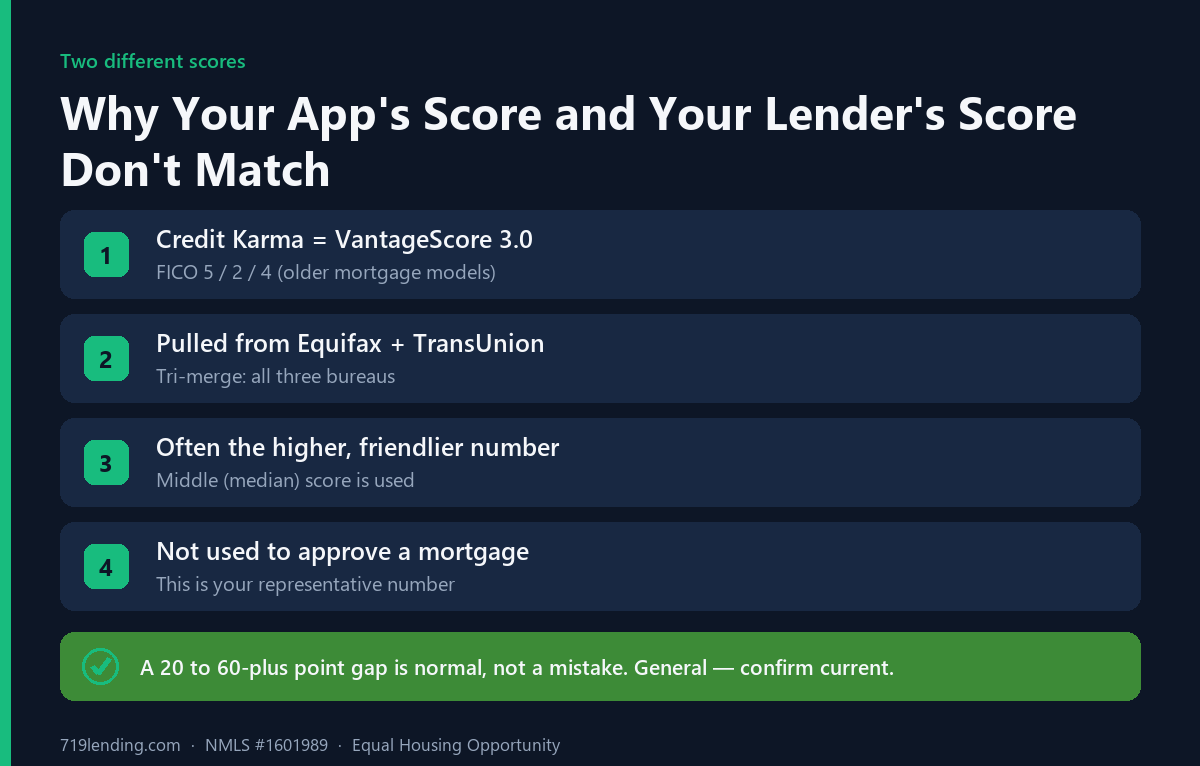

The short answer: the credit score your mortgage lender pulls is almost always lower than the number in your Credit Karma or banking app because they are two entirely different scoring systems. Credit Karma shows a VantageScore. Your mortgage lender pulls older, mortgage-specific FICO models from all three bureaus and uses the middle number. A gap of 20, 40, even 60-plus points between them is normal, not a mistake, and not your loan officer hiding a better number from you.

If you have ever watched your app show a proud 720, then heard your lender say “we are working with a 668,” you are not imagining it and you were not lied to. This is one of the most common and most upsetting surprises in the entire mortgage process. The good news is that once you understand the plumbing, the gap stops feeling like a trap and starts making sense. As a mortgage broker in Colorado Springs, this is a conversation we have almost every week, so let us walk through exactly what is happening.

Last updated: June 30, 2026.

Why the number your lender sees is not the number you see

There is no single “credit score.” There are dozens of scoring formulas, built by two different companies, calculated on data from three separate credit bureaus. The score you look at for free and the score a mortgage underwriter uses are built by different math, on different models, for different purposes. So the real question is not “which one is right” but “which one is being used to decide my loan.”

Two things drive the gap. First, the brand of score: FICO versus VantageScore. Second, the version of the score: the free FICO you might see online is a newer, more forgiving model than the older FICO versions the mortgage industry uses. Stack those two differences and a meaningful point spread is the expected outcome.

