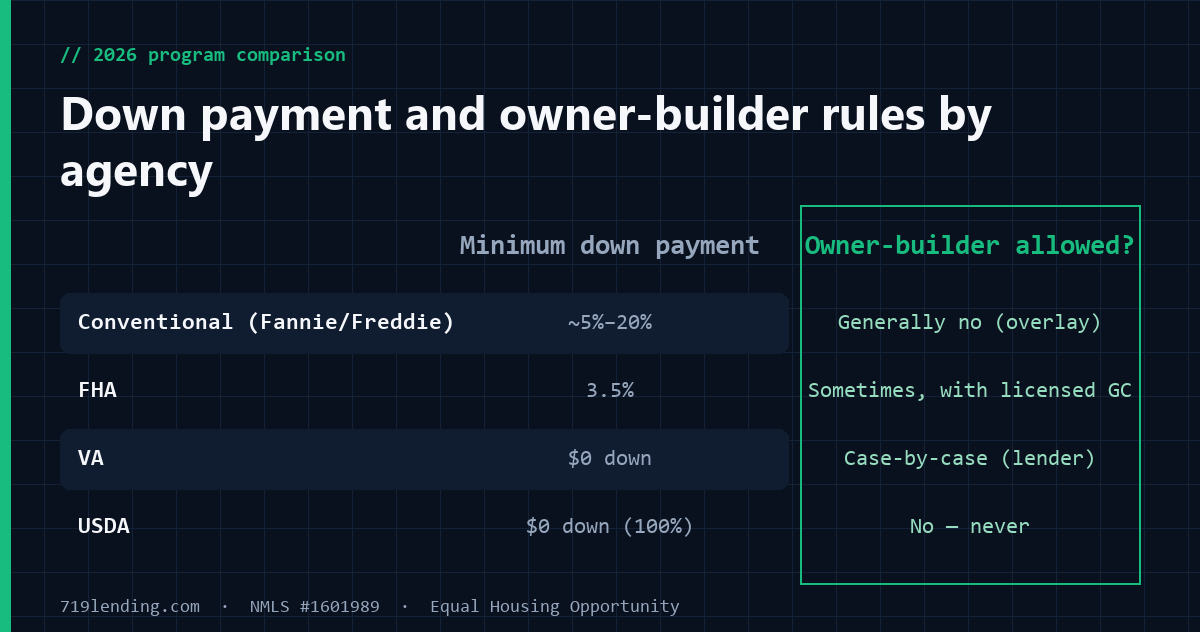

The five main construction-loan programs differ most on four things: how much you put down, whether it is one closing or two, when the government backing actually attaches to your loan, and whether you can act as your own builder. In short — conventional (Fannie Mae/Freddie Mac) runs roughly 5%–20% down; FHA is 3.5% down; VA and USDA can be $0 down. USDA is the outlier that guarantees the loan right after the interim closing, before your house is finished, while Fannie, Freddie, FHA, and VA all wait for completion and a final inspection or certificate of occupancy. And only some programs let you swing your own hammer. This is the hub page for our Colorado Springs construction-loan library; every figure below was checked against the agency’s own guide, and each program links to its own deep-dive.

Building in El Paso County — whether it is a custom home off Highway 115, a lot in Falcon, or new construction near Fort Carson — usually starts with the same question: which loan program fits? Below is the side-by-side, followed by a short plain-English breakdown of each program and how to choose. For the bigger picture, start with our construction loans in Colorado pillar, and if you want the mechanics of one-versus-two closings, see our guide on the one-time close vs. two-time close construction loan.

USDA construction loans” />Minimum down payment and owner-builder eligibility by program. General, confirm current.

The 2026 construction loan comparison table

Figures are general and current as of July 2026; confirm current terms and your own eligibility with a licensed loan officer, because agency guides update frequently (Freddie Mac’s two-time-close and delivery updates, for example, took effect for applications received on or after February 4, 2026).

Program

Minimum down payment

Closings

When the backing attaches

Owner-builder allowed?

