan officerbefore you make changes, not after. Timing a paydown or a correction to the lender’s credit pull is the difference between a rescore that helps and money spent on one that changes nothing.

Frequently asked questions

Can I order a rapid rescore myself? No. A rapid rescore is available only through a mortgage lender or broker and their credit vendor. Consumers cannot buy one directly from Equifax, Experian, or TransUnion, and a legitimate credit-repair company cannot sell you one either.

How long does a rapid rescore take? Generally about two to five business days once your lender submits creditor-furnished proof of the change to the credit reporting agency — far faster than the 30-plus days a normal reporting cycle can take. This range is general; confirm current timing with your loan officer.

Does a rapid rescore boost or fabricate my score? No. It only re-pulls your credit after a real change — a paid-down balance or a corrected error — that has already happened. It does not create points out of nothing and cannot remove accurate information.

Can a rapid rescore delete a legitimate late payment or collection? No. If the information is accurate, there is nothing to correct, so a rescore will not remove it. Only genuine errors that a furnisher agrees to fix can be captured by a rescore. Be cautious of anyone promising to erase accurate, recent items.

Will a rescore lower my mortgage rate? It might, if a documented change lifts your representative score across a pricing-tier boundary before your loan is priced — because Fannie Mae assesses loan-level price adjustments based on that score. No one can promise a specific point gain or rate, and results depend entirely on your file. Ranges here are general — confirm current.

Do I have to pay for a rapid rescore? The vendor charges a per-file, per-bureau fee — the CFPB notes roughly $25 to $40 per credit file, per credit reporting company. Under the Fair Credit Reporting Act you always have the right to dispute credit-report errors yourself for free, so you should never pay simply to correct an error; how the rescore fee itself is handled varies by lender, so ask your loan officer.

Last updated: June 30, 2026. 719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by any government agency, including FHA, VA, USDA, or CHFA. Credit-score, timeline, fee, and pricing figures above are general and illustrative — confirm current details for your situation. Nothing here promises a specific credit-score change, loan approval, interest rate, or pricing outcome. Rapid rescore is a lender process, not a FICO product, and reflects only real, documented credit changes.

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.