The score you see for free and the score your lender uses are two different systems. A 20 to 60-plus point gap is normal. General — confirm current.

The single biggest reason: Credit Karma is VantageScore, not FICO at all

Here is the reveal that clears up most of the confusion. The score on Credit Karma is a VantageScore, specifically VantageScore 3.0 drawn from your Equifax and TransUnion files. It is not a FICO score. It is a separate scoring model, developed jointly by the three credit bureaus as a competitor to FICO.

Mortgage lenders, on the other hand, generally use FICO scores, and specific older versions of them. So when you compare your Credit Karma number to your lender’s number, you are not comparing a “high” score to a “low” score. You are comparing an apple to an orange. They will rarely match, and there is no reason they should. VantageScore and FICO weigh your history differently, treat certain items differently, and can land dozens of points apart on the exact same credit file.

This matters because so many borrowers assume the lender’s lower number means something went wrong, or that the lender is being stingy. Neither is true. Your free app was simply never showing you the number that a home loan is actually decided on.

The free FICO you may see through a bank or card issuer is usually FICO Score 8, the version most widely used for everyday lending like credit cards and auto loans. The mortgage versions above (5, 2, and 4) are older generations. They were locked in years ago, and the mortgage industry has kept using them for consistency across the millions of loans sold to Fannie Mae and Freddie Mac. An older model plus different bureau data equals a number that often sits below your consumer FICO 8, and well below a VantageScore.

So even if your Credit Karma app were showing a FICO score, it still would not be the mortgage FICO. The mortgage version is a different, older release entirely.

Lenders use the median of three scores, never the average. On joint loans, the lower borrower’s middle score generally sets pricing. General — confirm current.

The tri-merge pull and the middle-score rule

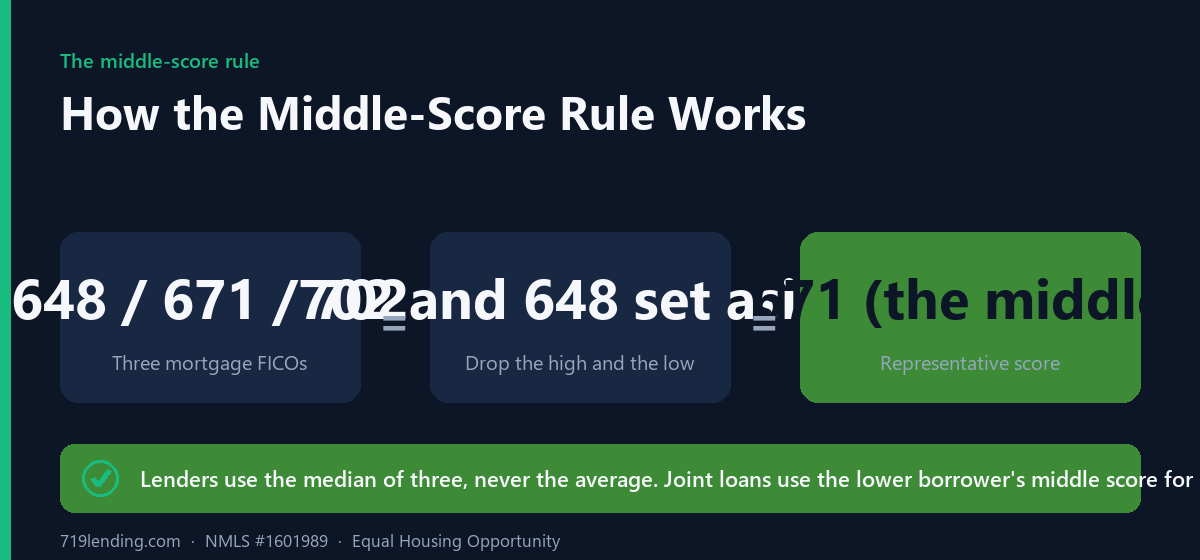

Now layer on how the three scores get combined. Your mortgage lender does not pull one score. They pull a tri-merge report, which stitches together your credit from all three bureaus (Equifax, Experian, and TransUnion) into one document, with a FICO score from each.

