Short answer: only dispute a hard inquiry you truly did not authorize. If you applied for that credit – or gave a company permission to pull your report – disputing the inquiry almost never raises your score, can spark a fraud investigation against a legitimate creditor, and can complicate the exact credit pull your mortgage depends on. Right before you apply for a home loan, a dispute spree is one of the fastest ways to freeze your file mid-process.

This is one of those pieces of internet advice that sounds harmless and is anything but. “Just dispute all your hard inquiries and watch your score jump” gets repeated constantly. For a mortgage borrower, following it can cost you far more than the couple of points an inquiry was ever worth.

Let’s separate what a hard inquiry actually is, what disputing one does (and doesn’t) accomplish, when a dispute is genuinely appropriate, and why timing matters enormously when you are buying a house. This post is about inquiries specifically – disputing an actual reporting error on an account (a wrong balance, a late that was never late) is a different process, and we cover that separately in our post on how to read your mortgage credit report.

FICO’s own numbers on hard inquiries. General – confirm current.

What a hard inquiry actually is

A hard inquiry (also called a “hard pull”) is the footprint left when you apply for credit and a lender checks your report to make a lending decision – a mortgage pre-approval, an auto loan, a new credit card, a personal loan. It stays on your report, visible to future lenders, as a record that you sought new credit.

Two things are worth knowing up front, both straight from FICO:

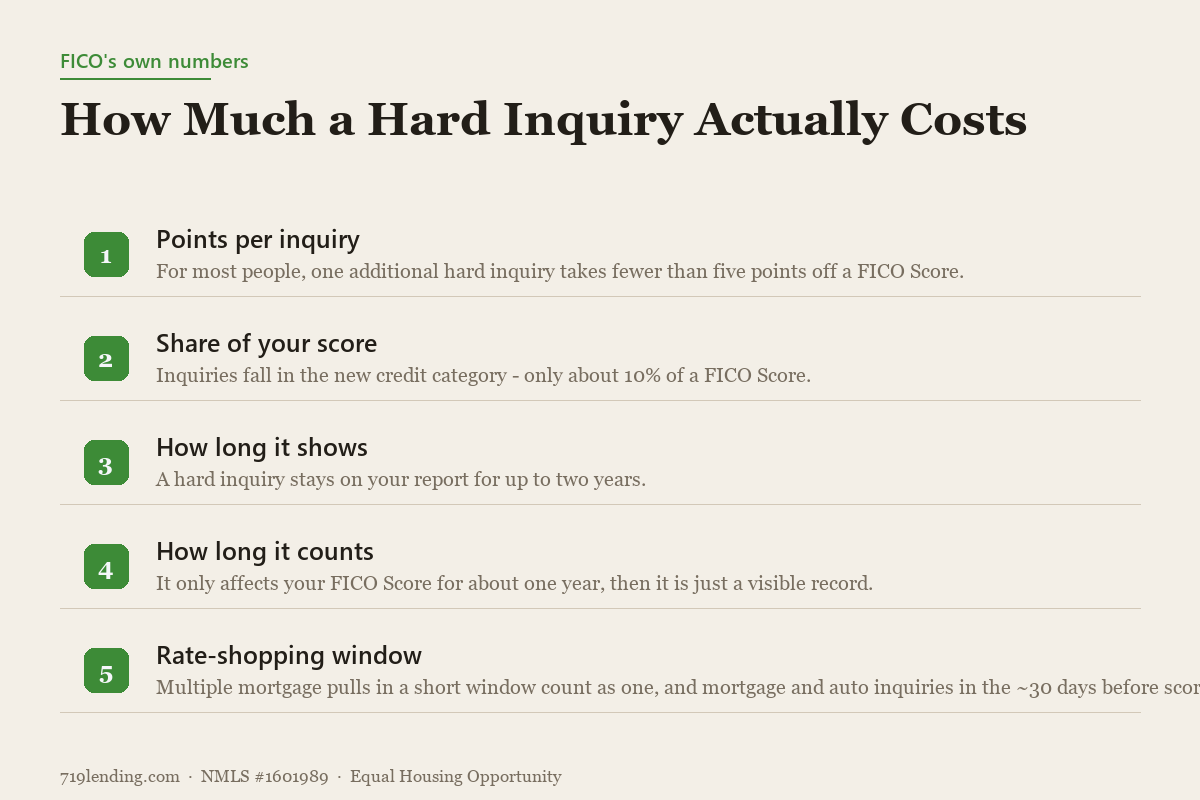

The impact is small. For most people, one additional hard inquiry takes fewer than five points off a FICO Score – inquiries are part of the “new credit” category, which is only about 10% of your score. There is no such thing as a 40-point inquiry (general – confirm current).

