Credit age and credit mix are the two credit factors you cannot rush – and trying to force them right before a mortgage usually backfires. Length of credit history is about 15% of a FICO Score and credit mix is about 10% (these weights are general and vary by profile), so together they shape roughly a quarter of your number. But unlike paying down a card, you cannot buy your way to a longer history or a broader mix in 30 days. Opening a new card to “add a tradeline” right before you buy actually lowers your average account age and can drop your score at the worst possible moment. The mortgage rule is simple: do not open or close anything while you are buying without talking to your loan officer first.

General FICO factor weights; the exact breakdown varies by credit profile. General – confirm current.

The three slow factors: age, mix, and new credit

FICO builds your score from five categories. Two of them – payment history (about 35%) and amounts owed / utilization (about 30%) – are the fast levers you can move in weeks. The other three move slowly, or work against you when you try to force them:

Length of credit history – about 15%. How long your accounts have been open, including the age of your oldest account, the age of your newest account, and the average age of all your accounts.

Credit mix – about 10%. The variety of account types you manage: revolving credit (cards) and installment loans (auto, student, personal, mortgage).

New credit – about 10%. How recently and how often you have opened accounts. A flurry of new accounts reads as elevated risk.

FICO is explicit that these percentages are general – the exact weighting depends on your unique profile. Someone new to credit leans more on mix and age; someone with decades of history leans more on payment behavior. Treat every number here as “general – confirm current,” not a fixed law.

Why average age of accounts matters

Length of credit history is not one number – it blends the age of your oldest account, the age of your newest account, and the average age across everything you have open. That average age is the piece most people accidentally sabotage.

Here is the math that trips borrowers up. Say you have three cards aged 10, 8, and 6 years – an average of 8 years. Open a brand-new card and you now have four accounts aged 10, 8, 6, and 0, dropping your average to 6 years. You did not do anything “wrong,” but you just diluted one of the factors that took years to build. FICO notes that new accounts lower your average account age, and that this has a larger effect if you do not already have a lot of other credit information – so thin files get punished more than thick ones.

The takeaway: age is a factor you earn by waiting, not one you engineer. Time in the saddle is the only thing that moves it up.

Why opening a new card right before buying backfires

Opening a new account before a mortgage hits you three ways at once, and none of them help:

It lowers your average account age. A zero-month account drags the average down, shaving points off your length-of-history factor.

It adds a hard inquiry and a brand-new tradeline under “new credit.” FICO treats several new accounts opened in a short window as greater risk – the model reads a burst of new credit as possible financial distress.

It can change your debt-to-income picture. This is the mortgage-only consequence. A new account with a minimum payment can move your DTI, and lenders re-check credit before closing (more on that below).

The instinct – “I’ll boost my score by adding credit before I apply” – is exactly backwards during a purchase. The account is too young to help your age, it dings new-credit, and it hands underwriting a fresh liability to reconcile.

Why a healthy credit mix helps – but chasing it is a mistake

Credit mix rewards you for showing you can responsibly juggle different types of credit – revolving cards alongside installment loans like an auto loan or student loan. A borrower with only credit cards, or only an auto loan, is missing part of the picture the model likes to see.

But here is the part the “optimize everything” crowd gets wrong: FICO itself says you should not go open credit types you do not have just to improve your mix. Their own guidance answers the question of whether you should start applying for all the types of credit you don’t currently have with a flat no. Mix is only about 10% of the score, and opening accounts to chase it triggers hard inquiries, lowers your average age, and can look like distress – the risk outweighs the reward for almost everyone.

A healthy mix is something you accumulate naturally over years of normal financial life. It is a nice-to-have, not a lever to yank the week before you apply for a mortgage.

New-credit red flags: why a flurry of accounts reads as distress

New credit is its own factor for a reason. FICO says opening several new accounts in a short period of time represents greater risk – especially for people who don’t have a long credit history. The risk model is built on decades of data showing that people who suddenly open a cluster of new accounts default more often than people who don’t. It cannot tell the difference between “I’m optimizing my credit mix” and “I’m scrambling for cash” – so it treats the pattern conservatively either way.