That gives three numbers. Here is the rule that trips people up: the lender does not average them. They take the middle score, the median. The high one and the low one are set aside, and the one in the middle becomes your representative score. So if your three mortgage FICOs come back as 648, 671, and 702, your representative score is 671. Not the 702 you would love to use, and not the average of 674, but the middle value.

A quick example of how these forces stack:

Your Credit Karma app shows 721 (a VantageScore).

Your three mortgage FICOs come back at 648 / 671 / 702.

The lender uses the middle, so your representative number is 671.

That is a 50-point gap from your app, and every step of it is completely normal.

For a joint application with two borrowers, there is a second wrinkle. Under Fannie Mae’s guidance, each borrower’s representative score is figured first (the middle of three, or the lower of two), and then, for pricing purposes, the loan generally uses the lower of the borrowers’ representative scores. One spouse’s rough patch on a single bureau can end up setting the number the whole loan is priced on. Talking through that with an experienced broker before you apply is the fastest way to avoid a surprise at rate lock.

Why your loan officer actually wants your score to be high

This is the part worth sitting with, because the fear underneath “why is my credit score different from my lender” is usually a suspicion that the lender is sandbagging your number to charge you more.

The opposite is true. A mortgage broker is paid at closing. If your loan does not close, we do not get paid. A higher score means a smoother approval, a stronger rate, a happier client, and a loan that actually funds. Every incentive we have points the same direction as yours: get that representative score as high as legitimately possible. We are not the party choosing the model or the number. Fannie Mae, Freddie Mac, and the FICO formula decide that. We are the ones trying to help you clear it.

So when a broker pulls your credit and the number comes in lower than your app, that is not us moving the goalposts. That is us showing you the real field you are playing on, and then helping you move the ball down it. Working with an experienced broker who can read the tri-merge and spot fixable issues is a big part of why the lender’s number and your app’s number stop feeling like a betrayal.

Do inquiries and rate shopping tank your score?

Two more fears worth putting to rest, because they feed the “my lender wrecked my score” story.

Checking your own credit does nothing to your score. Per the Consumer Financial Protection Bureau, requesting and reviewing your own report is a soft inquiry, which has no effect on your score. Your app’s daily updates are not hurting you.

Shopping multiple mortgage lenders barely dents your score. A single hard inquiry from a lender typically has only a small effect, and scoring models generally count multiple mortgage-shopping inquiries within a short window as a single inquiry, so getting quotes from several lenders in a short span counts essentially as one. You are not punished for comparison shopping the way people fear.

The takeaway: the lower mortgage number is about which model is used, not about the act of pulling your credit.

What about the newer credit-score models coming to mortgages?

You may have heard that mortgage credit scoring is changing, and it is, slowly. The Federal Housing Finance Agency has validated two newer models, FICO 10T and VantageScore 4.0, for use by Fannie Mae and Freddie Mac. As of mid-2026, though, this is a phased, limited rollout: VantageScore 4.0 is available for conventional loans at a limited set of approved lenders, FICO 10T historical data is expected to publish in summer 2026 ahead of broader adoption, and classic FICO (the 5/2/4 models above) remains the standard at most closings.

FHFA also did not proceed with an earlier plan to move to a two-bureau “bi-merge” report, so the tri-merge, three-bureau pull stays in place for now. Practically, this means the number your lender pulls today is still the older classic FICO, and it will still likely differ from your app. When the industry fully transitions, the gap may narrow, but do not count on it yet. This is general and evolving, so confirm current details with your lender at the time you apply.

What to actually do about the gap

Stop steering by the number in your app, and start steering by the number your lender pulls. A few practical moves:

Get your mortgage-pulled score early. Ask a broker to pull your tri-merge before you are under contract, so you know your real representative number, not your VantageScore.

Do not panic at the gap. A 20-to-60-point difference between Credit Karma and your mortgage FICO is expected. It is a model difference, not a red flag.

Ask about rapid rescore. If a paydown or a corrected error can lift your middle score across a pricing tier, a lender-ordered rapid rescore can capture it in days rather than months.

Let your loan officer coordinate the timing. Do not open new accounts or make big credit moves once you are in process without checking first.

Frequently asked questions

Why is my credit score different from my lender’s? Because they use different scoring systems. Free apps like Credit Karma show a VantageScore, while mortgage lenders generally pull specific older FICO models (Beacon 5.0, Fair Isaac Risk Model V2, and Classic 04) from all three bureaus. Different brand, different version, different number. A gap of 20 to 60-plus points is normal.

