You have a federal right to dispute inaccurate information on your credit report, and the credit reporting company generally has about 30 days to investigate. But here is the mortgage twist most people miss: an active “consumer disputes this account” remark on a tradeline can cause the automated systems that underwrite loans to set that account aside, which can stall or complicate your file until the dispute is resolved. So the smart move is to clean up genuine errors well before you apply, not in the middle of escrow.

This guide walks through your rights under the Fair Credit Reporting Act (FCRA), how the reinvestigation actually works, how to document a dispute so it sticks, and the part almost no consumer article covers: why timing a dispute wrong can backfire on a mortgage.

Last updated: June 30, 2026. Figures and program rules are general – confirm current guidance with your loan officer.

Your right to dispute inaccurate information

Under the FCRA, if you spot information on your credit report that is inaccurate or incomplete, you have the right to dispute it, and the credit reporting company must investigate. This is not a favor; it is the law. The Consumer Financial Protection Bureau and the Federal Trade Commission both publish plain-language guidance on how to do it, and both stress the same core steps.

Common errors worth disputing include:

An account that is not yours, often a sign of mixed files or identity theft

A payment reported late that you actually paid on time

A balance or credit limit that is wrong

An account still showing open that you closed, or a debt reported twice

A discharged or paid item still reported as owed

Outdated negative information that should have aged off

One important limit: you can only dispute information that is genuinely inaccurate or incomplete. An accurate, recent late payment cannot be “disputed off” – the furnisher will simply verify it and it stays. Any company promising to delete accurate items is selling you a fantasy.