The impact fades fast. A hard inquiry stays on your report for up to two years, but it only affects your FICO Score for about one year. After that first year it is just a visible record, not a scoring factor.

Checking your own credit is a soft inquiry – it does not affect your score at all and is not what this post is about. Soft pulls also cover things like pre-screened offers and, importantly for mortgage borrowers, the final credit refresh a lender runs before closing (more on that below).

Why disputing an inquiry you authorized usually backfires

Here is the crux. The dispute process under the Fair Credit Reporting Act (FCRA) exists to correct inaccurate information. A hard inquiry that resulted from an application you actually submitted is not inaccurate – it is a true record of something that happened. A legitimate, authorized inquiry will not be removed just because you dispute it, and disputing a genuine inquiry will likely not change your score at all.

So in the best case, you spend effort disputing something that does not move and does not come off. In the worse cases:

You may trigger a fraud investigation against a legitimate creditor. When you dispute an inquiry as “unauthorized,” you are effectively telling the bureau that a company pulled your credit without permission – or that someone applied for credit in your name. That is a fraud claim. If the pull was legitimate, you have set off an investigation into a business that did nothing wrong, and the item stays anyway once verified.

Escalating to a false identity theft report is a crime. Credit-repair schemes have pushed borrowers to file identity theft reports to “explain away” accurate items – and it is not a gray area. The FTC warned in January 2026 that filing a false identity theft report “may leave you worse off – and it’s a crime that could get you a fine, imprisonment, or both.” The report you sign at IdentityTheft.gov is a federal affidavit signed under penalty of perjury.

This is not hypothetical. In 2022, federal courts halted two large credit-repair operations that had filed thousands of false identity theft reports – often without their own customers’ knowledge – to strip accurate negative items and inquiries off reports. The takeaway from every regulator: disputing accurate information as fraud is not a life hack, it is a liability.

When disputing a hard inquiry is appropriate – and when it backfires. General guidance; confirm current.

When you should dispute a hard inquiry

There is exactly one situation where disputing a hard inquiry is the right move: you genuinely did not authorize it. That usually means one of two things.

Possible identity theft. You see an inquiry from a lender you never contacted, tied to an application you never made. That can be an early sign someone is trying to open credit in your name.

A pull you never permitted. A company accessed your report without a permissible purpose and without your consent.

Before you conclude an inquiry is fraudulent, rule out the innocent explanations – because many “I don’t recognize this” inquiries are perfectly legitimate:

The lender does business under a different legal or parent-company name than the brand you applied with.

You authorized a dealership, mortgage broker, or landlord to shop your application to multiple lenders, so several pulls trace back to one thing you agreed to.

An existing creditor reviewed your account, or a company that bought your loan or card pulled your file.

If, after checking, the inquiry is truly unauthorized, handle it correctly rather than blasting a generic online dispute. Contact the creditor listed and ask them to explain the pull and provide proof you authorized it. If it was fraud, file with each bureau that shows the inquiry, report identity theft at IdentityTheft.gov to generate an Identity Theft Report, and consider a fraud alert or credit freeze. Do this truthfully – the affidavit is signed under penalty of perjury, so it must reflect what actually happened.

Disputing an inquiry vs. disputing an account error

People blur these two, and the difference matters. An inquiry is a record that your credit was pulled. An account error is wrong information on a tradeline – a balance that is off, a payment marked late that you made on time, an account that is not yours, a collection that should have aged off. Account errors are exactly what the FCRA dispute process is built to fix: you contact both the credit reporting company and the furnisher, and they generally must investigate within 30 days.

Situation

Is disputing appropriate?

