Yes – you can usually get a mortgage with collections, charge-offs, or medical debt still on your report, and in many cases you do not have to pay them off first. Whether you must pay depends almost entirely on your loan program and property type, not on a single national rule. A conventional loan on a primary home treats old collections very differently than an FHA loan, and medical debt is treated more leniently than almost any other kind. The catch is that the balance can stay put while the monthly payment still counts against your debt-to-income ratio – and that mortgage layer is where a broker earns their keep.

Below we separate two questions people jam together: will this debt block my loan? and should I pay it off? The honest answer to both is “it depends, and here is how by program.” Figures below are general – confirm current for your file.

First, get the vocabulary straight: collection vs. charge-off vs. medical

These three words get used interchangeably, but underwriters treat them as different animals.

Collection – the original creditor gave up trying to collect and either sold the debt to a third-party collector or assigned it out. A separate collection tradeline appears on your report.

Charge-off – the creditor wrote the debt off on its own books for accounting and tax purposes. This is the single most misunderstood item on a credit report: a charge-off is not forgiveness. You still owe the money, and some creditors keep pursuing the full balance in-house rather than selling it. The label describes the creditor’s bookkeeping, not your obligation.

Medical collection – a collection that originated from a healthcare bill. As of 2026 this category has its own, much friendlier set of rules, which we cover in detail below.

All three can sit on your report at a $0 balance and still be scored as derogatory. And all three can show up on your tri-merge mortgage report even when they never appeared on the free consumer app you check.

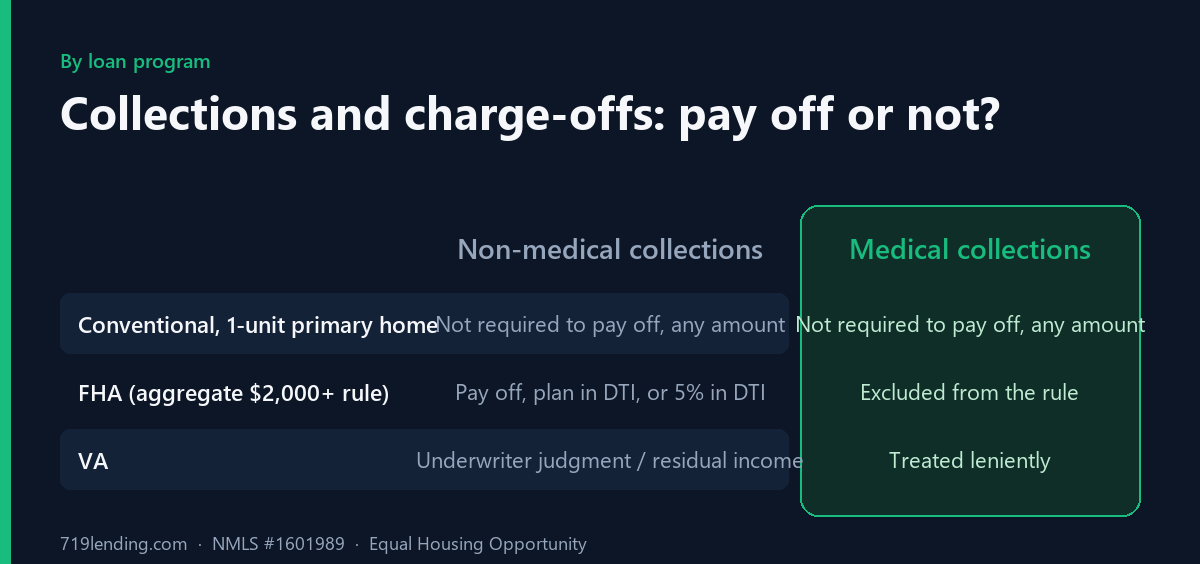

General – confirm current. On a one-unit primary residence, conventional loans do not require collections or non-mortgage charge-offs to be paid off; FHA applies a $2,000 aggregate rule to non-medical collections only; VA leaves most to underwriter judgment. Medical collections are carved out across programs. Sources: Fannie Mae Selling Guide, HUD Handbook 4000.1, VA credit standards.