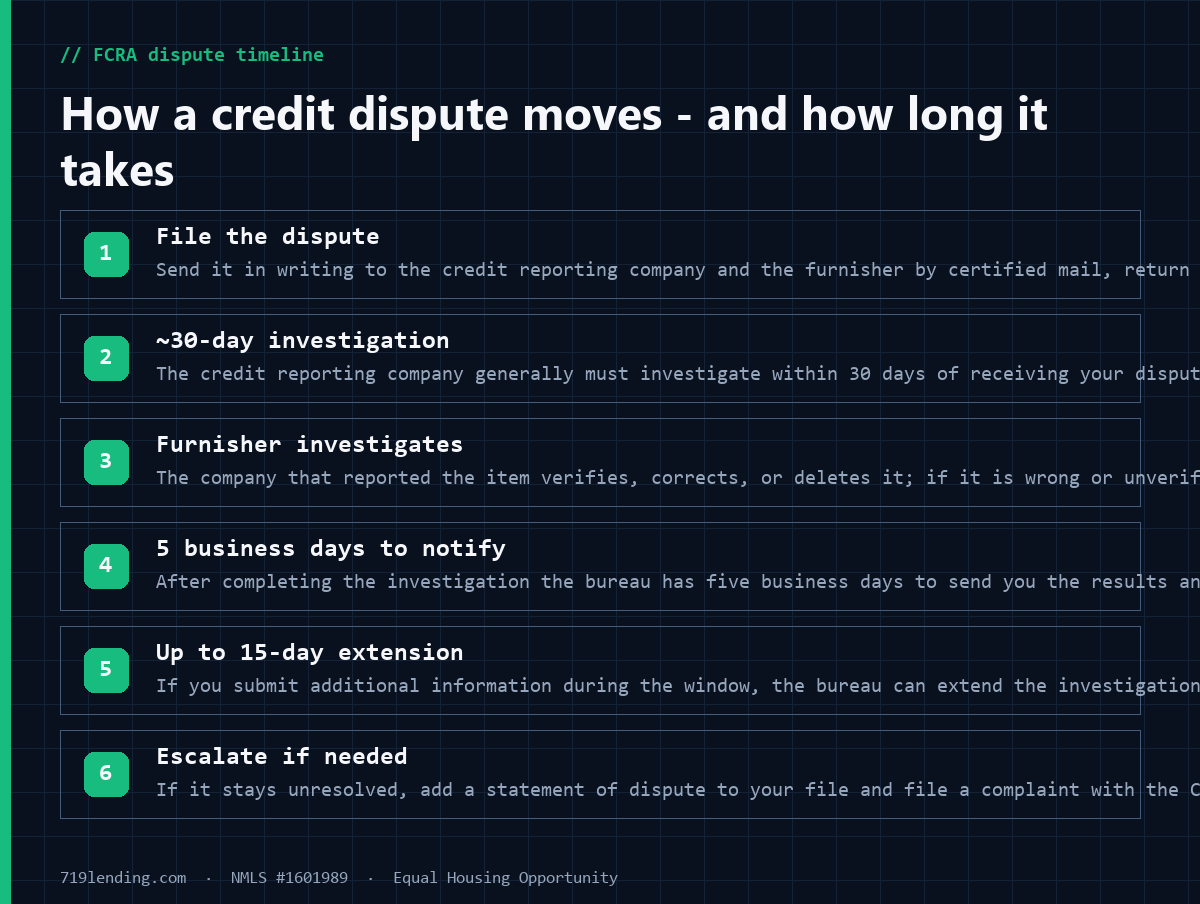

The FCRA dispute timeline: the bureau generally has 30 days to investigate, five business days to notify you, and up to 15 extra days if you add information. Source: CFPB.

How the reinvestigation works and the ~30-day timeline

The bureau forwards your dispute and supporting documents to the company that furnished the information, known as the furnisher.

The furnisher investigates and reports back. If it finds the information was wrong or cannot be verified, it must correct or delete it and notify the bureaus it reported to.

The bureau has five business days after completing the investigation to send you the results, along with a free copy of your updated report if anything changed.

If you submit additional relevant information during the investigation, the bureau can extend it by 15 days, so a dispute can take up to 45 days total. (Disputes filed after you pull your free annual report also carry the 45-day window.) Bottom line: plan on a full month or more, which is exactly why disputes belong on your calendar before you shop for a home, not after you are under contract.

How to document a dispute so it actually sticks

Both the CFPB and FTC recommend disputing in two places, not one: with the credit reporting company and with the business that supplied the information. Doing both puts the furnisher on notice directly and strengthens your paper trail.

To document it properly:

Put it in writing. Explain what is wrong, why, and identify each item by account number, along with your full name, address, and phone number.

Include a marked-up report. Attach the portion of your credit report with the disputed items circled or highlighted.

Attach copies, not originals. Send copies of documents that prove your case, such as statements, canceled checks, or payoff letters, and keep the originals.

Send it by certified mail, return receipt requested. This proves the bureau and furnisher received it and gives you a dated record.

Keep copies of everything – your letter, your enclosures, and the responses you get back.

The FTC publishes free sample dispute letters for both the bureau and the furnisher, so you do not have to write one from scratch. If the investigation does not resolve in your favor and you still believe the item is wrong, you can add a brief statement of dispute to your file and escalate a complaint to the CFPB.