Why

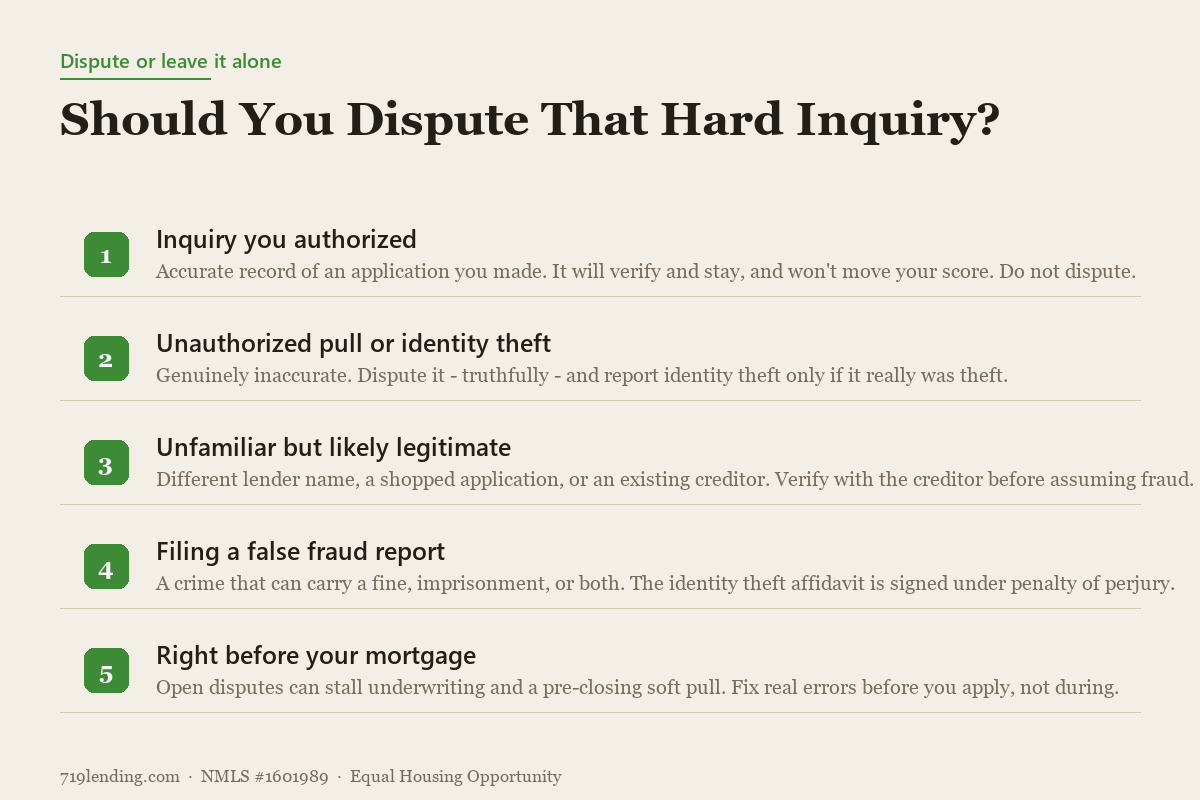

Hard inquiry you authorized

No

It is accurate; it will verify and stay, and won’t move your score

Hard inquiry you did not authorize (possible fraud)

Yes – truthfully

Genuinely inaccurate; report identity theft only if it really was theft

Wrong balance, wrong late, account that isn’t yours

Yes

These are inaccuracies the FCRA process exists to correct

Accurate late payment or collection you simply don’t like

No

Accurate items only get verified; disputing won’t remove them

Chasing accurate late payments off your report through disputes does not work either – see our guide on late payments and your mortgage for what actually helps there.

The mortgage layer: don’t dispute right before you apply

This is where the stakes jump for a homebuyer. A mortgage runs on credit reports that have to stay clean and readable from application through funding – and a dispute you open can gum up that machinery at the worst moment.

Two specific risks:

An open dispute can complicate or stall the file. Mortgage underwriting engines flag disputed items. A dispute you filed to “clean up” your report can force a manual review or require the item to be re-evaluated as if undisputed – extra steps, extra time, right when you are trying to lock a rate and close on schedule.

Lenders re-check your credit late in the process. Most lenders run a final soft pull – a “credit refresh” – within a few days of closing to confirm nothing changed: no new debts, no score drop, no new inquiries. New activity you kicked up, or new debt you took on, can push your debt-to-income ratio out of bounds. If a liability that exists at closing was not disclosed at application, Fannie Mae requires the lender to recalculate your DTI and re-run the loan, and an undisclosed debt can jeopardize or unwind it.

