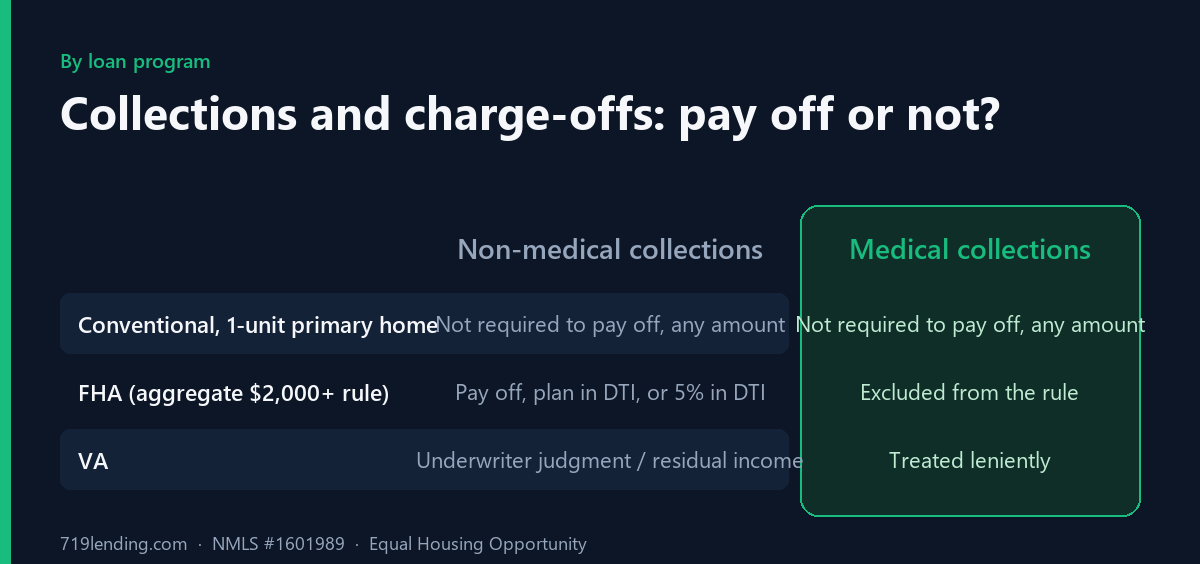

Can you get a mortgage with collections, charge-offs, or medical debt? Usually yes, often without paying them off. Here is how the answer changes by loan program, plus the paying-a-collection trap to avoid. General - confirm current.

What Credit Score Do You Actually Need to Buy a House?

The honest answer to “what credit score do you need to buy a house” is that there are two different questions hiding inside it: what a loan program allows on paper, and what a lender will actually approve and fund. Those are not the same number. Some agencies publish a hard minimum, some publish none at all, and almost every lender adds its own stricter cutoff on top. As a general reference (confirm current), the realistic floors are roughly: VA and USDA have no agency credit-score minimum, FHA allows 580 with 3.5% down (500 to 579 with 10% down), and conventional loans sit around a 620 practical floor. But “allowed” is not “approvable” — and your score only opens the door. Your debt-to-income ratio decides most of what happens next.

We are a mortgage broker in Colorado Springs, and this is one of the most misunderstood questions we field. Borrowers read a single number online, assume it is a pass/fail line, and either count themselves out or expect a guarantee. Neither is how underwriting works. Below we separate the paper minimum from the approvable reality for every major loan type, explain why the published minimums mislead, and show where your score actually stops mattering and your income takes over.

Allowed vs. approvable: the distinction that changes everything

Think of a credit score the way a lender does — not as a grade, but as one input into a risk model that answers a single question: if we lend this money, do we reliably get paid back? A published “minimum” is only the floor at which a loan program will insure or buy the loan. It is not a promise that any given lender will originate at that floor, and it is not the whole approval decision.

Three forces sit between the paper minimum and a funded loan:

- Lender overlays. Individual lenders routinely set their own minimum above the agency floor based on their risk appetite, their investors, and their servicing tolerance. This is why two lenders quote you different “minimums” for the exact same program — one may originate FHA at 580, another only at 620 or 640. Neither is wrong; they simply have different overlays.

- Sellability. Even on a manual underwrite, the loan usually has to be sellable to the agency (Fannie Mae, Freddie Mac) or insurable (FHA, VA, USDA). A lender will not hang onto a loan it cannot move, so its practical cutoff reflects what the secondary market will accept — not just what the rulebook technically permits.

- Score is one factor of many. A qualifying score gets your file reviewed. From there, debt-to-income ratio, down payment, reserves, employment history, and property type carry enormous weight. A 760 with a 55% DTI can be declined; a 640 with a 30% DTI and strong compensating factors can sail through.

