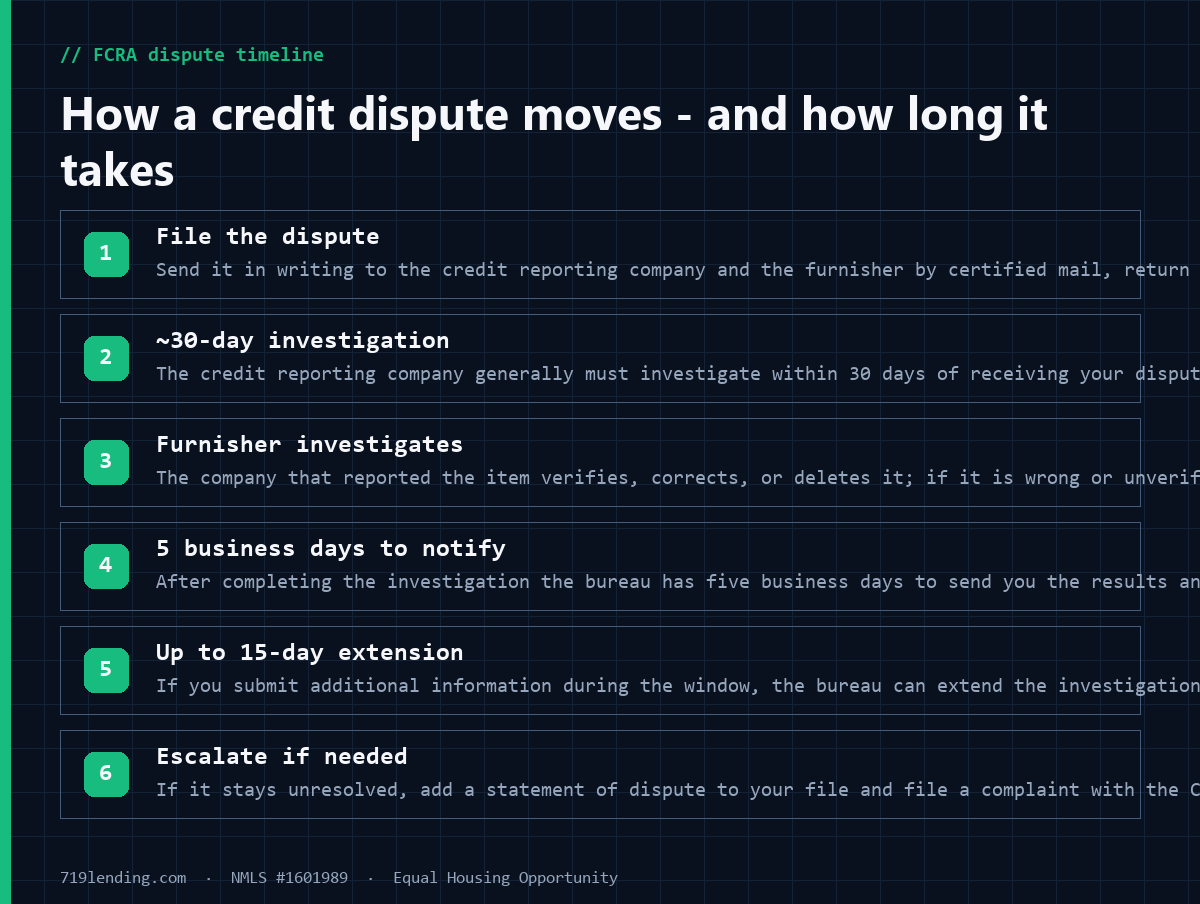

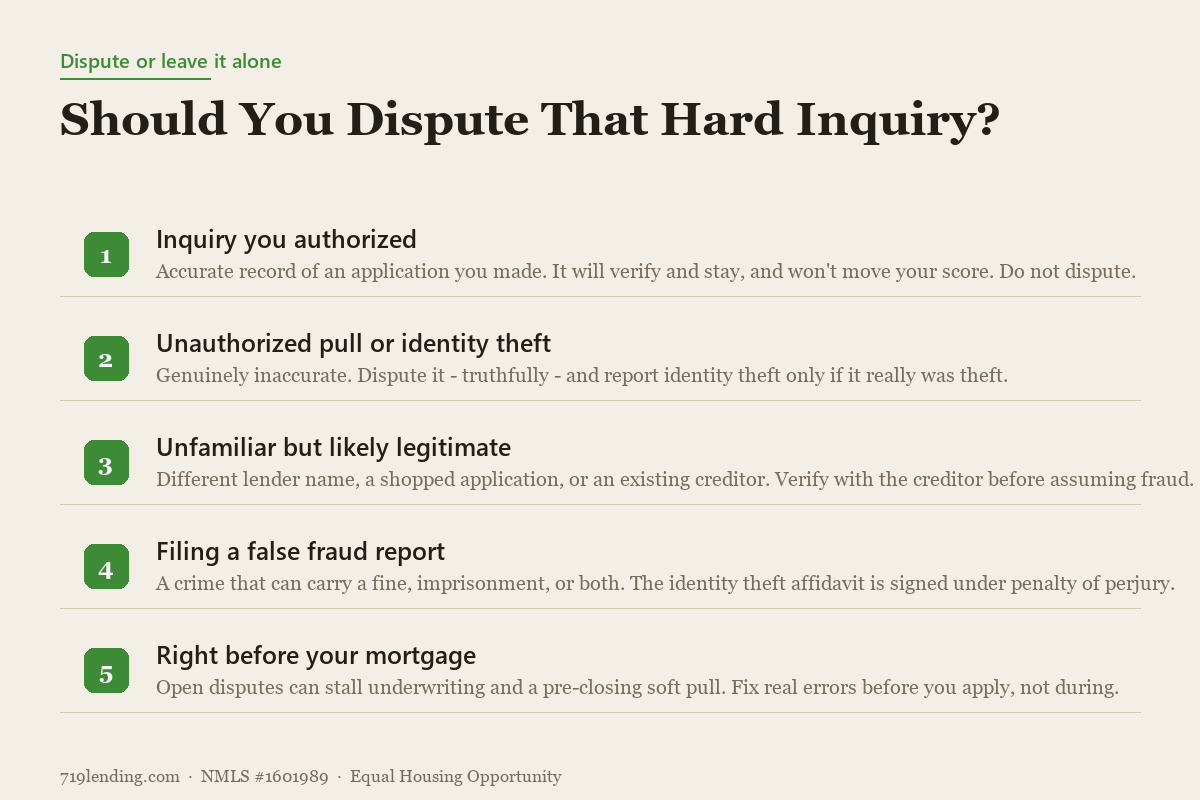

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

How Many Credit Scores Do You Have? (And Why Your Mortgage Uses Just 3)

You do not have one credit score — you have many. Between FICO’s multiple versions (8, 9, 10, and 10T), the separate VantageScore model, and three different credit bureaus, one person can carry well over a dozen possible numbers at the same time. Your mortgage, though, deliberately ignores almost all of them and runs the same proven three every time. That consistency is not a bug — it is the feature that keeps home-loan approvals predictable.

If you have ever pulled your score on a free app, walked into a mortgage conversation, and heard a number 30, 50, even 80 points lower, you are not being tricked. You are simply looking at a different score than the one your loan officer sees. Understanding which scores exist — and why the mortgage industry picks the ones it does — turns that confusing gap into something you can actually plan around. This is the front-door concept behind every other credit question in a home purchase, so we lead with the mortgage angle first.

Last updated: June 30, 2026.

A credit score is a risk model, not a grade

Start here, because it reframes everything. The Consumer Financial Protection Bureau defines a credit score plainly: it is a prediction of your credit behavior — how likely you are to pay a loan back on time — built from the information in your credit reports. It is not a report card and it is not a measure of your character. It is a probability estimate, a lender’s shorthand answer to one question: if we lend to this person, do we get paid back?