Two things soften the blow if you must apply for credit:

Rate-shopping protection. FICO groups multiple inquiries for the same purpose – like shopping several mortgage lenders – and treats them as a single event within the shopping window. Cluster your mortgage shopping into a tight window rather than spreading it over months.

FICO also only considers inquiries from the last 12 months when scoring, and many inquiry types – promotional offers, account reviews, and your own credit checks – are ignored entirely. But a mortgage in progress is the one time you do not want to be testing those edges.

The myth that closing an old card erases its history

This is the most common and most damaging myth about credit age, so let’s correct it cleanly: closing a credit card in good standing does not erase its history.

Closed accounts with a positive payment record generally stay on your credit report for up to about 10 years from the date they are reported closed, and those on-time payments keep helping you for that whole stretch. So the “I closed my old card and lost all that history” fear is not immediate.

It eventually shortens your average age. When that closed account finally drops off in about a decade, its age stops counting. That is a long-fuse effect, not a next-month one – but it is real.

The CFPB’s bottom line matches: closing a card may make sense for your situation, but don’t assume it will improve your credit scores. If you are anywhere near a mortgage, the safest move is to leave old accounts open and untouched.

Illustrative behaviors during a home purchase; effects are general and profile-dependent. General – confirm current.

The mortgage layer: don’t touch anything without your loan officer

Everything above gets sharper once you are actually in a loan. Lenders do not pull your credit once and forget it. Fannie Mae’s guidelines have lenders obtain a new credit report and reconcile it against the report used at underwriting to identify any debt that was not accounted for when the loan was underwritten – and a newly discovered liability can mean recalculating your debt-to-income ratio and, in some cases, running the file back through underwriting. A new account you opened “to help your score” can surface at the worst moment and complicate an approval that was already lined up.

That is why the single most important rule of credit age and credit mix during a purchase is behavioral, not mathematical:

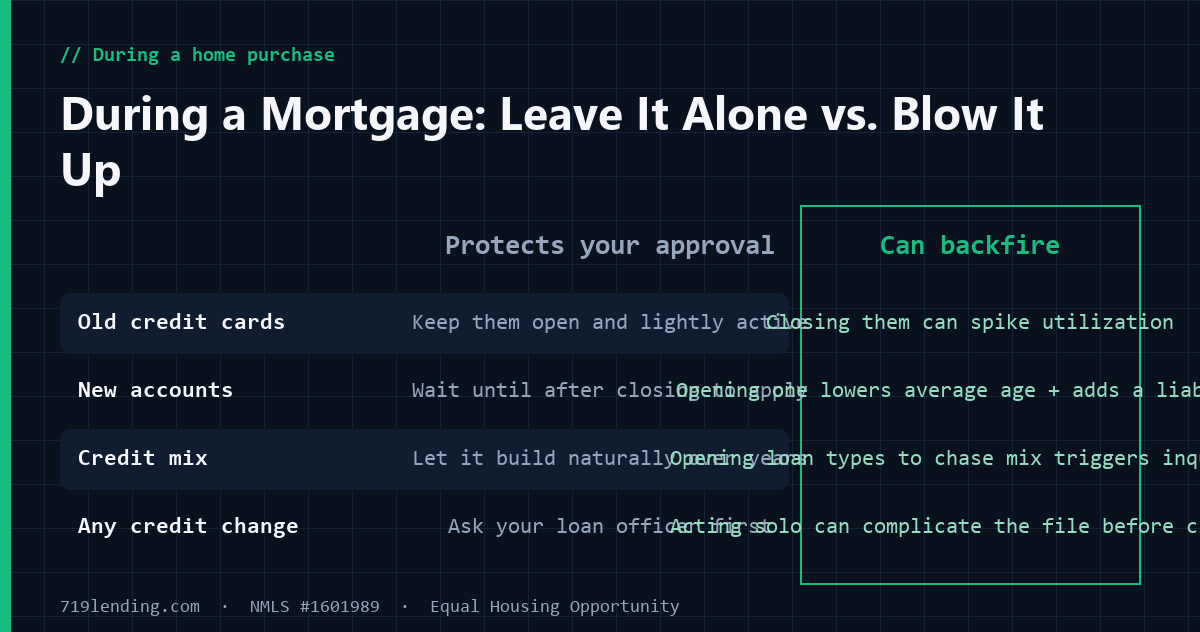

Don’t open new accounts – cards, auto loans, “buy now, pay later,” store financing – while under contract. It dilutes your age, dings new-credit, and can move your DTI.