Do you have to pay off collections to get a mortgage? It depends on the loan

There is no universal “pay everything off” requirement. Each agency writes its own playbook, and the differences are large enough that the same borrower can be told “leave it alone” by one lender and “pay it first” by another – because they are quoting different programs.

Loan program

General treatment of collections and non-mortgage charge-offs

No mandatory payoff. But if your non-medical collections total $2,000 or more, the lender must do one of three things: (1) you pay them off, (2) you document a payment plan and that payment counts in your DTI, or (3) 5% of the outstanding balance is added to your monthly DTI as a hypothetical payment – even if you never pay a dime.

VA

No blanket payoff requirement. The underwriter uses judgment on the overall pattern – how many, how recent, how large – alongside VA’s residual-income test. Isolated collections often do not need to be paid. Judgments, federal debts, and tax liens are the exception and must be resolved or under a documented plan.

Notice what is not in that table: your credit score alone. A pile of paid or unpaid collections can be perfectly allowable under the program rules and still drag your score into a worse pricing tier or below a lender overlay. Program eligibility and score-driven pricing are two different gates – see what credit score you need to buy a house for how the two interact.

The mortgage layer everyone forgets: DTI counts the payment even if the balance stays

Here is the twist that catches borrowers off guard. “You don’t have to pay it off” is not the same as “it doesn’t affect your loan.” On FHA, a large collection balance can inject a phantom monthly payment into your debt-to-income ratio – 5% of the balance, or a documented plan payment. On a $10,000 aggregate collection balance, that is a $500 hypothetical payment sitting on your DTI, whether or not any real money moves.

Debt-to-income is the co-equal qualifier next to your credit score. A borrower with plenty of income can absorb that phantom payment; a borrower already near the DTI ceiling may be pushed over it. This is exactly the kind of trade-off a mortgage broker prices out before you touch a single account – which program forgives what, and which choice keeps your DTI under the cap. If your ratio is tight, learning how much you actually need up front and where your cash is best deployed matters as much as the debts themselves.