So the useful mental model is: the agency minimum tells you whether a program is possible; the lender’s overlay tells you whether this lender will do it; and your full financial picture tells you whether you are actually approvable.

Agency minimum vs. what’s actually approvable, by loan type

Here is the gap laid out program by program. Every figure is general — confirm current, because overlays and agency policy change.

| Loan type | Agency minimum (on paper) | What’s typically approvable (real world) |

|---|---|---|

| VA | No agency credit-score minimum | Lender overlays commonly land around 580 to 640 |

| USDA | No hard minimum score | 640+ runs the automated (GUS) credit path; below 640 typically means manual underwriting |

| FHA | 580 at 3.5% down; 500 to 579 at 10% down | Most lenders start around 580 to 620; sub-580 origination is rare due to overlays |

| Conventional (Fannie/Freddie) | ~620 practical floor | 620 possible, but pricing punishes scores below the mid-600s to ~700 |

| Jumbo (non-agency) | Lender-set, no agency backstop | Commonly 680 to 700+, often higher |

VA loans: no agency minimum, but overlays are real

The VA does not impose a minimum credit score, and its lender handbook is explicit that a lack of credit history is not treated as a negative. Instead, VA underwriting leans on residual income (money left over after major obligations) and compensating factors like significant liquid assets, a low debt-to-income ratio, and long-term employment. That is a fundamentally different philosophy from a hard score cutoff.

But “no VA minimum” does not mean “no minimum.” Because the lender still has to fund and sell the loan, most VA lenders apply an overlay — commonly somewhere in the 580 to 640 range. So an eligible Veteran with a 600 middle score may be told “no” by one lender and “yes” by another, entirely because of overlay differences, not VA rules. If you are using your VA benefit, the practical move is to find a lender whose overlay fits your file rather than assuming a paper “no agency minimum” clears every desk.

USDA loans: no hard floor, but 640 is the dividing line

USDA’s guaranteed program also has no hard credit-score minimum on paper. In practice, 640 is the number that matters. Applicants at 640 or above generally clear the automated underwriting path through USDA’s Guaranteed Underwriting System (GUS), as long as no disqualifying credit indicators are present. Below 640, the file typically drops to a more cautious, manual review where the underwriter documents the full credit history and any mitigating circumstances. USDA is careful to note that GUS itself does not approve loans — it is a risk tool that supports, but does not replace, an underwriter’s judgment.

FHA loans: the widest published range, the narrowest real one

FHA publishes the most explicit thresholds of any program, tied to what it calls the Minimum Decision Credit Score (MDCS):

- Below 500: not eligible for FHA-insured financing.

- 500 to 579: eligible, but capped at 90% loan-to-value — meaning a 10% down payment.

- 580 and above: eligible for maximum financing, which is 96.5% loan-to-value — a 3.5% down payment.

Here is the trap. On paper FHA goes down to 500, but almost nobody originates below 580, and many lenders will not go below 600 or 620. Two reasons: overlays (lenders don’t want the default risk of a sub-580 file), and the practical mismatch of a borrower who has a 500 score also having 10% saved for a down payment. The published 500 figure is real, but for the vast majority of buyers the approvable FHA floor is 580, with lender overlays layered on top. FHA determines your MDCS the same way most programs do — the median of your three bureau scores, or the lower of the two if only two are available.

Conventional loans: 620 on paper, but pricing punishes below the mid-600s

Conventional loans backed by Fannie Mae and Freddie Mac have long treated 620 as the practical floor. Freddie Mac still requires a minimum Indicator Score of 620 for most manually reviewed mortgages. Fannie Mae recently shifted its automated system, Desktop Underwriter, away from a single hard 620 cutoff toward a broader credit-risk assessment for new loan casefiles created on or after November 16, 2025 — but 620 remains the meaningful reference point, especially for manually underwritten and non-DU files, and lenders still price and overlay around it.

The bigger point on conventional is that clearing 620 does not make you competitive. It makes you eligible. Loan-level pricing adjustments mean your rate and mortgage-insurance cost improve in bands as your score climbs — roughly the mid-600s, then 680, 700, 720, and 740+ each tend to move your pricing. The CFPB describes it plainly: the lowest rates go to borrowers in the mid- to high-700s or above, borrowers in the 620 to 680 range generally pay the highest rates and have the fewest choices, and below 620 many borrowers struggle to qualify at all. So on conventional, 620 gets you in the door and the mid- to high-700s gets you the best available pricing.

