A one-time close construction loan (also called construction-to-permanent financing) uses a single closing before construction begins; when the home is finished, that same loan automatically converts to your permanent mortgage, so you pay one set of closing costs and handle your rate once. A two-time close uses an interim construction loan first, then a completely separate closing to refinance into permanent financing when the home is done, which means two closings, two sets of closing costs, and re-qualifying and re-appraising at conversion. For most Colorado Springs buyers building on a lot in Banning Lewis Ranch, Falcon, or out toward Peyton, the practical question is not which one is “better” in the abstract, but which structure fits your loan program, your timeline, and your tolerance for rate risk while the framing goes up.

This guide defines both structures precisely, shows which loan programs use which, and walks through the trade-offs that actually move the needle: closing costs, rate-lock exposure, re-qualification risk, and cash flow. Every agency rule below is drawn from the lender’s own published guide, verified current as of July 2026.

What a one-time close construction loan actually is

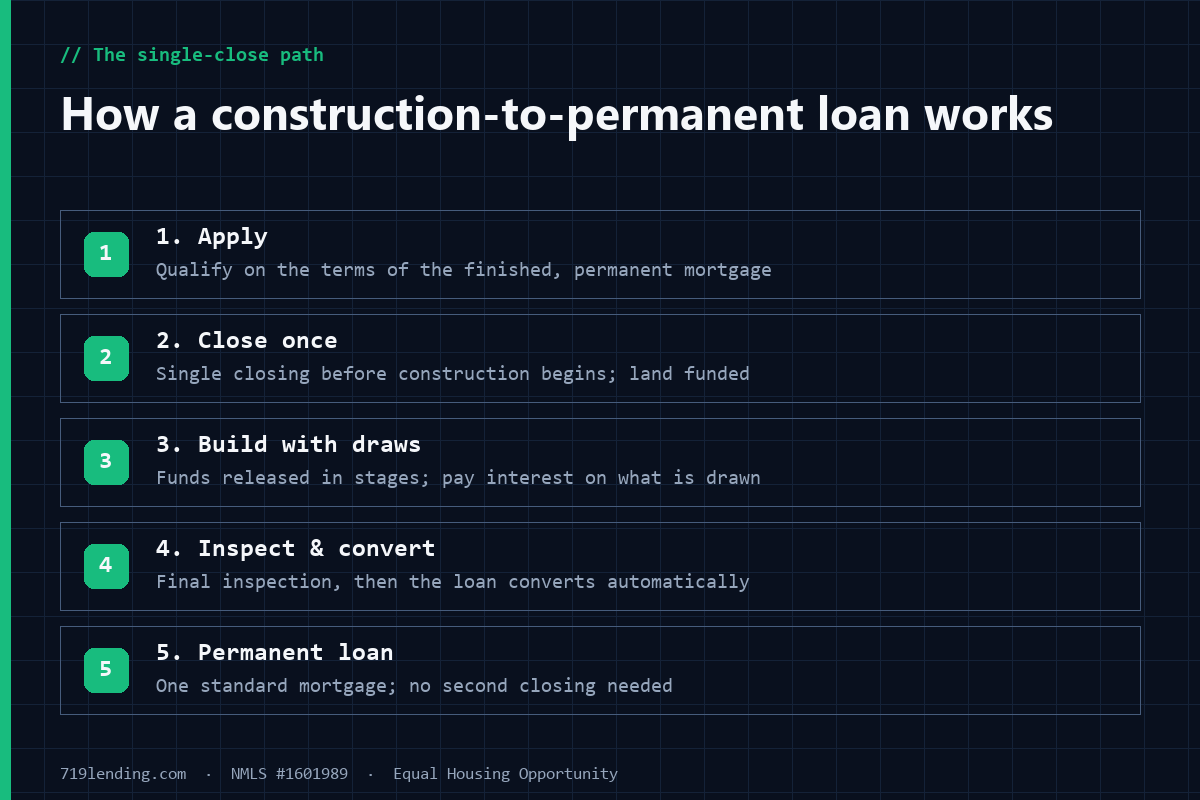

A one-time close (OTC) loan combines the short-term construction loan and the long-term permanent mortgage into a single transaction with one closing that happens before the first shovel hits the dirt. You qualify once, sign once, and lock the structure of your permanent financing up front. As construction proceeds, the lender advances money to the builder in stages (draws), and you typically pay interest only on the funds drawn. When the certificate of occupancy is issued and the home is complete, the loan converts, or “modifies,” into your permanent mortgage without a second application.

The FHA describes its version this way in HUD Handbook 4000.1: a Construction to Permanent Mortgage “combines the features of a construction loan … and the traditional long-term permanent residential Mortgage” with “a single mortgage closing prior to the start of construction.” That single-closing-before-construction design is the defining feature of a true one-time close across every program that offers it.

The upside is straightforward: one set of closing costs, one underwriting event, and no requirement to re-prove your income, credit, or the property value at the finish line. What you lock in at the start is what carries through.