Conventional (Fannie Mae)

~5% (as low as 3% on some products); 20% avoids PMI

One-time (single-closing) or two-closing

At delivery, after construction is complete with a final inspection or certificate of occupancy

Lender overlay — generally no

Conventional (Freddie Mac)

~5%–20% depending on the underlying product

One-Time Close or Two-Time Close

Loan cannot be sold to Freddie until construction is finished

Lender overlay — generally no

FHA

3.5% (96.5% max LTV)

One-Time Close (construction-to-permanent)

Permanent mortgage amortizes after the later of final inspection or CO

Sometimes, with a licensed general contractor and lender approval

VA

$0 down

One-Time Close (construction/permanent)

Loan Guaranty Certificate is not issued until a clear final compliance inspection is received

No — a VA-registered, licensed builder is required

Loan Note Guarantee can be requested right after the interim closing, before completion

No — applicants may not build their own home

Two rows in that table do the most work. First, the down-payment column is why so many Colorado Springs veterans and rural buyers gravitate to VA and USDA — both can be built with nothing down, subject to the lender approving the borrower, the builder, the budget, and the as-completed value. Second, the “when the backing attaches” column is the single most misunderstood point in construction lending, so it gets its own section below.

When each agency’s guarantee or purchase actually happens

This is the detail that trips up even experienced borrowers, and it changes how much risk your lender carries during the build:

USDA — before completion. Under the USDA single-close program, the lender may request the Loan Note Guarantee before the work is complete, without waiting for the home to be finished, provided the program’s conditions are met. That early guarantee is precisely why lenders will extend 100% financing with no down payment on a house that does not physically exist yet.

Fannie Mae — at delivery, after completion.Fannie Mae’s Selling Guide (B5-3.1) requires all construction work to be completed, with an Appraisal Update and/or Completion Report (Form 1004D) certifying completion, before the mortgage is delivered.

Freddie Mac — after construction finishes. Freddie Mac’s guide is explicit that the loan cannot be sold until construction is complete, and the lender must provide evidence of completion.

FHA — permanent phase begins after final inspection or CO. On an FHA construction-to-permanent loan, amortization of the permanent mortgage begins no later than the first of the month following 60 days from the final inspection or issuance of the certificate of occupancy, whichever is later.

VA — Loan Guaranty Certificate after a clear final inspection. Per the VA Lender’s Handbook (Pamphlet 26-7, Chapter 7), although the loan is normally considered guaranteed upon closing, the Loan Guaranty Certificate will not be issued until a clear final compliance inspection report has been received by VA.

The takeaway: USDA is the only one of the five where the federal backing can be locked in at the interim close. For the other four, the paperwork that makes the loan salable or guaranteed comes at the finish line.

Conventional construction loans (Fannie Mae and Freddie Mac)

Conventional is the most flexible program and the one most Colorado Springs custom builds actually use. Fannie Mae’s single-closing construction-to-permanent structure caps the construction loan period at no single period of more than 12 months and a total period not exceeding 18 months — and Fannie states plainly that “exceptions to the 12-month and 18-month periods will not be granted.” How the loan is classified depends on lot ownership: it is a purchase when the borrower is not the owner of the lot at the first advance of interim financing, and a limited cash-out refinance when the borrower held legal title to the lot before that first advance. Cash-out refinances are not eligible on single-closing transactions.

Fannie also offers a genuinely useful documentation break. Credit and income documents may be more than four months but not more than 18 months old at conversion to permanent financing, provided the loan was underwritten through Desktop Underwriter with an Approve/Eligible recommendation and the LTV, CLTV, and HCLTV ratios do not exceed 95%. Freddie Mac allows an even longer window on One-Time Close loans — income, employment, and credit documentation may be dated up to 540 days before the effective date of permanent financing when its conditions are met.