Is Credit Karma a FICO score? No. Credit Karma shows VantageScore 3.0 based on your Equifax and TransUnion data. It is a separate scoring model from FICO, and mortgage lenders do not use VantageScore 3.0 to approve home loans.

Which FICO scores do mortgage lenders use? Conventional lenders typically pull Equifax Beacon 5.0 (FICO 5), Experian Fair Isaac Risk Model V2 (FICO 2), and TransUnion FICO Risk Score Classic 04 (FICO 4). These are older versions than the FICO Score 8 you often see on free apps.

Does my lender use the average of my three scores? No. For a single borrower, the lender uses the middle (median) of the three FICO scores as the representative score. The highest and lowest are set aside. On a joint application, the lower of the two borrowers’ representative scores generally sets the pricing.

Why is my mortgage score lower than my free FICO score? Even your free FICO is usually FICO Score 8, a newer, more forgiving model. Mortgage FICO versions are older generations pulled from all three bureaus, so the mortgage number often comes in below both your free FICO 8 and your VantageScore.

Does my loan officer benefit from a lower score? No, the opposite. A broker is paid only when the loan closes, so a higher score, a smoother approval, and a funded loan all serve the broker’s interest as much as yours. The lender does not choose your score; the FICO formula and the bureaus do.

Will shopping several lenders hurt my score? Only slightly. Mortgage-shopping inquiries made within a short rate-shopping window are generally grouped into a single inquiry, and a hard inquiry has only a small effect to begin with. Checking your own credit has no effect at all.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, or acting on behalf of or at the direction of, FHA, VA, USDA, HUD, or any government agency. Credit-score models, mortgage program rules, and qualifying guidelines change and vary by borrower profile, lender, and loan program; all figures and ranges here are general, illustrative, and current as of June 2026, and are not a commitment to lend or a guarantee of any rate or approval. Confirm current details with a licensed mortgage professional.