What a two-time close construction loan actually is

A two-time close (also called two-closing) uses two separate loans with two separate sets of legal documents. The first closing funds an interim construction loan, usually a short-term, higher-rate product from a bank or credit union, and may also cover the lot purchase. Once the home is finished, you close a second time on a permanent mortgage that pays off the construction loan. Fannie Mae is explicit that it “does not purchase construction loans (the first closing); however, Fannie Mae does purchase loans that were used to provide the permanent financing.”

Because the permanent loan is a brand-new transaction, you re-qualify at conversion. That means a fresh look at your credit, income, and debts, plus a new appraisal of the completed home. If your circumstances or the market have shifted during the six-to-twelve months of construction, that second closing is where it shows up, for better or worse.

A consequential rule change took effect in 2026. Under Freddie Mac’s Seller/Servicer Guide, for mortgages with application received dates on or after February 4, 2026, all two-time close construction-to-permanent mortgages must be delivered asrefinance mortgages, classified as either a no-cash-out or cash-out refinance, regardless of whether the borrower owned the land before the interim construction financing closed. In plain terms: with a two-time close, that second loan is a refinance, not a purchase, and it is underwritten and priced accordingly. This figure is general; confirm current details with your lender.

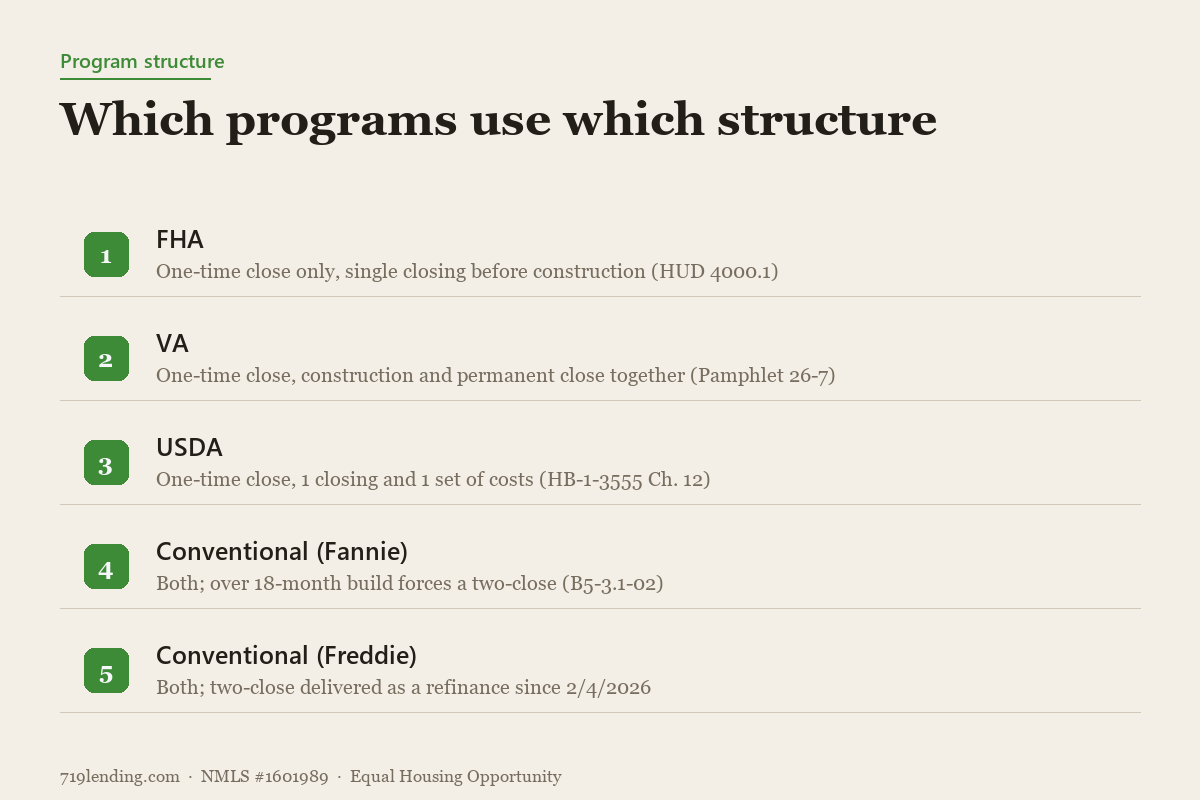

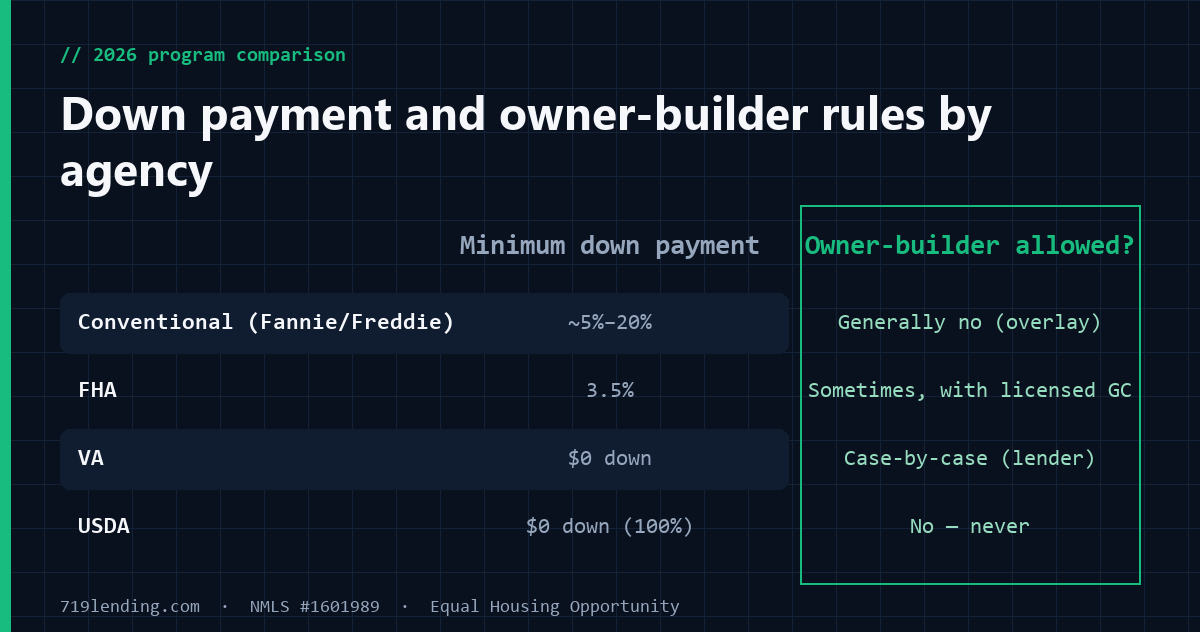

FHA, VA and USDA are one-time close by design; Fannie and Freddie offer both. General, confirm current.

Which loan programs use one-time close vs. two-time close

The single most important thing many buyers miss: your loan program often decides the structure for you. Here is how the five major programs break down, per each agency’s current guide:

USDA – one-time close. Under USDA Handbook HB-1-3555, Chapter 12, the Combination Construction-to-Permanent (single-close) loan has “only 1 loan closing (and 1 set of loan closing costs),” and the Loan Note Guarantee is issued at closing, before the home is built.

Conventional (Freddie Mac) – both. Freddie offers Construction Conversion Mortgages structured as one-time (single) or two-time close.

So if you are set on an FHA, VA, or USDA construction loan, you are getting a one-time close; there is no two-time close version of those government programs. The one-time-versus-two-time decision is a genuine choice mainly on the conventional side, through Fannie Mae and Freddie Mac.

When a two-time close becomes unavoidable

Even on the conventional side, the choice can be made for you by the construction timeline. Fannie Mae’s Selling Guide (B5-3.1-02) sets hard limits on single-closing construction-to-permanent loans: the construction loan period “may have no single period of more than 12 months and the total period may not exceed 18 months,” and it states flatly that “exceptions to the 12-month and 18-month periods will not be granted.”