Freddie Mac’s Feb. 4, 2026 update (effective for applications received on or after that date) refined its delivery instructions for both One-Time Close (including with a modification agreement) and Two-Time Close transactions. On a two-close structure, the permanent loan is generally treated as a refinance when the borrower already owns the land before the interim construction financing closes. Down payments run roughly 5%–20%; putting 20% down is how borrowers avoid private mortgage insurance. Read the full breakdown on our conventional construction loan page.

FHA construction-to-permanent loans

FHA is the low-down-payment option that still allows some owner-builder flexibility. The minimum required investment is 3.5% of the adjusted value, and the maximum loan-to-value on a purchase is 96.5%. FHA uses a One-Time Close construction-to-permanent structure, and amortization of the permanent mortgage begins no later than the first of the month following 60 days from the final inspection or issuance of the certificate of occupancy, whichever is later. FHA can permit a borrower to act as their own contractor in limited situations with a licensed general contractor and lender sign-off, but most lenders in practice require a professional builder. For Colorado Springs buyers weighing FHA generally, our FHA loans in Colorado guide covers credit, MIP, and county loan limits; the construction-specific mechanics live on our FHA construction loan page.

VA construction loans

VA is the strongest program for eligible veterans — $0 down — but it does not let you build your own home. The VA construction/permanent loan is closed before construction starts, with proceeds covering the land and the balance escrowed and paid to the builder in draws. Because payments do not begin until construction is complete, the VA Lender’s Handbook allows the initial payment on principal to be postponed up to one year if necessary. The loan is considered guaranteed upon closing, but the Loan Guaranty Certificate is only issued after VA receives a clear final compliance inspection report. The builder must be VA-registered and licensed, so the do-it-yourself path is effectively closed. Fort Carson and Peterson-area service members can compare the standard purchase route on our VA loan in Colorado Springs page, and the build-specific details on our VA construction loan in Colorado Springs page.

USDA construction loans

USDA is $0 down for eligible rural buyers, guarantees early, and is the strictest on who builds. The single-close combination construction-to-permanent loan provides up to 100% financing with no down payment for households at or below 115% of area median income in eligible rural areas — and much of El Paso County outside the urban core qualifies. The construction period is generally about 12 months, and the lender may request the Loan Note Guarantee before the work is complete. The trade-off is rigidity: applicants may not act as their own contractor or build their own home (applicants who build their own homes cannot provide the required self-warranty), and condominiums — including detached and site condominiums — are ineligible for the combination construction loan. See our USDA construction loan page for eligibility maps and income limits.

How the programs differ on builders, property types, and documents

Beyond the headline numbers, several finer rules decide which program will actually work for your project:

Owner-builder: USDA prohibits it and VA effectively requires a registered, licensed builder; FHA may allow it with a licensed GC and lender approval; conventional treats it as a lender overlay that is usually declined.

Property type: USDA excludes condominiums from combination construction financing; Fannie and the government programs treat attached condos, co-ops, and manufactured homes with extra conditions, so verify eligibility before you fall in love with a plan.

Document age at conversion: Freddie Mac allows up to 540 days on One-Time Close; Fannie allows up to 18 months at conversion when the loan is DU Approve/Eligible and the LTV is 95% or less. These windows matter on long builds where the original approval could otherwise go stale.

Construction timeline: Fannie’s single-closing cap is 12 months for any single period and 18 months total; USDA new construction is generally 12 months.

Our take: for most Colorado Springs custom builds where the borrower has 10%–20% to put down, a conventional one-time-close loan is usually the cleanest path because of its flexible product mix and documentation windows. Eligible veterans should almost always price the VA option first for the $0-down and payment-postponement benefits, and rural buyers who can live with a professional builder and no condos should look hard at USDA. FHA is the natural middle ground for a lower-down-payment build with a bit more owner-builder latitude. That is a general framework, not advice for your file — the right answer depends on your credit, income, the lot, and the builder.

A quick framework for narrowing construction programs. General, confirm current.