Because it is a prediction, there is no single “true” score handed down from on high. Different companies build different prediction models, feed them slightly different data, and get different numbers. All of them are trying to sort higher-risk borrowers from lower-risk ones — they just do the math differently. That is the whole reason you have more than one score, and it is why the mortgage industry had to pick a standard rather than letting every number float.

So how many credit scores do you have?

More than most people would ever guess. The two big scoring companies each publish multiple models, and each model is calculated separately at each of the three bureaus. Here is the realistic landscape:

- FICO base versions. Fair Isaac Corporation maintains several general-purpose models still in circulation — FICO Score 8 (the most widely used), FICO Score 9, and the newer FICO Score 10 and 10T. Older versions linger in specific industries.

- FICO industry-specific versions. On top of the base models, FICO builds tuned versions for auto lending, bankcards, and mortgages. Counting every base and industry variant across all three bureaus, there are well over a dozen distinct FICO scores in active use.

- VantageScore. A separate model entirely, jointly created by the three bureaus, with its own recent versions (3.0 and 4.0). This is almost always the number free apps show you.

- Three bureaus. Equifax, Experian, and TransUnion each hold their own copy of your data, so every model above produces a different result at each bureau.

Multiply models by bureaus and a single consumer can realistically have a dozen or more live scores at any moment — and none of them is “wrong.” They are simply different tools measuring the same underlying credit behavior. So when someone asks how many credit scores do you have, the honest answer is: many. The more useful question for a home buyer is which three a mortgage lender will actually use.

Why your mortgage uses just three (the Classic FICO trio)

When you apply for a conventional home loan, the lender does not pull your phone-app score. Under the rules Fannie Mae and Freddie Mac set for loans they buy, lenders order a three-bureau merged report and pull a specific, older set of FICO models known informally as the “Classic FICO” trio:

- Equifax: Beacon 5.0 (FICO Score 5)

- Experian: Fair Isaac Risk Model V2 (FICO Score 2)

- TransUnion: FICO Risk Score, Classic 04 (FICO Score 4)

Yes, these are intentionally older models — and that is on purpose, not oversight. The government-sponsored enterprises that buy the vast majority of U.S. mortgages standardized on these versions because they have decades of proven performance data behind them. When trillions of dollars in home loans get packaged and sold to investors, everyone in that chain needs to price risk against the same yardstick. Swapping in a brand-new model every couple of years would inject uncertainty into the largest debt market on earth. The “same old three” are tried-and-true, and that stability is exactly what makes mortgage approvals and pricing predictable for you as a borrower.

The tri-merge and the middle score

A mortgage lender pulls all three bureaus at once — the “tri-merge” report — so it sees three separate FICO numbers for you. It does not average them, and it does not cherry-pick the highest. Fannie Mae’s rules direct the lender to use the score that lands in the middle. If your three numbers are 690, 712, and 738, your representative score is 712. The high and the low are set aside. (If two of the three match, that matched number is the middle.)

The middle-score rule is deliberately conservative and deliberately fair: it throws out both the flattering outlier and the punishing one, and lands on the number that best represents your actual credit profile. This is why the single figure your loan officer quotes may not match any score you have seen on your own — it is the median of a specific trio you probably never look at.

What about two borrowers?

When a couple applies together, each borrower gets their own middle score first. Under Fannie Mae’s current rules, the lender then works from the average of the two borrowers’ median scores to evaluate the file. (Separately, note that effective November 16, 2025, Fannie Mae removed the hard 620 minimum representative and average-median score requirement from its automated underwriting — credit is now evaluated through a broader risk assessment rather than a single cutoff. A lender must still pull a score for every borrower, and mortgage insurers or specific programs may keep their own minimums.)

The practical takeaway has not changed: a lower-scoring co-borrower still influences your pricing and qualification, so it is worth knowing both partners’ middle scores before you apply. If one spouse’s credit is dragging the file, there may be a real decision to make about who goes on the loan — a conversation a broker can walk you through.