Don’t close old accounts to “clean up” – it can spike utilization and start the clock on losing that age.

Do ask first. If there is a genuine reason to open or close something mid-process, your loan officer can tell you whether it helps or hurts your file – and time it around the credit pull.

Age and mix are the factors you plant years in advance and then leave alone. The move that actually helps you before closing is protecting what you already built – not chasing a few points you cannot earn in 30 days. A local mortgage broker can map which of your credit factors are worth touching before you apply and which to leave exactly as they are.

Frequently asked questions

Does opening a credit card before buying a house hurt my mortgage application? It usually hurts more than it helps. A brand-new account lowers your average account age, adds a hard inquiry under the new-credit factor, and creates a fresh liability that can change your debt-to-income ratio. Because lenders re-check credit before closing, a new account can also complicate a file that was already approved. Talk to your loan officer before opening anything while you are buying.

Will closing my oldest credit card lower my score? Closing it does not erase the account’s history – a closed account in good standing generally stays on your report for up to about 10 years and keeps helping. The bigger immediate risk is utilization: closing a card removes its limit from your available credit, which can raise your utilization ratio and lower your score. Over the long run, when the account eventually drops off, it can also shorten your average account age.

How much do credit age and credit mix affect my score? As a general FICO breakdown, length of credit history is about 15% and credit mix is about 10%, so together they influence roughly a quarter of the score. FICO is clear that these weights are general and vary by profile – someone new to credit is affected differently than someone with decades of history. Treat the percentages as general, not fixed.

Should I open different types of loans to improve my credit mix before a mortgage? No. FICO explicitly advises against opening credit types you do not have just to improve your mix. Mix is only about 10% of the score, and new accounts trigger inquiries, lower your average age, and can read as financial distress. A healthy mix is something you build naturally over time, not a lever to pull before applying.

How long does it take to improve credit age? There is no shortcut – average account age only rises with time. A new account generally starts to help your length-of-history factor as it seasons, and the benefit grows as it ages. This is why age is called a factor you cannot rush: the only way up is to keep your accounts open and let them mature.

Does rate-shopping for a mortgage hurt my credit through new credit? Much less than people fear. FICO groups multiple inquiries for the same purpose – like shopping several mortgage lenders – and counts them as a single event within the shopping window, so clustering your lender shopping into a tight window limits the impact. Checking your own credit is a soft pull and does not affect your score at all.

This article is general education, not financial, credit, or lending advice, and does not guarantee any credit score change, loan approval, or interest rate. Credit scoring factors, weights, and mortgage guidelines are general and subject to change – confirm current details for your situation. 719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. Last updated June 30, 2026.