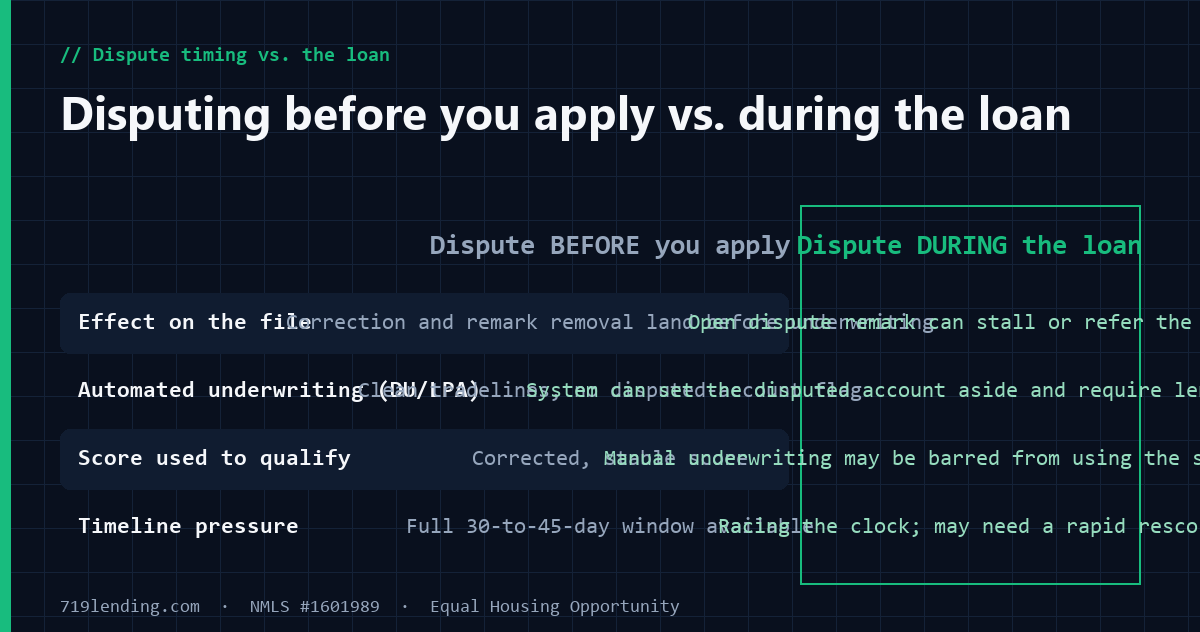

The dispute remark that can stall your mortgage

Here is the differentiator, and it is the reason timing matters so much. When a tradeline carries an active “consumer disputes this account” remark, it does not just sit there quietly – it can change how your mortgage is underwritten.

Most conventional loans run through an automated underwriting system: Fannie Mae’s Desktop Underwriter (DU) or Freddie Mac’s Loan Product Advisor. Per Fannie Mae’s Selling Guide, when the report contains a disputed tradeline, DU first assesses the loan including the disputed account. If it can approve the file that way, no further action is needed. But if it cannot approve with the disputed tradeline included, DU re-assesses the risk without that account, and then flags that the lender must investigate the tradeline to confirm whether the borrower is responsible and whether the information is accurate.

That extra step is where files can stall. The lender may have to obtain a written explanation from you, gather documentation, and, if the disputed information turns out to be accurate and yours, get the dispute remark removed and the file re-scored before the loan can move forward. Under Fannie Mae’s guidance, if the account is accurate and you are responsible for it, the loan is not eligible for delivery as a DU loan until the dispute status is resolved. In practice, that can mean days of delay at the worst possible moment.

It gets sharper on manual underwriting. Fannie Mae’s guide is explicit: if the borrower has disputed information, the credit reporting company confirms the disputed information is inaccurate or incomplete, and underwriting has to be completed before the credit file can be corrected, the lender cannot use the credit score when manually underwriting the loan. Instead, the credit risk assessment must be based on a review of the borrower’s traditional credit history. A single stray dispute remark can knock your score out of the equation entirely.

Important caveats, because this is investor- and system-specific:

This is a “can,” not an “always.” Whether a disputed tradeline trips the file depends on the AUS result, the loan program, and individual lender overlays.

Disputed medical tradelines are treated differently. Fannie Mae does not include disputed medical debt in the disputed-tradeline message, and lenders are not required to investigate it.

Freddie Mac’s Loan Product Advisor has its own handling, but the practical takeaway is the same across both: an open dispute can complicate the file.

Timing a dispute against a mortgage: cleaning up errors before you apply protects the file; an open dispute mid-process can complicate automated underwriting. General – confirm current with your loan officer.

Why timing is everything: clean up before you apply

Put the two halves together and the strategy is obvious. A legitimate dispute is a good thing – fixing a real error can lift your score and clear a wrongful black mark. But the dispute process takes about a month, and an open dispute remark can set off the underwriting stall above. So:

Dispute genuine errors early – ideally two to three months before you plan to apply, so both the correction and the remark removal have time to land.

Do not open new disputes mid-process. A dispute filed after your application, or one still active when the lender pulls credit, can convert a clean approval into a conditioned or referred file.

If a stray dispute remark is already on an accurate account, tell your loan officer. Often the fix is to contact the furnisher, confirm you no longer dispute the item, have the remark removed, and re-pull.

Never dispute accurate items to “buy time” or inflate a score. During an investigation a disputed negative can drop out of scoring temporarily, but lenders and the underwriting systems are built to catch exactly that, and it can leave your qualifying score artificially unstable.

The mortgage fast lane: rapid rescore

What if a genuine error surfaces after you are already in the loan and there is no time for the full 30-to-45-day cycle? That is what rapid rescore is for. When a creditor furnishes proof that an item has been corrected – a paid-down balance, a removed dispute remark, a mis-coded account fixed – your lender can push that update through the bureaus in a matter of days rather than weeks. It is a lender-ordered tool, not something you can request yourself, and it only works once the creditor confirms the change. Paired with a well-timed correction, it is how a fixed error becomes an updated score before your rate lock expires. See our guide on the days-not-weeks rapid rescore process for how it works.