Why your app score looks so different

Here is the single biggest source of borrower confusion, and it is worth stating flatly: the free score on most banking and credit apps is usually a VantageScore, not a FICO score at all. It is a different model, built by a different company, using different math on the same underlying data. Comparing it to your mortgage FICO score is like comparing a Fahrenheit reading to a Celsius one — both are valid, neither is a lie, but they are not the same scale.

On top of the model difference, your app usually shows a current-generation score (FICO 8/9 or VantageScore 4.0), while your mortgage uses the older Classic FICO trio above. Two layers of difference — different model and different version — easily explain a 30-to-80-point gap. So the tactic is simple: use your free app to watch trends (is my score moving up or down?), but steer your home-buying decisions by the lender-pulled mortgage score, because that is the only number that determines your loan.

Same three today — but change is coming

The Classic FICO trio has been the mortgage standard for decades, but that is finally starting to shift. In July 2025 the Federal Housing Finance Agency directed Fannie Mae and Freddie Mac to let lenders choose VantageScore 4.0 as an alternative to Classic FICO, and by 2026 that option was in place. Two important caveats: the three-bureau tri-merge is still required (FHFA reversed an earlier plan to drop to a two-bureau report), and a lender uses one model or the other on a given loan — not both. Classic FICO remains the score used at most closing tables today.

What this means for you: nothing you need to act on urgently, but a real reason to work with someone who tracks these rules. The score model a lender runs can change a file’s outcome, and the industry is mid-transition. For now, just know the “same old three” are still driving most approvals, and that predictability is working in your favor.

Frequently asked questions

How many credit scores do I actually have? Realistically a dozen or more at any given time. FICO alone maintains several base versions (8, 9, 10, 10T) plus industry-specific ones for auto, bankcard, and mortgage lending, VantageScore is a separate model with its own versions, and every model is calculated separately at Equifax, Experian, and TransUnion. None is the single “real” score — they are different risk models measuring the same behavior. This range is general; the exact count depends on which versions each bureau currently produces.

Which credit score does a mortgage lender use? For conventional loans, lenders pull the Classic FICO trio on a three-bureau merged report: Equifax Beacon 5.0 (FICO 5), Experian Fair Isaac Risk Model V2 (FICO 2), and TransUnion FICO Risk Score Classic 04 (FICO 4). They then use the middle of the three numbers as your representative score. Confirm current program specifics with your lender.

Why is my free app score higher than my mortgage score? Free apps typically show a VantageScore, not a FICO score — a different model built by a different company. Your mortgage uses an older Classic FICO version. Two layers of difference (different model and different version) can easily produce a 30-to-80-point gap. Neither number is fake; they are just different scales.

Do lenders average my three scores or take the highest? Neither. For a single borrower they use the middle (median) of the three bureau scores; the highest and lowest are set aside. For two borrowers, current Fannie Mae rules work from the average of each borrower’s median score.

Is a higher credit score version always better for me? Not necessarily — it depends entirely on which version the lender pulls, and you do not get to choose. A newer model might score you higher or lower than the Classic FICO trio your mortgage actually uses. What matters is the score on the lender-pulled tri-merge, not the one on your app.

Will the mortgage industry stop using Classic FICO? Eventually, likely. As of 2026, FHFA has approved VantageScore 4.0 for use as an alternative to Classic FICO on loans sold to Fannie Mae and Freddie Mac. But it is a lender choice (one model per loan), the three-bureau tri-merge is still required, and Classic FICO is still standard at most closings. This is general and evolving; confirm current requirements when you apply.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, endorsed by, or acting on behalf of any government agency, including the FHA, VA, USDA, FHFA, Fannie Mae, or Freddie Mac. All score ranges, program rules, and figures are general and subject to change — confirm current details with your loan officer. This article is educational and not a commitment to lend or a guarantee of any credit-score outcome, loan approval, or interest rate.

Related Posts