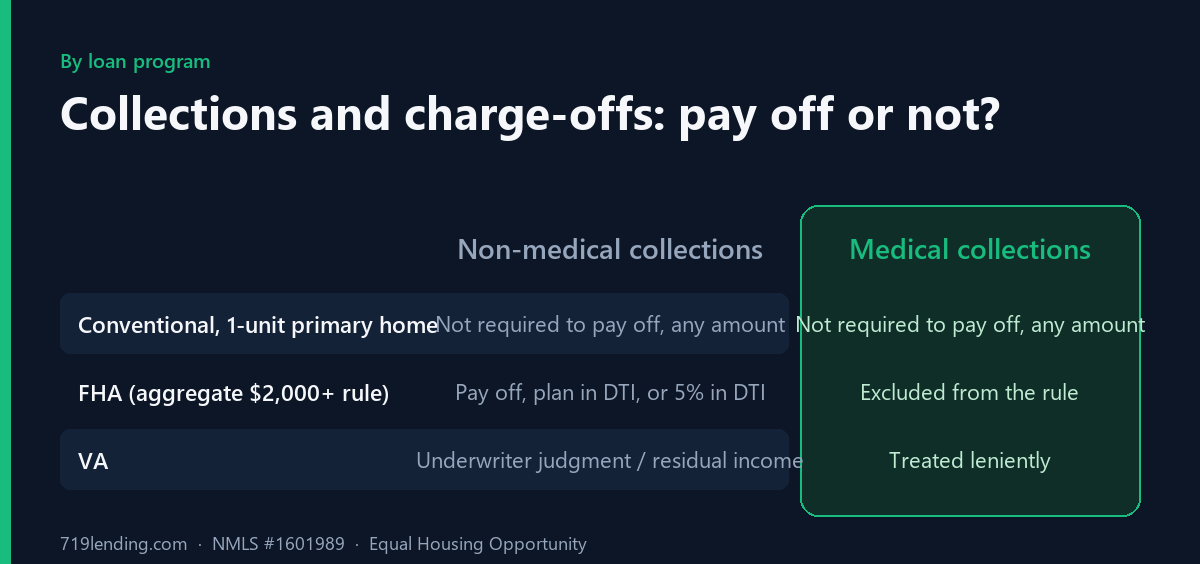

Can you get a mortgage with collections, charge-offs, or medical debt? Usually yes, often without paying them off. Here is how the answer changes by loan program, plus the paying-a-collection trap to avoid. General - confirm current.