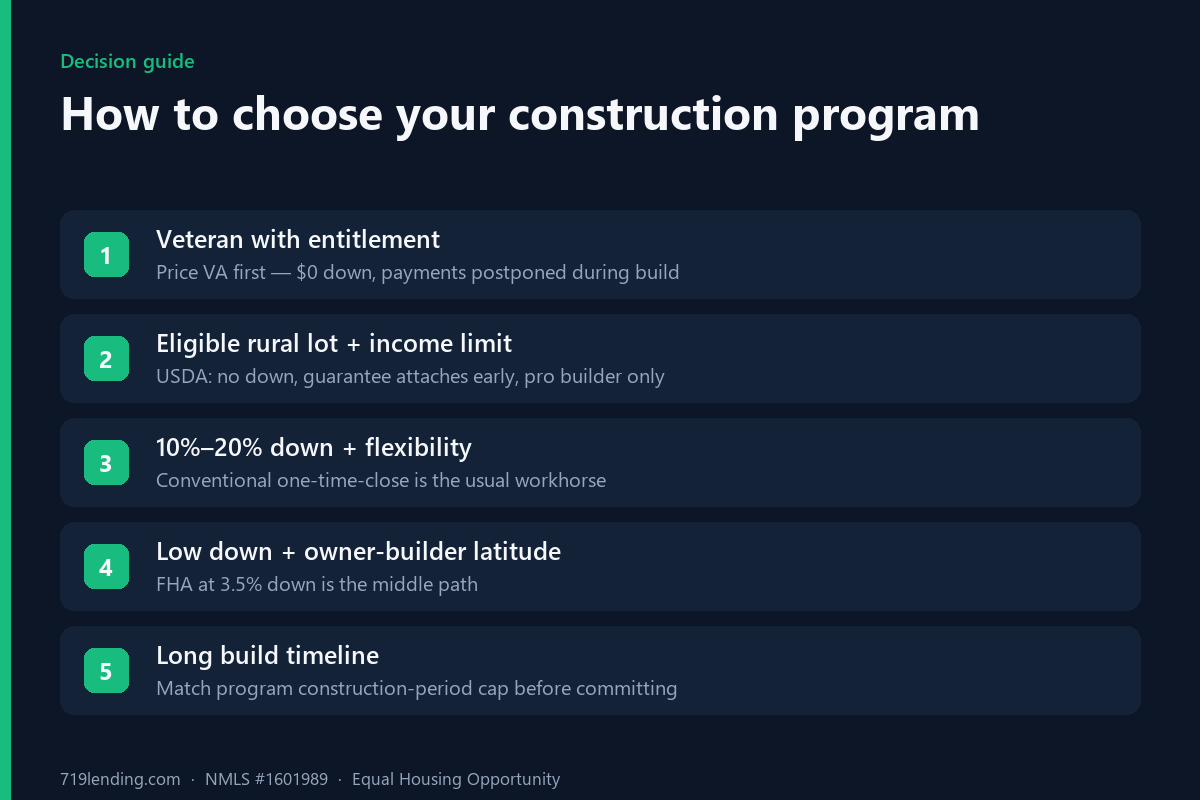

How to choose your construction program in Colorado Springs

Work through these questions in order and the field narrows quickly:

Are you a veteran with entitlement? Price VA first — $0 down and postponed payments during the build are hard to beat.

Is the lot in an eligible rural area and your income within limits? USDA’s no-down, guarantee-early structure is compelling if you will use a professional builder.

Do you have 10%–20% to put down and want product flexibility? Conventional (Fannie or Freddie) is usually the workhorse.

Do you want a low down payment with some owner-builder latitude? FHA at 3.5% down is the middle path.

How long will the build take, and who is building it? Match your timeline to the program’s construction-period cap and its owner-builder rule before you commit.

Not sure where you land? A quick conversation with a local broker can rule programs in or out in minutes. Talk to our team through our mortgage broker in Colorado Springs page, and if you are still early, our building a home in Colorado Springs overview walks through the whole process from lot to move-in.

