A USDA construction loan is a single-close, construction-to-permanent mortgage under the USDA Single Family Housing Guaranteed Loan Program that lets eligible buyers build a new home in a qualifying rural area with $0 down and one closing. Its defining feature is unusual: the government’s Loan Note Guarantee is issued right after the interim construction loan closes, before the house is finished, so the lender is protected from day one. That is a stronger backstop than any other agency construction program offers, but it comes with strict rules on who can build, how the money is held, and where the home can sit. For anyone eyeing the rural fringes of El Paso County, this program is worth understanding in detail.

Core features of the USDA combination construction-to-permanent loan (general — confirm current).

How USDA single-close construction works

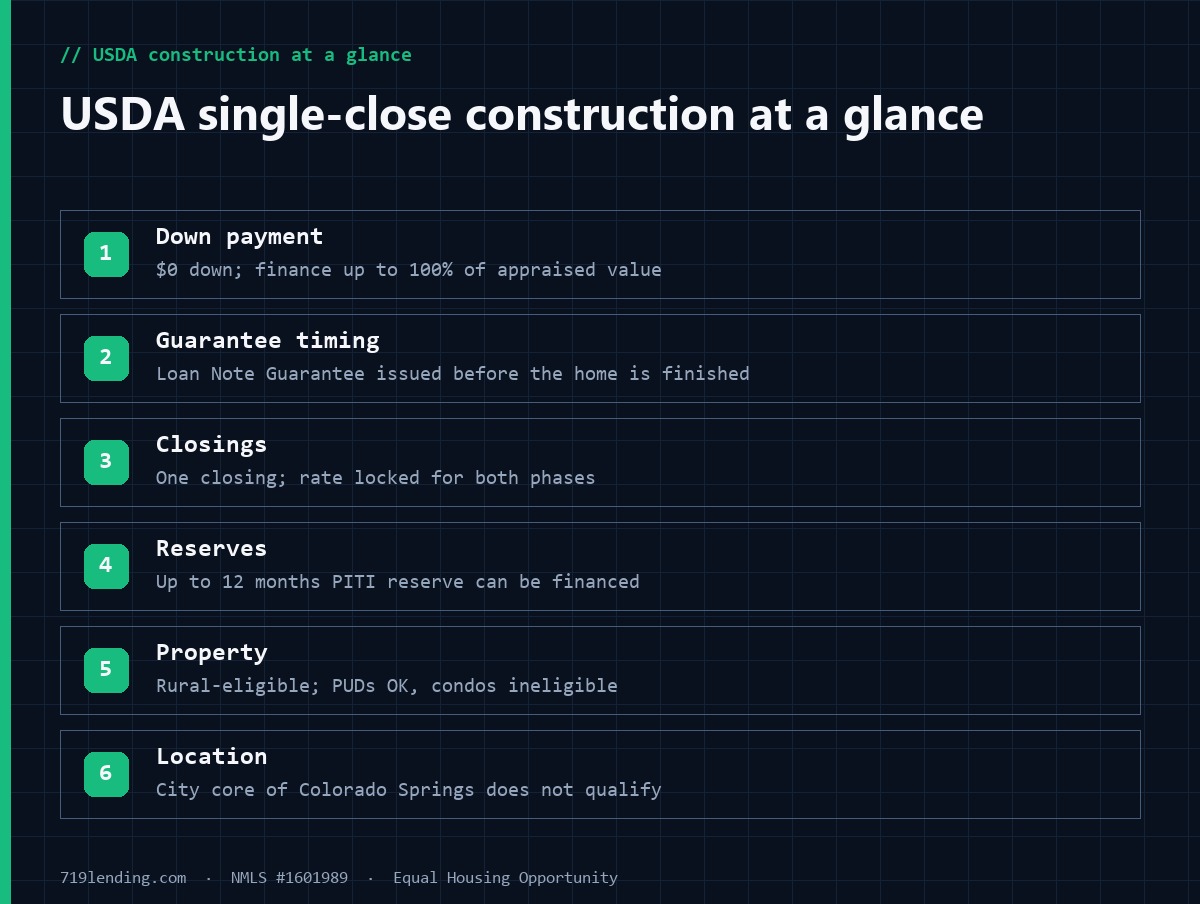

USDA calls this product a “combination construction to permanent loan.” Instead of taking out an interim construction loan and then refinancing into a permanent mortgage — two closings, two sets of fees, two credit and appraisal reviews — you close once. The interim construction period and the long-term mortgage are set up in a single transaction at a single interest rate locked at that closing.