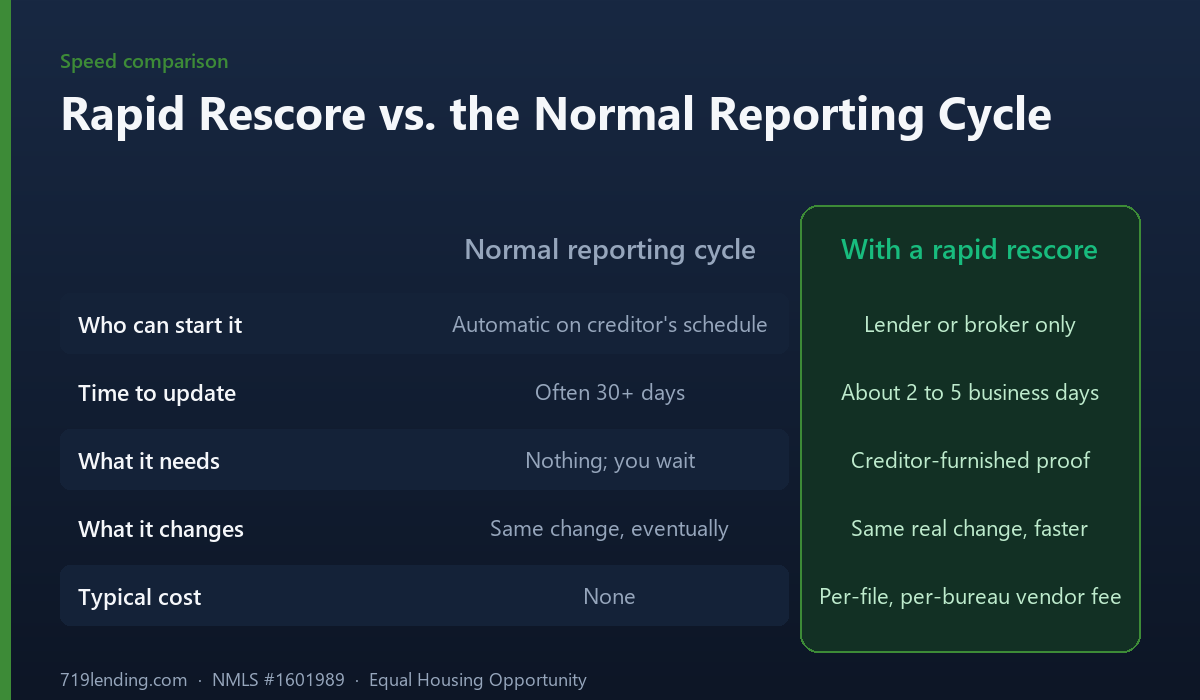

So the rule of thumb from the loan side is simple: do not go on a dispute spree in the weeks before or during your mortgage. The couple of points a legitimate inquiry costs you are trivial next to the risk of freezing your file mid-process. If there is a genuine error worth fixing – a real inaccuracy that is dragging your qualifying score – the move is to raise it before you apply, or to let your loan officer coordinate the timing, sometimes through a rapid rescore that captures a legitimate correction in days rather than weeks.

And remember what a hard inquiry does not do to a mortgage. When you shop several mortgage lenders in a short window, FICO’s mortgage scoring treats those pulls as a single inquiry and even ignores mortgage and auto inquiries made in the roughly 30 days before scoring – so responsible rate shopping is not something you need to “fix” by disputing. We cover that fully in why your lender’s credit score is different.

What to do instead

If your goal is a stronger file for a mortgage, put your energy where it actually pays off:

Leave authorized inquiries alone. They fade from your score in about a year and were only ever worth a few points.

Fix real errors, early. Genuine tradeline inaccuracies are worth disputing through the proper FCRA channel – but do it before you apply, not during underwriting.

Work the levers that move the needle. Lowering credit utilization before a mortgage and keeping every payment on time do far more than any inquiry cleanup.

Only file a fraud claim if it is fraud. Unauthorized inquiry or identity theft – real ones – get reported truthfully and promptly.

Loop in your loan officer. Before you dispute anything with a home purchase in sight, ask. Timing and sequencing are half the battle, and a good broker will tell you what is worth touching and what to leave alone.

If you are getting ready to buy in Colorado and want a second set of eyes on your report before you start disputing anything, that is exactly the kind of thing a mortgage broker in Colorado Springs should help you sort out – and it is a conversation worth having before, not after, you have opened a dispute.

Frequently asked questions

Does disputing a hard inquiry raise my credit score? Almost never. A single hard inquiry costs most people fewer than five points to begin with, and if the inquiry was legitimate and authorized, disputing it will not get it removed – the bureaus verify it and it stays. The only inquiries that come off through a dispute are ones that were genuinely unauthorized.

Can you remove hard inquiries from your credit report? Only if they are inaccurate – meaning you did not authorize the pull, often because of identity theft. Legitimate inquiries from applications you actually made cannot be removed and will fall off on their own after two years, ceasing to affect your score after about one year.

Is it illegal to dispute hard inquiries? Disputing a genuine unauthorized inquiry is your right under the FCRA. What is illegal is knowingly filing a false report – especially a false identity theft report – to remove accurate items. The FTC has warned that this is a crime that can carry a fine, imprisonment, or both, and the identity theft affidavit is signed under penalty of perjury.