Frequently asked questions

What is the lowest down payment on a construction loan? VA and USDA construction loans can be built with $0 down for eligible borrowers — VA for qualifying veterans, USDA for eligible rural buyers within income limits. FHA requires 3.5% down, and conventional programs generally run about 5%–20%. All figures are general; confirm current terms with a licensed loan officer.

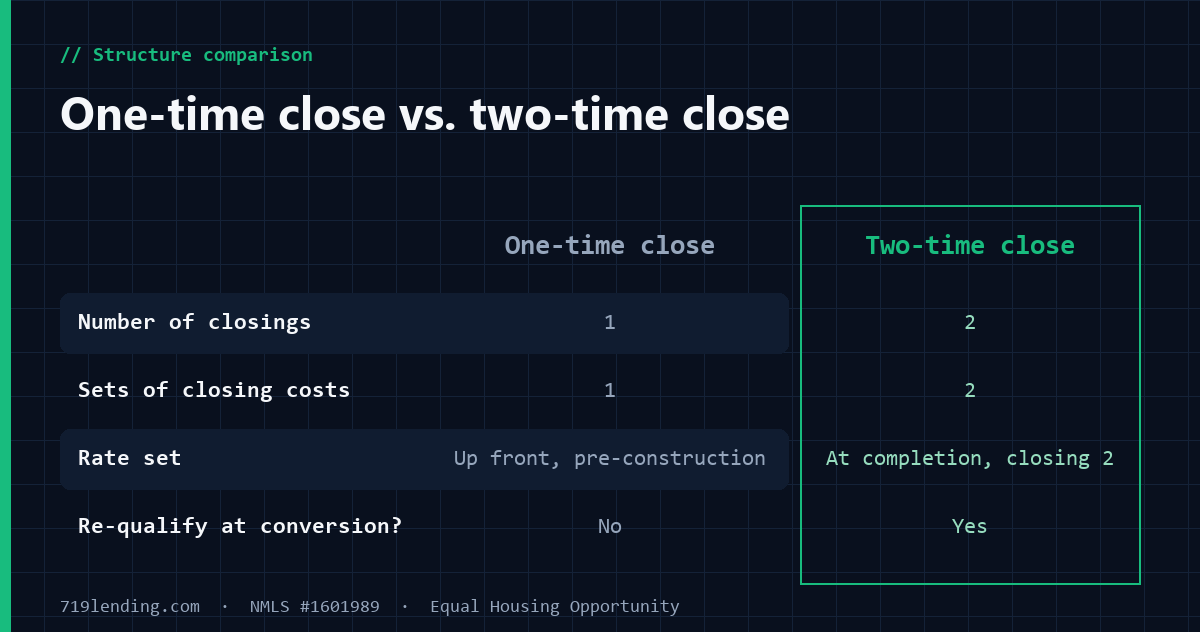

What is the difference between a one-time close and a two-time close construction loan? A one-time close (single-closing) wraps construction and permanent financing into a single closing that converts automatically when the home is finished. A two-time close uses two separate closings, and on Freddie Mac’s structure the permanent loan is generally treated as a refinance when the borrower already owns the land. See our dedicated comparison for the trade-offs.

Can I be my own general contractor on a construction loan? It depends on the program. USDA prohibits applicants from building their own homes, and VA effectively requires a VA-registered, licensed builder. FHA can allow a borrower to act as their own contractor in limited cases with a licensed GC and lender approval, while conventional lenders usually decline owner-builder arrangements as an overlay.

When does the government guarantee or purchase happen on a construction loan? USDA is the only program where the lender can request the Loan Note Guarantee right after the interim closing, before the home is complete. Fannie Mae, Freddie Mac, FHA, and VA all attach their backing at or after completion — Fannie and Freddie at delivery after a completion report, FHA when the permanent phase begins after the later of final inspection or certificate of occupancy, and VA when a clear final compliance inspection is received.

How long can a conventional construction loan take to build? Fannie Mae’s single-closing construction-to-permanent loan allows no single construction period of more than 12 months and a total period not exceeding 18 months, and states that exceptions to those limits will not be granted. USDA new construction is generally about 12 months.