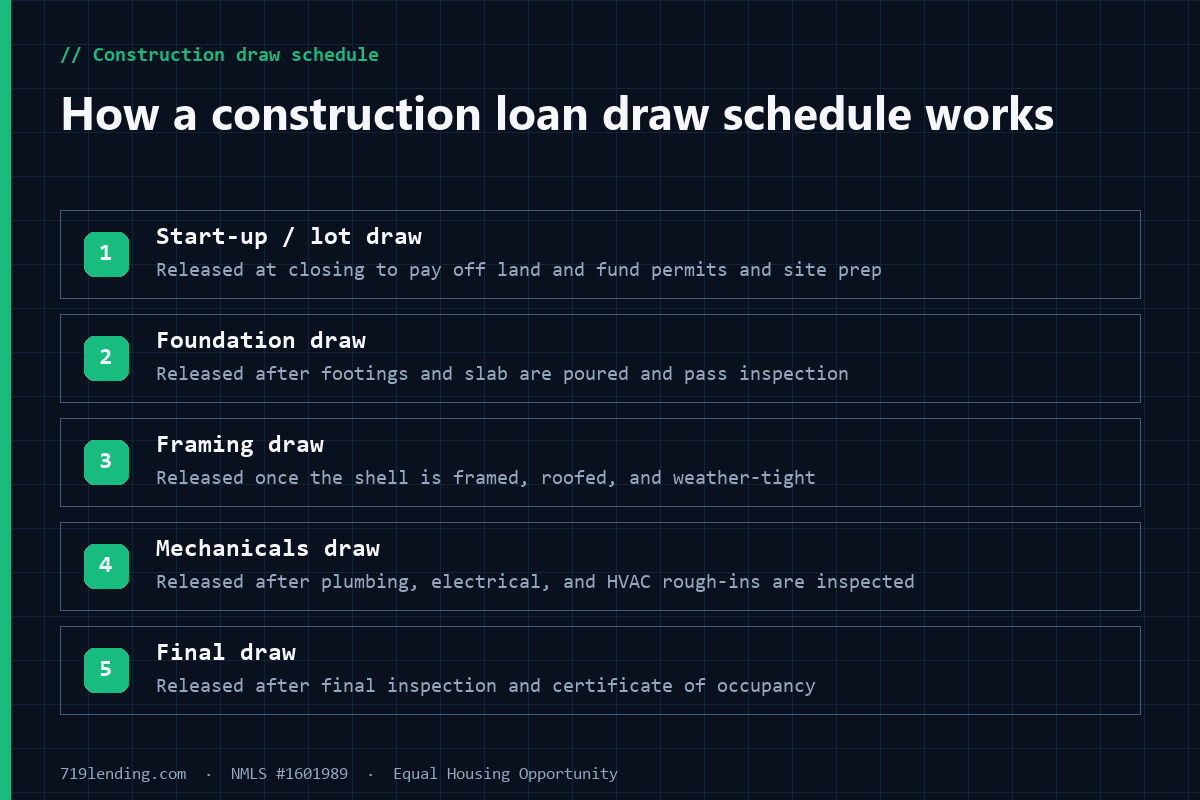

The mechanics resemble the broader idea behind a one-time-close construction loan, but USDA layers on its own rules. During the build, funds are released to the builder through scheduled inspections and disbursements — the same draw structure that governs how construction loan draws work on any construction-to-permanent product. When the home is complete and passes final inspection, the loan either converts automatically or is modified into its permanent amortizing phase, depending on which structure option you chose.

Because it is part of the USDA guaranteed program, the same core borrower rules apply: the property must be in an eligible rural area, household income must fall under the applicable limit, and the home must be your primary residence. If you have never used a rural loan, our overview of how FHA, VA, USDA, and conventional construction loans compare is a useful starting point before you commit to the USDA route.

The guarantee is issued before the home is finished

This is the single most distinctive feature of the USDA program. Under the federal rule at 7 CFR 3555.105, the Loan Note Guarantee is issued after the construction loan closes “without waiting for complete construction,” provided the lender submits acceptable closing documentation. In plain terms, the USDA backstop attaches at the start of the build rather than at the end.

Contrast that with the other agencies. On FHA, VA, and conventional single-close construction programs, the government or investor protection generally does not fully attach until the home is complete and the loan converts to its permanent phase. Because USDA’s guarantee is in place earlier, some lenders are more comfortable extending 100% financing through the riskiest phase of a project — the construction period itself. Our take: this front-loaded guarantee is the quiet reason a no-down-payment construction loan can exist at all, and it is why USDA construction lending, though niche, is not a gimmick.