Jumbo loans: no agency floor, so the lender sets a high bar

Jumbo loans exceed conforming loan limits, so they are not bought by Fannie or Freddie and carry no agency backstop. That means the lender holds more risk and sets the credit bar itself — commonly 680 to 700 or higher, frequently with larger reserve and down-payment requirements. If conventional is where pricing tiers start to bite, jumbo is where the entry bar itself rises.

Whose score counts when there are two borrowers

If you are applying with a co-borrower, the lender does not average your scores in the way people expect. For each borrower, the lender takes that person’s middle of three scores (or the lower of two). Then, for pricing and qualification, conventional loans generally use the lowest of the borrowers’ representative scores. In plain terms: a 760 spouse paired with a 620 spouse means the 620 governs your pricing. You will usually still qualify — but at the worse rate and pricing tier tied to the lower score, not the higher one.

That creates a real strategic decision: apply solo on the stronger score (better pricing, but you lose the second income for debt-to-income purposes) versus apply together (add the income, absorb the pricing hit). There is no universal right answer — it depends on whether you need the second income to qualify. This is exactly the kind of trade-off a broker runs both ways before you lock anything.

Score gets you in the door — DTI decides the rest

Your credit score is famously not the whole story, and here is the part borrowers underestimate: your income is not on your credit report at all. The report shows your debts and payment behavior, not your paycheck. So the single biggest qualifier after your score is your debt-to-income ratio — your monthly obligations divided by your gross monthly income.

This is why a high score is not a golden ticket and a modest score is not a death sentence. A strong score with a stretched DTI can still be declined, because the file cannot show capacity to repay. A middling score with a comfortable DTI, real reserves, and stable employment can be approved, because the compensating factors carry it. Score answers “how has this person handled credit?” DTI answers “can this person actually afford this payment?” Underwriting needs both to say yes.

What this means for your next step

If you take one thing from this: stop treating a single online number as your verdict. Pull your actual scores, know that a lender uses a different mortgage-specific score than a free consumer app, and get a real read on your full file — score, DTI, down payment, and reserves together. A borrower who “doesn’t qualify” at one lender because of an overlay may be perfectly approvable at another, on a different program, at a different price. That is the entire value of shopping the file rather than shopping a rumor. As a broker, that comparison across programs and lenders is the work we do before you ever make an offer.

Frequently asked questions

What credit score do you need to buy a house? There is no single number. On paper, VA and USDA have no agency minimum, FHA allows 580 with 3.5% down (500 to 579 with 10% down), and conventional loans sit around a 620 floor. But “allowed” is not “approvable” — lender overlays and your full financial picture (especially debt-to-income) determine the real answer. General — confirm current.

Can I buy a house with a 500 credit score? Technically FHA permits financing down to a 500 score with a 10% down payment, but almost no lender originates at that level because of overlays and risk appetite. Realistically, most buyers need at least 580 for FHA, and often 600 to 620 depending on the lender. Treat 500 as a paper floor, not a practical one.

Do VA loans really have no minimum credit score? The VA itself sets no minimum credit score and looks at residual income and compensating factors instead. However, individual lenders add overlays — commonly around 580 to 640 — so an eligible Veteran can be approved by one lender and declined by another purely because of overlay differences, not VA rules.

Why do two lenders quote me different minimum scores for the same loan? Because of lender overlays. Each lender adds its own stricter cutoff on top of the agency minimum based on its risk appetite and what its investors will buy. The agency floor is the same; the overlays are not. Shopping lenders is how you find one whose overlay fits your file.

Whose credit score counts if my spouse and I apply together? The lender takes each borrower’s middle of three scores (or lower of two), then generally uses the lowest borrower’s representative score to price and qualify a conventional loan. A high score paired with a low score means the low score governs your rate — so it is worth comparing applying jointly versus solo.

Does a higher credit score get me a lower rate? Generally yes on conventional loans, where pricing improves in bands as your score rises through roughly the mid-600s, 680, 700, 720, and 740+. The CFPB notes the lowest rates go to borrowers in the mid- to high-700s or above. We cannot promise any specific rate — pricing depends on many factors and changes constantly. General — confirm current.

Is my credit score the only thing that matters for approval? No. Your score gets your file reviewed, but your debt-to-income ratio, down payment, reserves, and employment history often decide the outcome. Income is not even on your credit report. A strong score with a high DTI can be declined; a modest score with a low DTI and solid reserves can be approved.

719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by any government agency, including the FHA, VA, USDA, or CHFA. All credit-score thresholds, loan-program guidelines, and pricing references above are general and subject to change — confirm current requirements for your situation. This article is educational and is not a commitment to lend, a credit decision, or a guarantee of any rate, term, or approval. Last updated: June 30, 2026.

Related Posts