Do condominiums qualify for USDA construction loans? No. USDA excludes condominiums — including detached and site condominiums — from combination construction-to-permanent financing. If you are building a condo unit, you will need a different program.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. Rates, figures, and program terms are general — confirm current terms and your eligibility with a licensed loan officer; this is not a commitment to lend. Last updated: July 2026.

One-time close vs. two-time close construction loans explained for Colorado Springs buyers: closings, costs, rate exposure, re-qualification, and which programs use which.

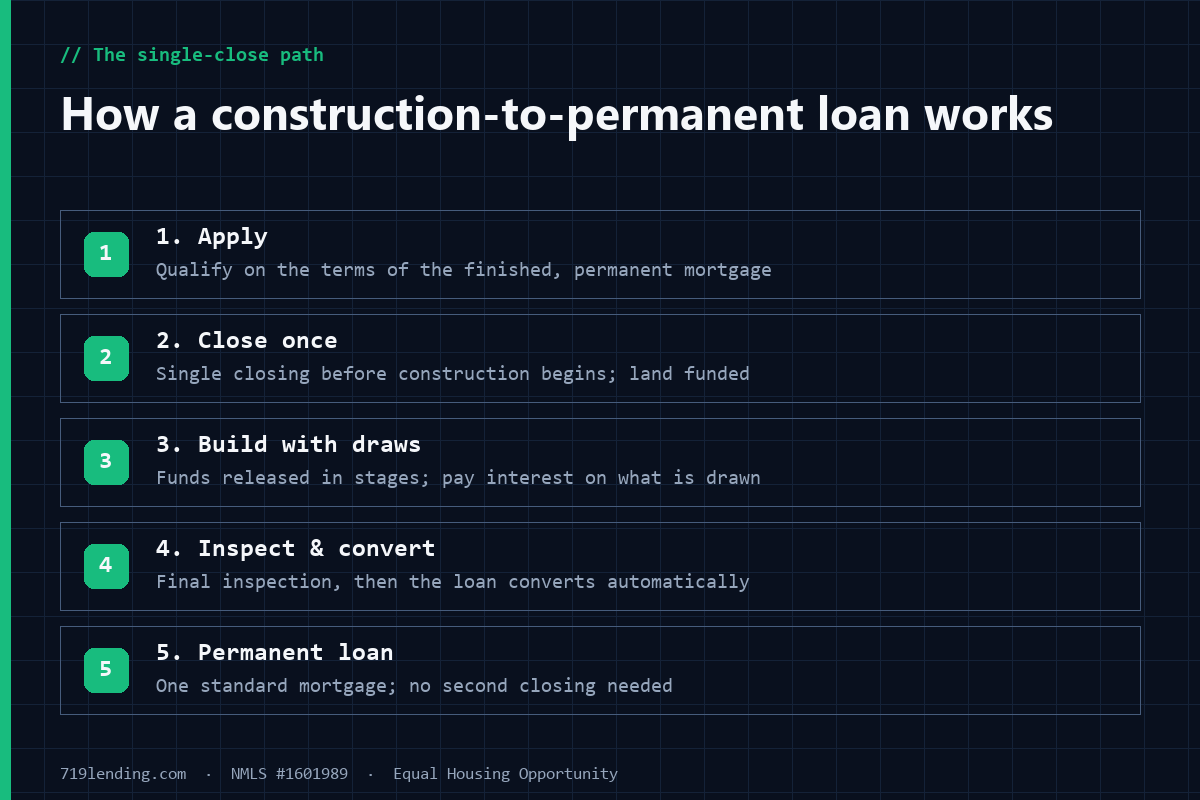

How construction-to-permanent (single-close) loans work in Colorado Springs and El Paso County: the five loan programs, down payments, draws, underwriting, and timeline.

USDA construction loans” />

USDA construction loans” /> USDA construction loans” />

USDA construction loans” />