Zero down payment and 100% financing

USDA is the only widely available program that finances new construction with no down payment. The maximum loan is based on the fair market value of the completed home as determined by a licensed or certified appraiser, and eligible buyers can finance up to 100% of that value. The loan amount may exceed 100% only by the financed upfront guarantee fee, which USDA allows to be rolled into the balance rather than paid in cash at closing.

That structure makes USDA construction financing one of the lowest-cash-to-close ways to build. If down payment is your main obstacle, it is worth comparing against the down payment math on other programs — see how much you need down on a construction loan and, more broadly, how down payments on a house work. All figures here are general — confirm current terms and limits with a licensed loan officer, because rural income limits and the guarantee fee change periodically.

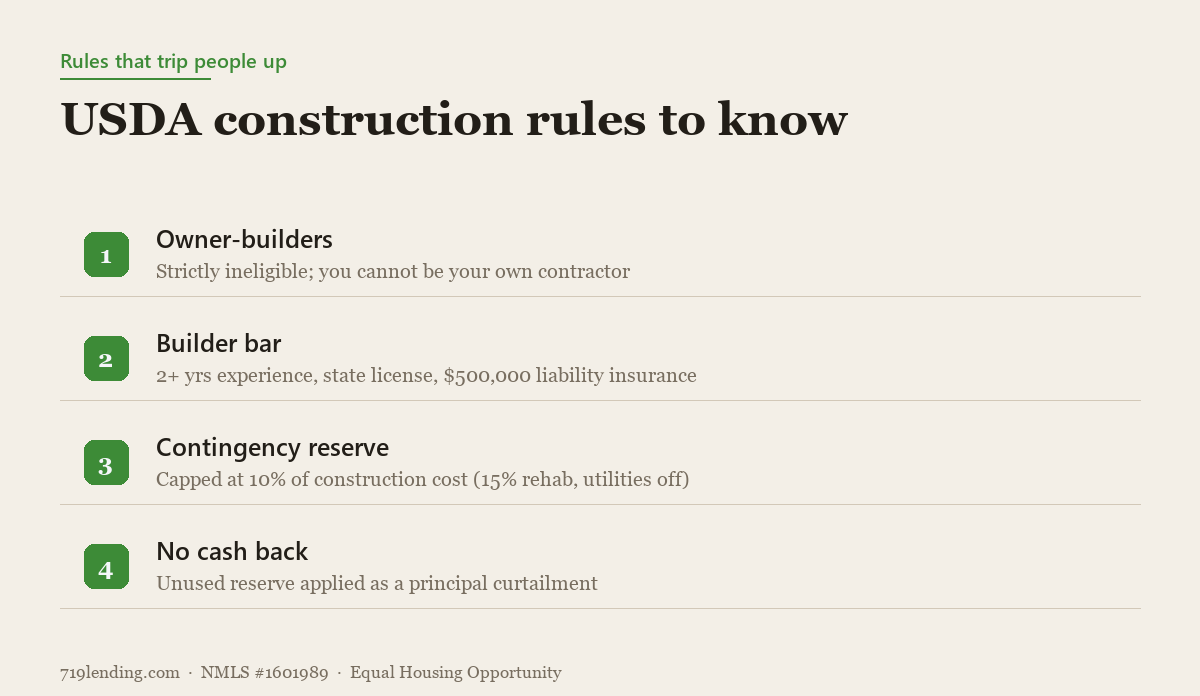

Owner-builders are strictly ineligible

You cannot build your own USDA home. The regulation is explicit: contractors or builders who are constructing their own residence are ineligible, and the borrower may not act as their own general contractor. If you were hoping to save money by managing the project yourself, USDA is not the vehicle — you would need to look at an owner-builder construction loan through a different program.

Beyond barring owner-builders, USDA sets a specific bar for the licensed general contractor you hire. Under 7 CFR 3555.105, the builder must have:

Two or more years of experience building or constructing all aspects of single-family dwellings;

A state-issued construction or contractor license, as required by state or local law; and

Commercial general liability insurance of at least $500,000.

These are not suggestions a lender can waive. If your preferred builder is newer, unlicensed for the work, or under-insured, the file does not qualify. Vetting the contractor early is part of meeting the broader construction loan requirements before you apply.

Non-negotiable USDA rules under 7 CFR 3555.105 and Handbook Chapter 12 (general — confirm current).

Reserves, contingency, and no cash back

USDA lets the loan fund reserves so payments and cost overruns are covered during construction, but it caps them and forbids the borrower from pocketing leftover money.