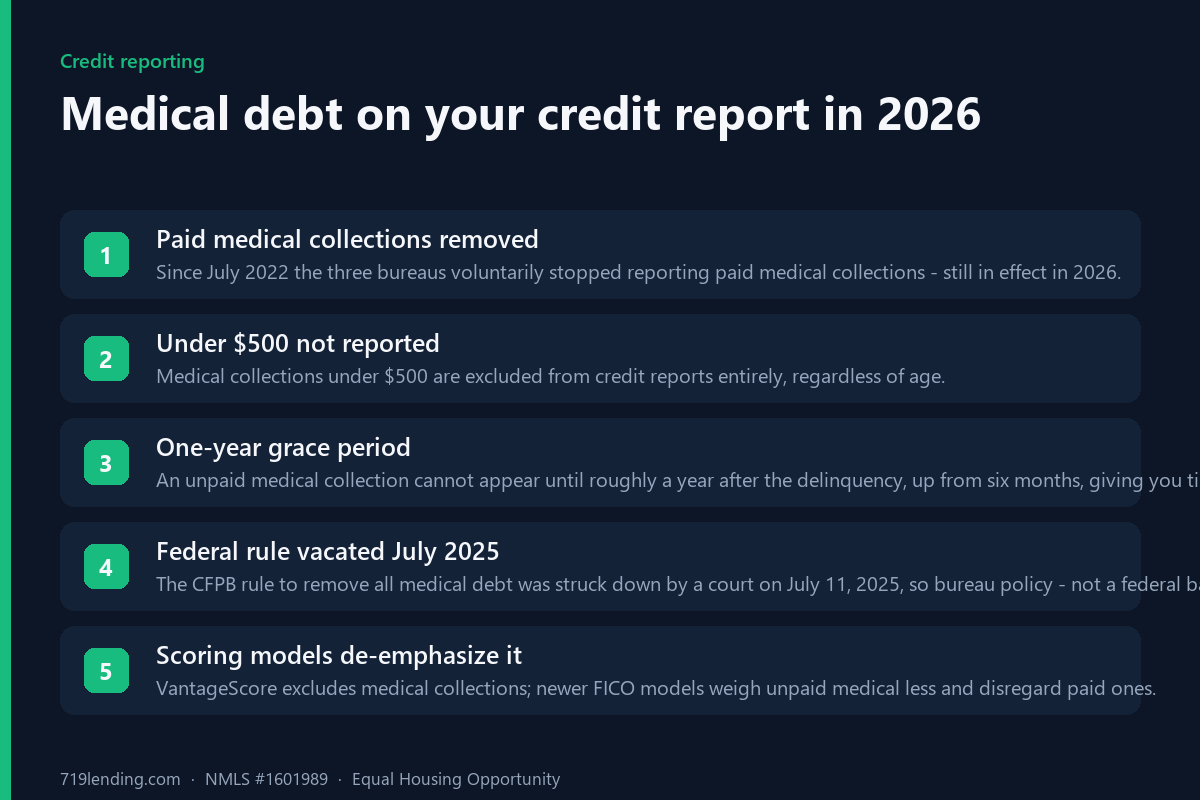

General – confirm current. As of June 2026, bureau policies from 2022-2023 remain in force; the January 2025 CFPB medical-debt rule was vacated by a federal court on July 11, 2025 and is not enforceable. Sources: CFPB, credit bureau (Equifax/Experian/TransUnion) policies.

Medical debt in 2026: what actually changed, and what stuck

Medical debt is the most in-flux category in credit reporting right now, so it is worth getting current facts rather than repeating old advice.

What the bureaus voluntarily did (2022-2023, still in effect): Equifax, Experian, and TransUnion stopped reporting paid medical collections (effective July 1, 2022), stopped including medical collections under $500 at all (effective early 2023), and extended the grace period before an unpaid medical collection can appear on your report from six months to a full year. Those are industry policies, and they remain in place as of 2026.

What the federal rule tried to do – and why it is not in force: In January 2025 the Consumer Financial Protection Bureau finalized a rule (an amendment to Regulation V) that would have removed essentially all medical debt from credit reports and barred creditors from considering it. That rule was vacated by a federal court on July 11, 2025 (Eastern District of Texas), on the grounds that it exceeded the CFPB’s authority under the Fair Credit Reporting Act. As of mid-2026 that rule is not enforceable – so the broad federal ban never took effect, and medical debt can still appear on reports within the limits above.

How scoring models treat it: This is where the real relief lives. VantageScore 3.0 and 4.0 exclude medical collections from the score calculation entirely. Newer FICO models (FICO 9 and 10) weigh unpaid medical collections less heavily than other collections and disregard paid ones. But the mortgage FICO versions lenders pull are older by design – so an unpaid medical collection over $500 can still show up and factor in on a mortgage file, which is why medical debt is not automatically invisible to your loan even though it may be invisible on your consumer app.

The good news for buyers: across conventional, FHA, and VA, medical collections are specifically carved out of the pay-off and DTI-hit rules that apply to ordinary collections. A stack of medical debt that would trigger the FHA $2,000 rule as a non-medical balance generally does not. Confirm the current treatment for your file – but as a rule, medical debt is the friendliest derogatory a mortgage borrower can carry.

The paying-it trap: how paying an old collection can backfire

The instinct to “just pay it and clean it up” is reasonable and often correct – but on an old collection it can hurt you in two specific ways, so time it deliberately.

It can restart the statute of limitations for being sued. The CFPB warns that making a partial payment on – or even acknowledging – an old debt can restart the clock a collector has to sue you, in many states. A debt that was legally too old to be sued over can become collectible again the moment you send money toward it. This is separate from your credit report.