How this connects to the rest of your credit picture

How long does a credit report dispute take? The credit reporting company generally must investigate within 30 days of receiving your dispute, then has five business days to notify you of the results. If you submit additional information during the investigation, the window can extend by 15 days, for up to 45 days total. Plan accordingly and dispute well before you apply for a mortgage.

Can disputing an error hurt my mortgage application? The dispute itself does not lower your score, but an active dispute remark on a tradeline can affect underwriting. Automated systems like Fannie Mae’s Desktop Underwriter can set a disputed account aside and require the lender to investigate, which can stall the file. That is why it is generally best to resolve disputes before you apply, not during the loan.

Should I dispute accurate late payments to remove them? No. You can only dispute information that is genuinely inaccurate or incomplete. An accurate, recent late payment will simply be verified and remain on your report. Disputing accurate items to inflate a score can also destabilize your qualifying number during underwriting.

Do I have to dispute with both the credit bureau and the creditor? The CFPB and FTC recommend disputing in both places. File with the credit reporting company (Equifax, Experian, or TransUnion) and separately with the business that furnished the information. Send both by certified mail and keep copies of everything.

What happens if the disputed information is verified as correct? If the furnisher confirms the item is accurate, it stays on your report. If the account is accurate and yours but still carries a dispute remark, your lender may need that remark removed and the file re-scored before the loan can proceed. Contact the furnisher to confirm you no longer dispute the item.

Can a corrected error be updated in time for closing? Sometimes. Once a creditor furnishes proof of a correction, your lender can order a rapid rescore to update the bureaus in days rather than the full 30-to-45-day cycle. It is a lender-ordered tool and requires creditor-confirmed proof of the change.

719 Lending, NMLS #1601989. Equal Housing Opportunity. This article is for general educational purposes and is not credit-repair, legal, or financial advice; program rules, timelines, and figures are general and subject to change – confirm current details with your loan officer. 719 Lending is not affiliated with, and this content is not endorsed by, any government agency.