Contingency reserve. For new construction, the financed contingency reserve is limited to 10% of the cost of construction. For rehabilitation projects where utilities are disconnected, the cap rises to 15% (general — confirm current). This cushion covers unexpected cost overruns during the build.

Payment (PITI) reserve. The lender may fund a reserve of up to 12 months of scheduled principal, interest, taxes, and insurance so the loan stays current while the home is under construction.

No cash back. Borrowers are not to receive funds after closing (with a narrow exception for certain unused prepaid expenses paid with personal funds). Any unused contingency or reserve money is applied as a principal curtailment — it pays down your balance rather than coming back to you as cash.

That last rule surprises people. On some renovation products you might expect a refund of unspent contingency; on USDA, it simply reduces what you owe. For a side-by-side look at how this differs from home-equity or renovation financing, see construction loan vs. HELOC vs. renovation loan.

Two ways to structure the construction phase

USDA offers two structure options, and the choice affects your payments during the build and whether the loan needs a modification when the home is done:

Option 1 — Interest-only during construction, then reamortize. You make interest-only payments (typically drawn from the funded reserve) while the home is being built. When construction finishes, the loan is modified and reamortized into its permanent, fully amortizing payment.

Option 2 — Amortizing PITI with a payment reserve. You make full principal-and-interest-plus-escrow payments from the start, drawn from the funded PITI reserve during construction. Because the loan is already amortizing, no loan modification is required when the home is complete.

Option 2’s appeal is that it avoids a post-completion modification, which is one reason USDA enhanced the program to support it. The right choice depends on your cash flow and how your lender manages the file.

Construction timelines and property types

USDA expects the build to move on a defined schedule. The construction phase generally may not exceed 12 months for new construction, and up to 10 months for rehabilitation projects (general — confirm current). Building a home is rarely instantaneous, so understanding a realistic construction loan timeline before you start helps you stay inside USDA’s window.

Property type matters just as much as the schedule (property-type eligibility below is general — confirm current):

Property type

USDA combination construction eligibility

Single-family detached (site-built)

Eligible

Planned Unit Development (PUD)

Eligible

New manufactured home (HUD code, permanent foundation)

Eligible with conditions

Condominium — including detached and site condos

Ineligible

The condo exclusion is written directly into the rule: condominiums, including detached condominiums and site condominiums, are ineligible for combination construction and permanent loans. PUDs, by contrast, are generally eligible under USDA program guidance (confirm current). If a manufactured home is your goal, note that USDA has its own conditions — our guide to the manufactured home construction loan covers those specifics.

Where you can build in and around Colorado Springs

USDA construction loans only work on property in an eligible rural area, and that geography is the deciding factor for most Colorado Springs-area buyers. The city core of Colorado Springs does not qualify — it is far too densely developed to meet USDA’s rural definition. But large parts of eastern and northern El Paso County do qualify, and that is where this program shines.

Communities and fringe areas toward Calhan, Peyton, and Ellicott, along with stretches of the county’s rural east and north, frequently fall inside eligible USDA territory, while Fort Carson and the built-up areas along the I-25 corridor generally do not. Eligibility is drawn parcel by parcel and can change year to year, so the only reliable move is to check the official USDA property eligibility map for the exact address before you fall in love with a lot. Do not assume a rural-feeling address qualifies — verify it.

If your target parcel turns out to be ineligible, or if income limits are a concern, you are not out of options. Many Colorado Springs buyers who cannot use USDA end up with an FHA loan in Colorado or, if they have served, a VA loan. First-time buyers should also review Colorado first-time home buyer programs, which can pair with several construction and purchase paths.

Is a USDA construction loan right for you?

The USDA single-close construction loan is a genuinely powerful tool for the right buyer: someone building a modest primary home on eligible rural land in eastern or northern El Paso County, with income under the limit and a licensed, experienced, well-insured builder lined up. The $0-down structure and single closing are hard to beat.

It is not the right tool if you want to build inside Colorado Springs proper, act as your own contractor, build a condo, or earn back unused funds in cash. In those cases a conventional or FHA construction path usually fits better. Because the eligibility, income, and builder rules are unforgiving, working with a broker who runs these files matters. As a local mortgage broker in Colorado Springs, 719 Lending can pre-check an address on the USDA map, confirm your income eligibility, and vet a builder before you spend money on plans.

Frequently asked questions

Do USDA construction loans really require no down payment? Yes. USDA finances up to 100% of the completed home’s appraised fair market value, and the balance may exceed 100% only by the financed upfront guarantee fee. It is the only widely available new-construction program with a true $0-down option (general — confirm current).