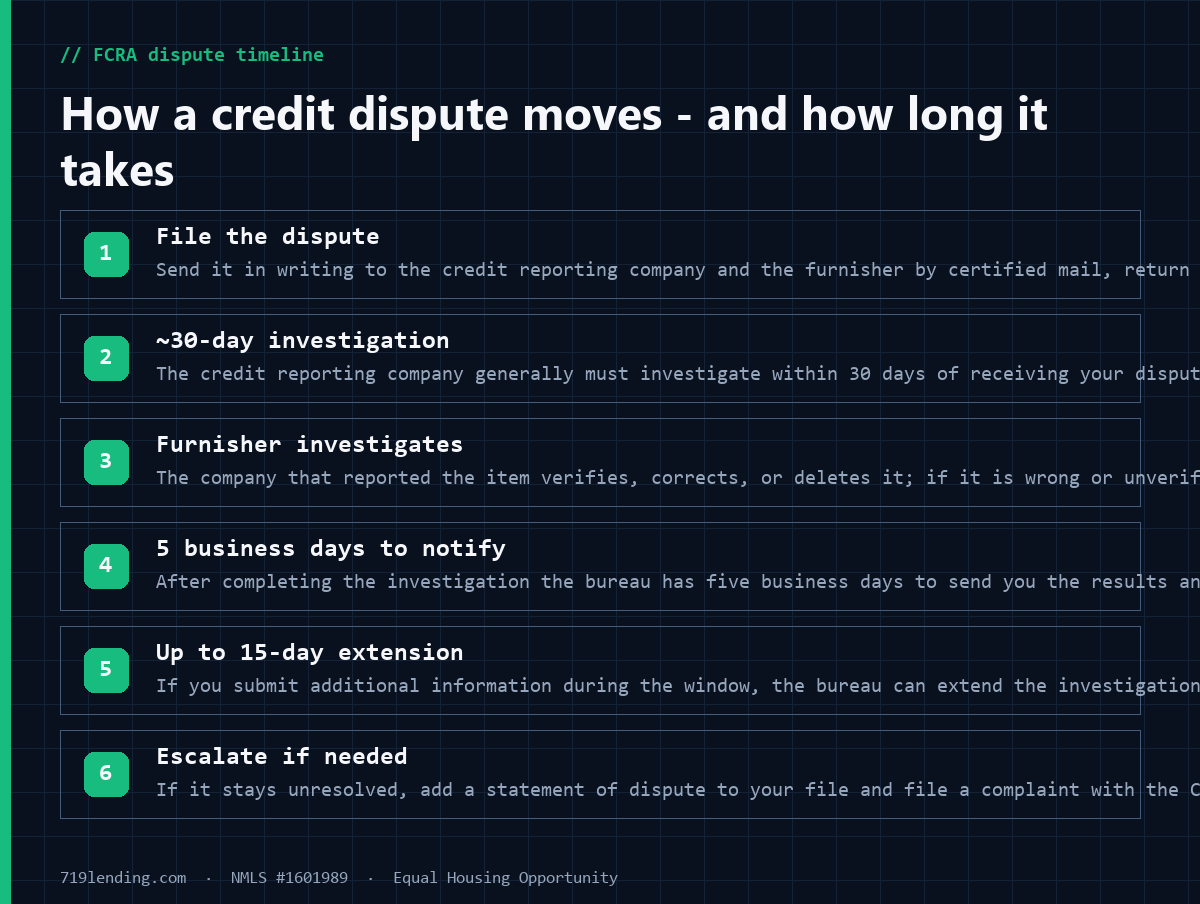

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

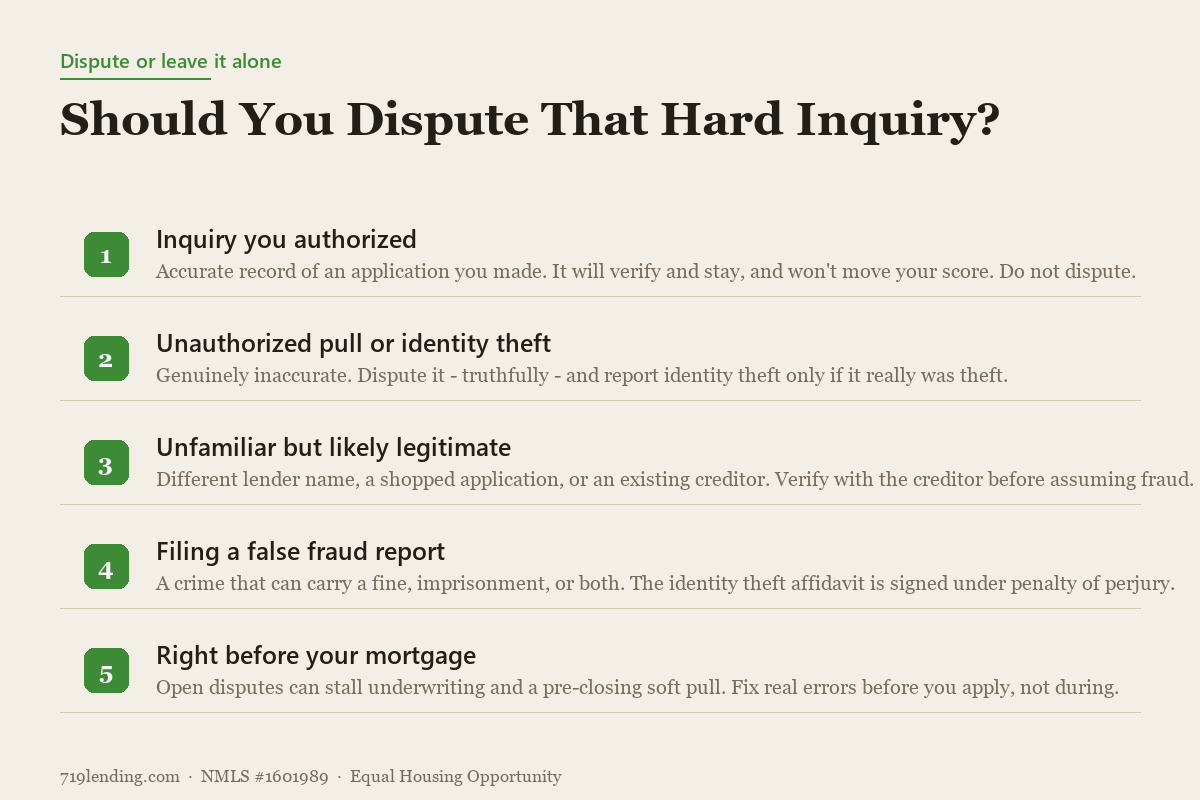

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.