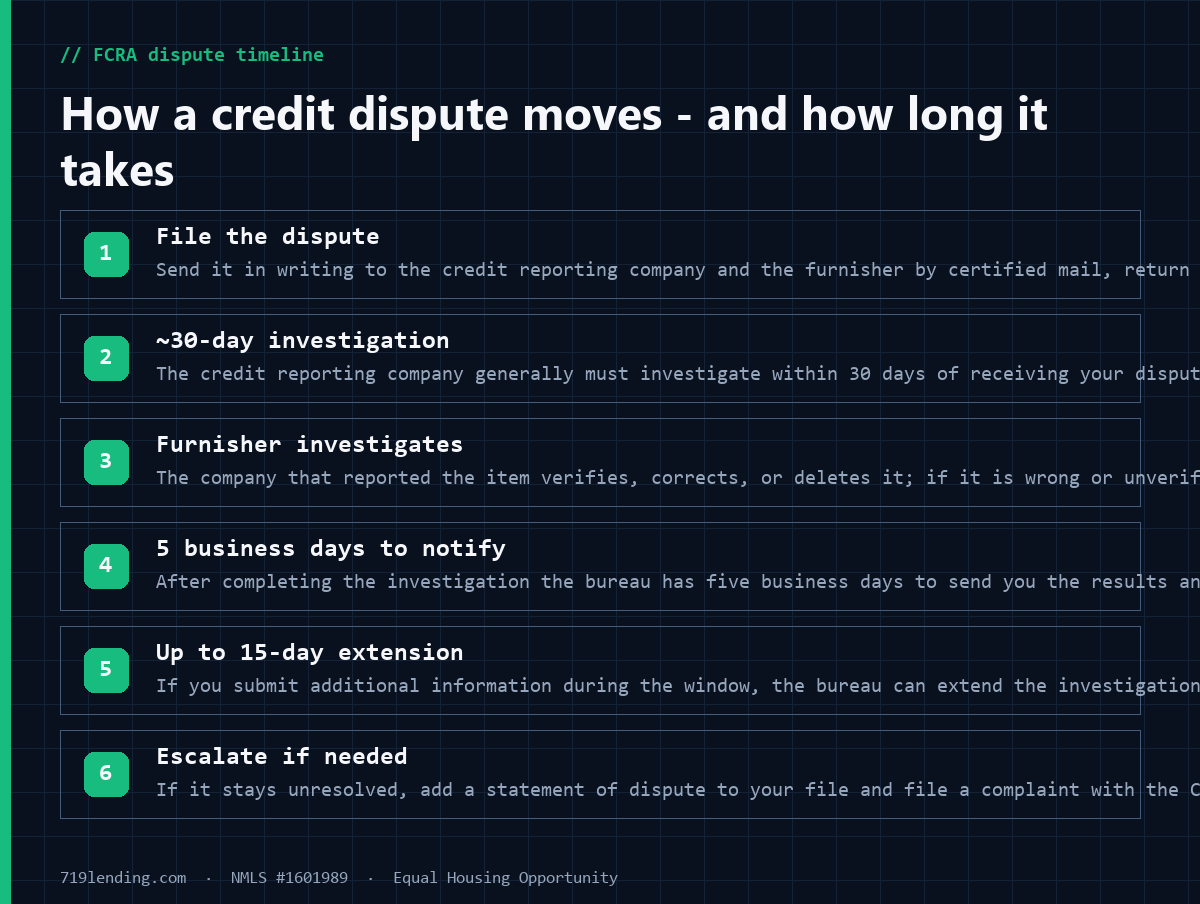

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

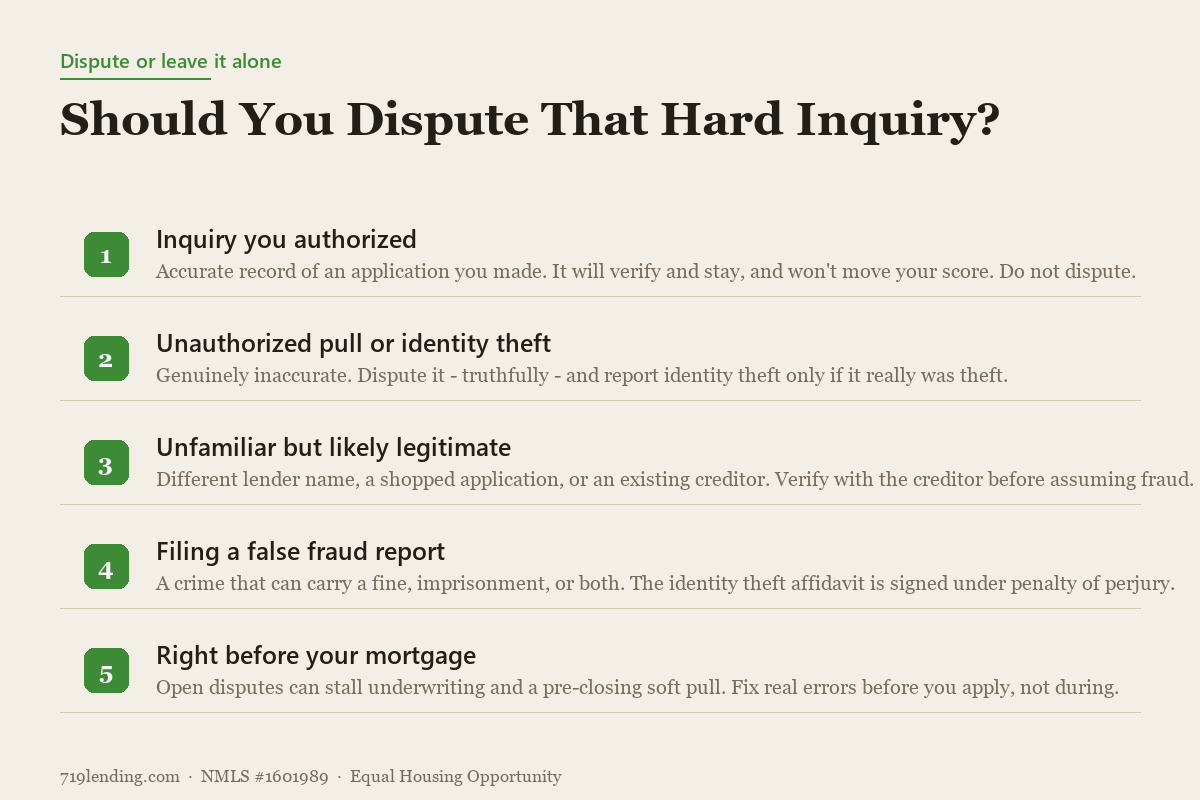

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.