Will disputing inquiries hurt my mortgage application? It can. Open disputes can trigger extra underwriting steps or manual review, and lenders re-check your credit with a soft pull shortly before closing. Filing disputes right before or during your loan can complicate the process and delay closing. Handle any legitimate corrections before you apply, and ask your loan officer first.

What if I don’t recognize an inquiry on my report? Do not assume fraud. It may be a lender operating under a different name, a company you authorized to shop your application, or an existing creditor. Contact the creditor listed and ask them to confirm the pull. Only if it is truly unauthorized should you dispute it as fraud and report identity theft.

Do mortgage rate-shopping inquiries hurt my score? Not the way people fear. FICO’s mortgage scoring counts multiple mortgage pulls in a short window as a single inquiry and ignores mortgage and auto inquiries made in roughly the 30 days before scoring. Shopping several lenders responsibly is not something you need to dispute away.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. This article is educational and general in nature and is not credit repair, legal, or financial advice; figures and program guidelines are general – confirm current with your loan officer. 719 Lending is not affiliated with, or acting on behalf of or at the direction of, any government agency. Last updated: June 30, 2026.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.

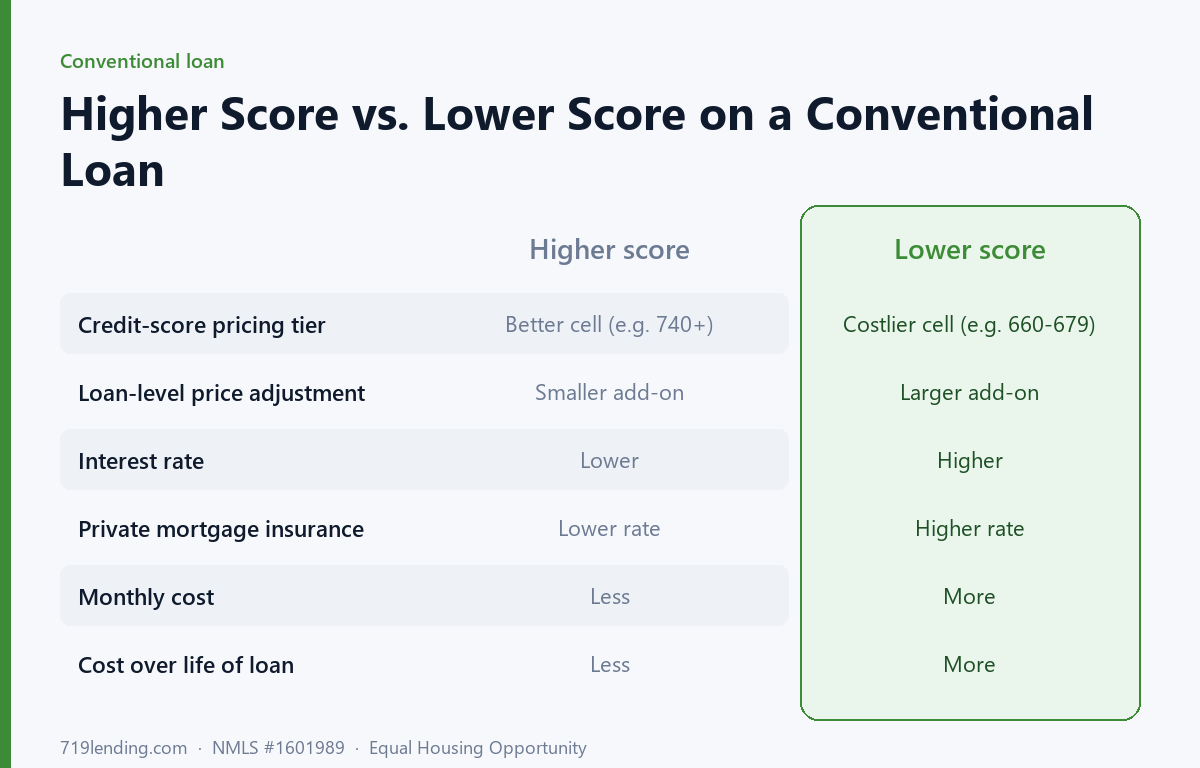

Does credit score affect mortgage rate? Yes - on conventional loans it moves your rate and PMI through credit-score pricing tiers. Here is how the bands work.

A rapid rescore lets your lender update your mortgage credit in about 2-5 business days after a real change like a card paydown or a corrected error. Here is how it works, why only a lender can order it, and how it fits a Colorado Springs home loan.