Re-aging on the report is a real (and illegal) hazard. A negative item can stay on your credit report for up to seven years from the original delinquency, and nothing – not even a payment – is supposed to restart that seven-year clock. But some collectors illegally re-age a debt to make it look newer, which resets its apparent recency and can drop your score right when you least expect it.

Because recency drives how much a derogatory item costs your score, paying an old collection without a plan can open a new wound – the payment refreshes the activity date and, in scoring terms, can look worse than leaving a stale item alone. The safe move before a mortgage is a pay-for-delete in writing (removal, not just payment, is what helps the score) coordinated with your lender’s timing. For the full mechanics of the date-of-last-activity trap and when paying does more harm than good, see our guide on how late payments and derogatory marks affect your mortgage.

The transaction-grade play: pay-for-delete plus a rapid rescore

If you are already under contract and a collection is dragging your qualifying score or blocking a program, you do not have to wait months for the bureaus to catch up. When a creditor furnishes proof that an account was deleted, paid, or corrected, your lender can order a rapid rescore and update the mortgage credit report in a few business days rather than a full billing cycle. Rapid rescore is a lender-only tool – you cannot order it yourself – which is another reason to run this through a broker instead of DIY-ing it.

The winning sequence is usually: (1) identify which items actually matter for your program and pricing tier, (2) negotiate deletions or documented plans in writing before or early in the process, (3) let the lender rapid-rescore the corrections, and (4) make sure any remaining balances are accounted for in DTI the way the program requires. That is a coordinated play, not a scramble – and it is far more effective than blindly paying everything the week before closing.

How this fits the rest of your file

Collections and charge-offs rarely travel alone. If they came out of a rough stretch, you may also be dealing with waiting periods after a bankruptcy, or trying to rebuild a thin file at the same time. Two quick reminders that trip people up:

Do not open or close accounts to “fix” collections mid-process. A new tradeline or a closed old card can move your DTI, utilization, and average age at the worst moment – and can trigger the lender’s soft re-pull before funding.

Keep utilization low while you are at it. The fastest score lever is not paying a five-year-old collection; it is getting your revolving balances down before the lender pulls. See our guide to credit utilization before a mortgage.

Self-employed borrowers have an extra wrinkle worth flagging: business debts with a personal guarantee can land on your personal report and behave like any other collection – our self-employed mortgage guide covers how that interacts with qualifying.

Frequently asked questions

Do I have to pay off collections to qualify for a mortgage? Not necessarily. On a conventional loan for a one-unit primary residence, collections and non-mortgage charge-offs generally do not have to be paid off regardless of amount. FHA does not mandate payoff either, but if your non-medical collections total $2,000 or more, the lender must either have you pay them, document a payment plan counted in your DTI, or add 5% of the balance to your DTI. VA leaves most collections to underwriter judgment. It genuinely depends on the program – general, confirm current for your file.

Does a charge-off mean the debt is forgiven? No. A charge-off is the creditor’s accounting decision to write the debt off its own books for tax purposes. You still owe the money, and some creditors keep pursuing the full balance in-house instead of selling it. Treat a charge-off as an unpaid debt, not a canceled one.

Does medical debt still hurt my mortgage in 2026? Much less than it used to. Since 2022-2023 the three bureaus voluntarily stopped reporting paid medical collections and medical collections under $500, with a full-year grace period before any unpaid medical collection appears. VantageScore excludes medical collections entirely and newer FICO models de-emphasize them. A broad federal rule to remove all medical debt was vacated by a court in July 2025, so those bureau policies – not a federal ban – are what protect you now. Conventional, FHA, and VA also carve medical collections out of their pay-off and DTI rules. Confirm current treatment for your situation.

Will paying an old collection raise my score before I buy? It might, but it can also backfire. Paying or even acknowledging an old debt can restart the statute of limitations for a lawsuit in many states, and a fresh payment can refresh the item’s activity date in a way that scoring models read as more recent – sometimes lowering your score. The score-safe approach is a written pay-for-delete coordinated with a rapid rescore, rather than paying blindly. General – confirm current.