When does the USDA guarantee take effect — before or after the home is built? Before. Under 7 CFR 3555.105, the Loan Note Guarantee is issued after the construction loan closes without waiting for complete construction. That early backstop is unique among agency construction programs and is a key reason no-down-payment construction financing is possible.

Can I be my own builder on a USDA construction loan? No. Owner-builders are strictly ineligible, and you cannot act as your own general contractor. Your builder must have at least two years of single-family construction experience, a state-issued contractor license, and at least $500,000 in commercial general liability insurance.

What happens to leftover contingency or reserve money? It is not refunded to you. USDA prohibits cash back to the borrower, so any unused contingency or payment reserve is applied as a principal curtailment that reduces your loan balance.

Can I build a home in Colorado Springs with a USDA construction loan? Not in the city core — it does not meet USDA’s rural definition. However, eligible rural areas of eastern and northern El Paso County, near communities like Calhan, Peyton, and Ellicott, often qualify. Always confirm the specific parcel on the official USDA property eligibility map before proceeding.

Are condos eligible for USDA construction financing? No. Condominiums — including detached condominiums and site condominiums — are ineligible for USDA combination construction and permanent loans. Single-family detached homes and PUDs are eligible.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. Loan programs, figures, income limits, and area eligibility are general — confirm current details with a licensed loan officer; approval is subject to program guidelines and underwriting. Last updated: July 2026.

How construction loan money is released: draws, inspections, written borrower approval, interest reserves, and contingency reserves — with FHA, VA, USDA, and conventional rules explained.

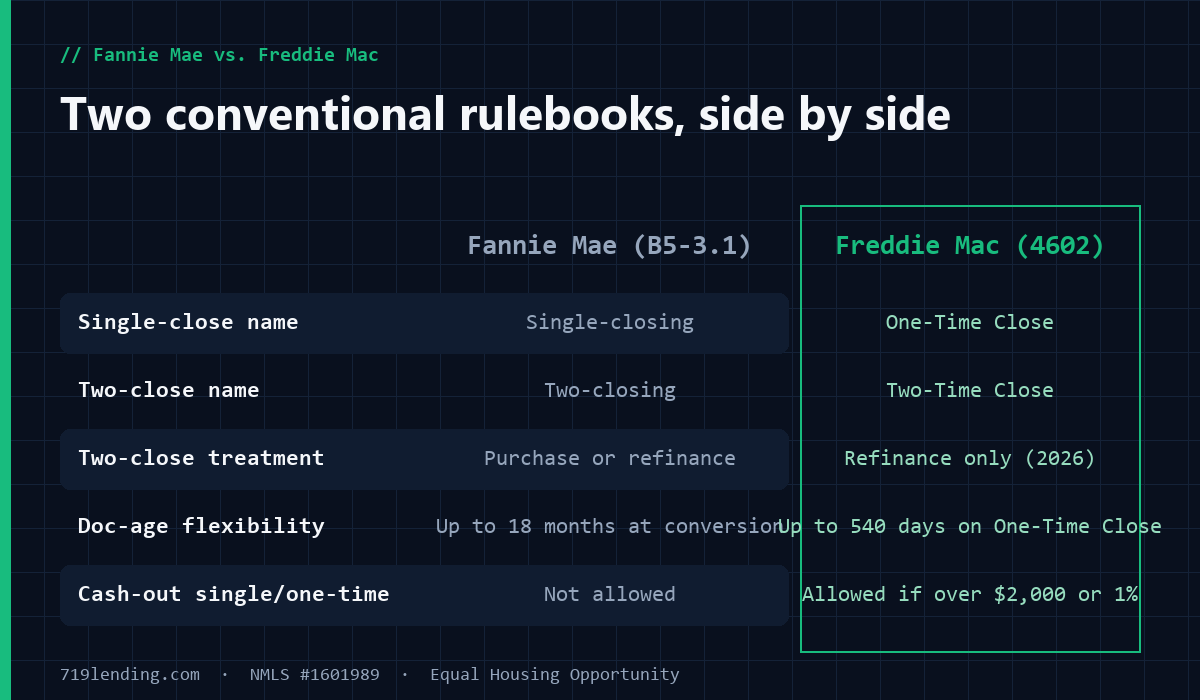

How conventional construction-to-permanent loans work under Fannie Mae (Selling Guide B5-3.1) and Freddie Mac (Guide 4602), with 2026 rule changes, for Colorado Springs builders.

How VA construction loans let eligible Colorado Springs veterans build a home with $0 down and no monthly mortgage insurance. One-time close vs two-time close, draws, funding fee, and the 2025 builder-ID change explained.