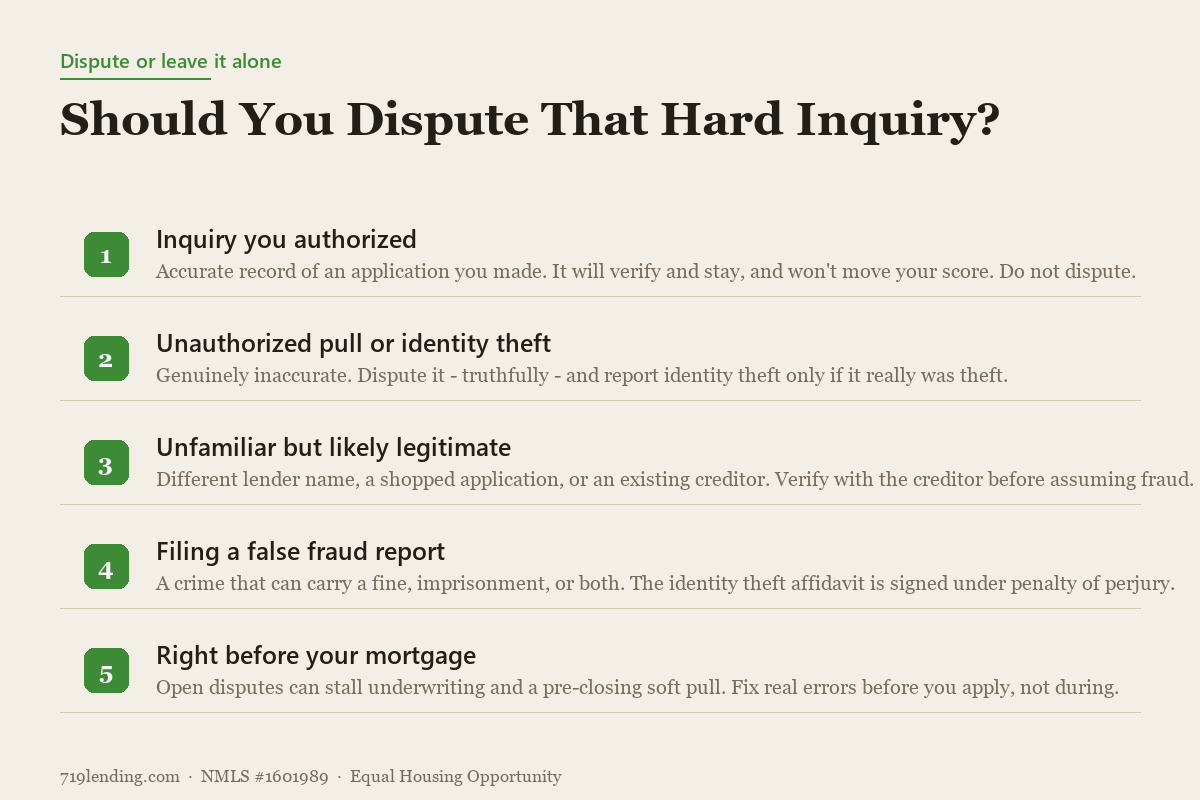

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.

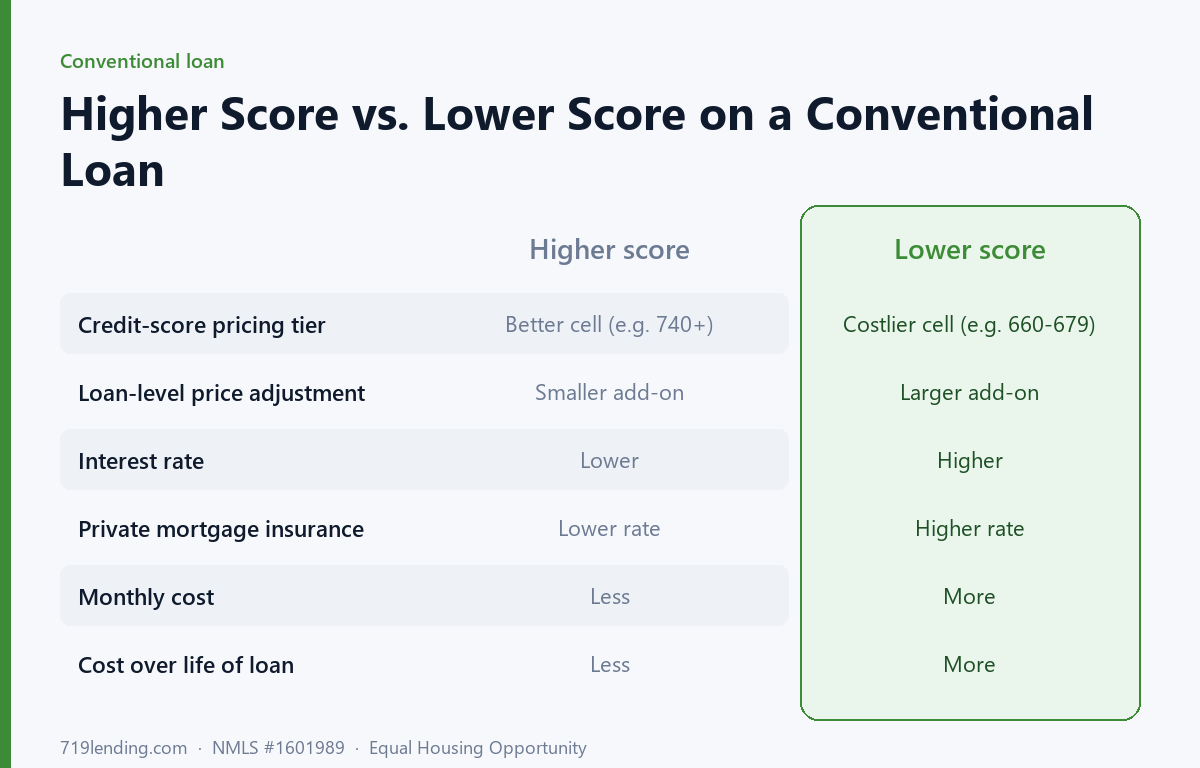

Does credit score affect mortgage rate? Yes - on conventional loans it moves your rate and PMI through credit-score pricing tiers. Here is how the bands work.