How is the collection payment counted if I don’t pay it off? On FHA, if you leave a non-medical collection unpaid and have no documented plan, the lender adds 5% of the outstanding balance to your monthly debt-to-income ratio – a hypothetical payment you never actually make. A $10,000 balance becomes a $500 phantom DTI payment. That is why leaving a debt unpaid can still affect your approval through DTI even when the program does not require payoff.

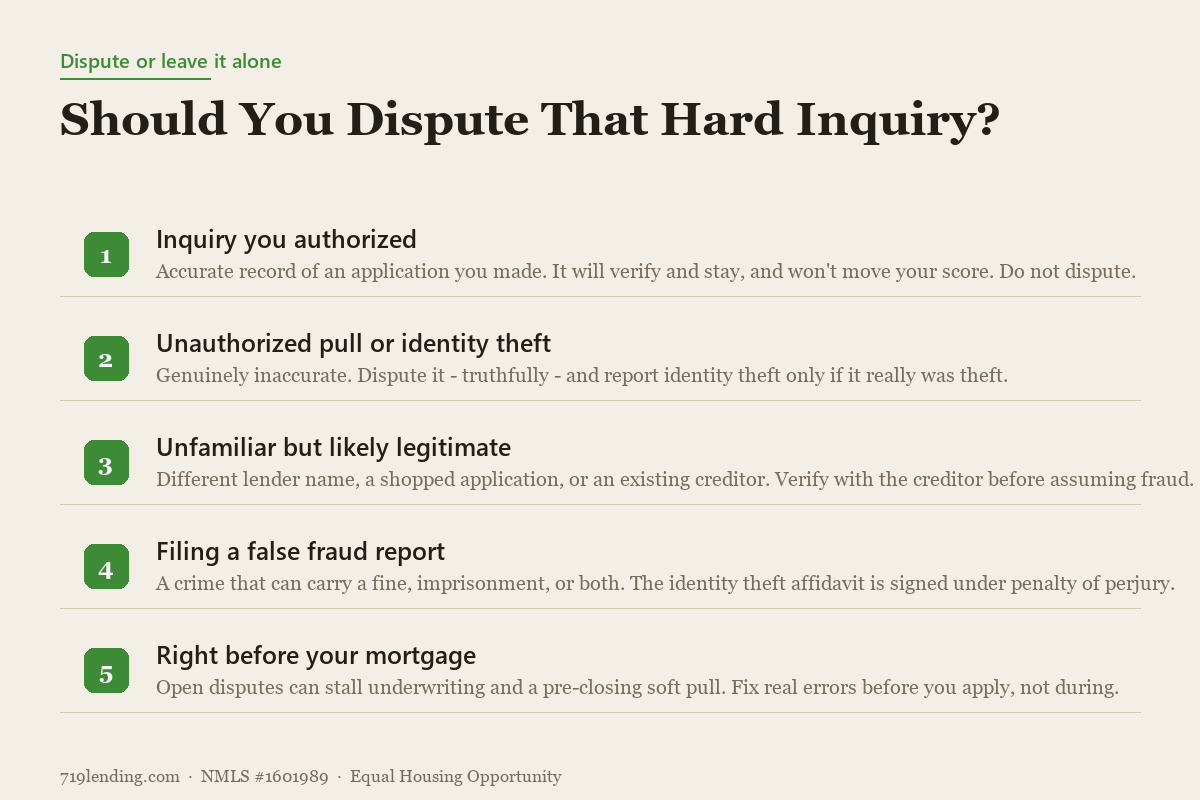

Should I dispute a collection right before applying for a mortgage? Be careful. A tradeline marked as disputed can drop out of scoring temporarily and can stall automated underwriting, forcing a manual re-underwrite – so it is a pre-application move, not a mid-escrow one. Clear or resolve disputes before your lender pulls credit, and coordinate the timing with your loan officer.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. This article is educational and not a commitment to lend or credit advice. Loan-program rules, thresholds, dollar figures, and scoring-model treatments are general and change over time – confirm the current requirements for your specific situation with a licensed loan officer. 719 Lending is not affiliated with, or acting on behalf of or at the direction of, HUD/FHA, the VA, USDA, or any government agency. Rules cited (FHA HUD Handbook 4000.1, Fannie Mae Selling Guide, VA credit standards, CFPB guidance) are current as of June 2026 and subject to change. Last updated: June 30, 2026.

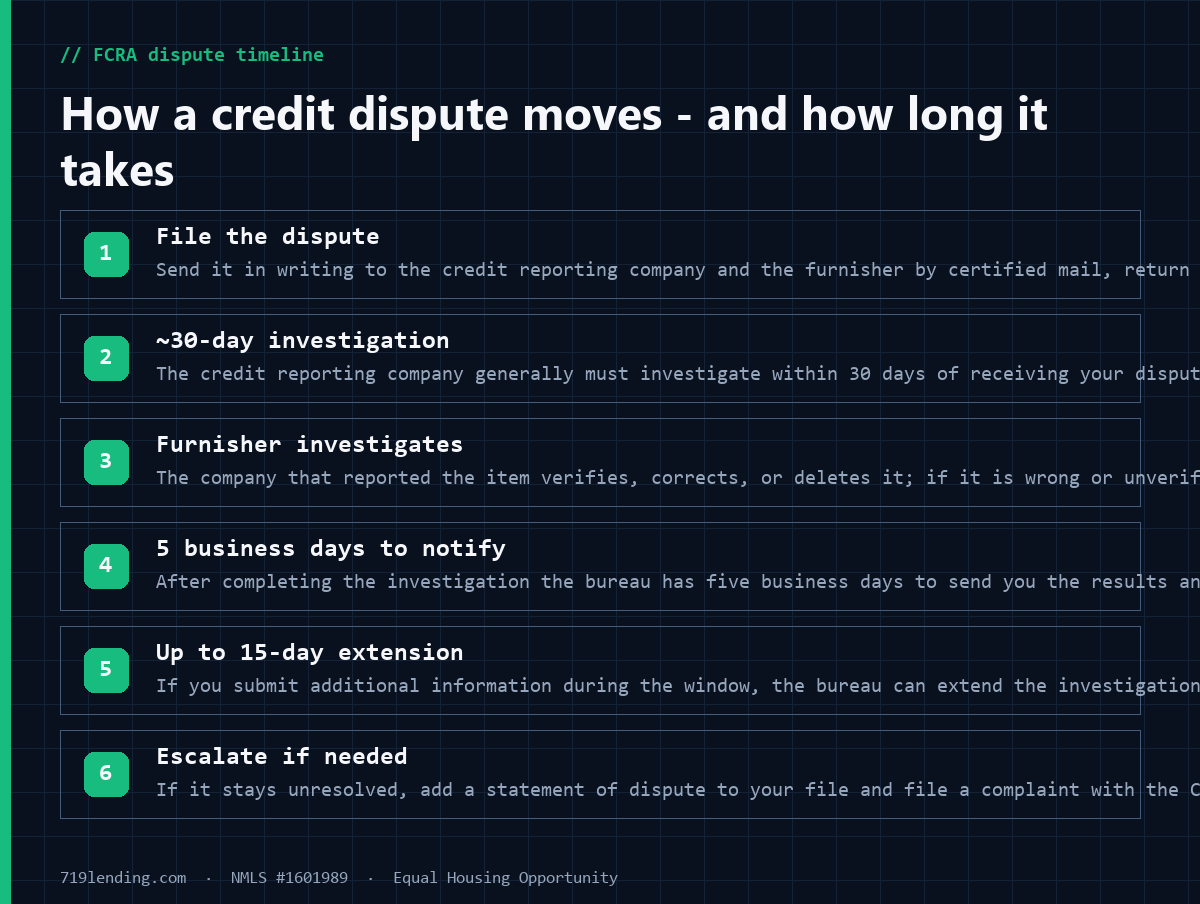

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.