The construction-period limits do not apply to two-closing transactions. So if your build is going to run long, past that 18-month total, Fannie’s guide requires the lender to process it as a two-closing construction-to-permanent transaction for the permanent loan to be eligible for sale. A sprawling custom build in the foothills, a project stalled by supply delays, or a phased build can all push past the window and force a two-close. In those cases the two-time structure is not a preference; it is the only way the loan works.

The trade-offs that actually matter

Closing costs

This is the clearest difference. A one-time close means one set of closing costs, lender fees, title, recording, and the like, paid once. A two-time close means you pay closing costs twice: once on the interim construction loan and again on the permanent refinance. USDA’s own materials cite the single closing and single set of closing costs as the reason single-close loans “save applicants money over older two-time closed loans.” For a typical Colorado Springs build, a second full closing can add several thousand dollars, so the savings on a one-time close are real, not theoretical. Actual costs vary by lender and loan amount; general, confirm current.

Rate-lock exposure

With a one-time close, your permanent financing terms are set up front, before construction, which protects you if rates climb while the home is being built. Many one-time close programs use an extended lock or, as VA allows, a “ceiling-floor” (float-down) option, where the borrower must qualify at the maximum rate but can lock lower if the market improves. With a two-time close, your permanent rate is not set until the second closing, potentially a year later, so you carry the full risk (and the full opportunity) of wherever rates land at completion.

Re-qualification and re-appraisal risk

A one-time close underwrites you once. A two-time close requires you to re-qualify at conversion, a fresh credit pull, re-verified income and employment, and a new appraisal of the finished home. If you change jobs, take on new debt, or the completed-home appraisal comes in soft, that second closing is where a two-time close can wobble. The one-time close eliminates that finish-line uncertainty, which is why it is often the calmer path for salaried buyers with stable finances.

Cash flow during construction

Both structures typically bill interest only on the funds drawn during the build, so monthly carrying costs behave similarly while the home goes up. The cash-flow divergence is mostly at the closings: one-time close front-loads a single set of costs, while two-time close spreads costs across two events but totals more. A two-time close can occasionally offer more flexibility mid-project (for example, shopping the permanent loan separately), but that flexibility is exactly what creates the re-qualification exposure above.

One-time close: 1 closing, 1 set of costs, rate set up front, no re-qualification. General, confirm current.

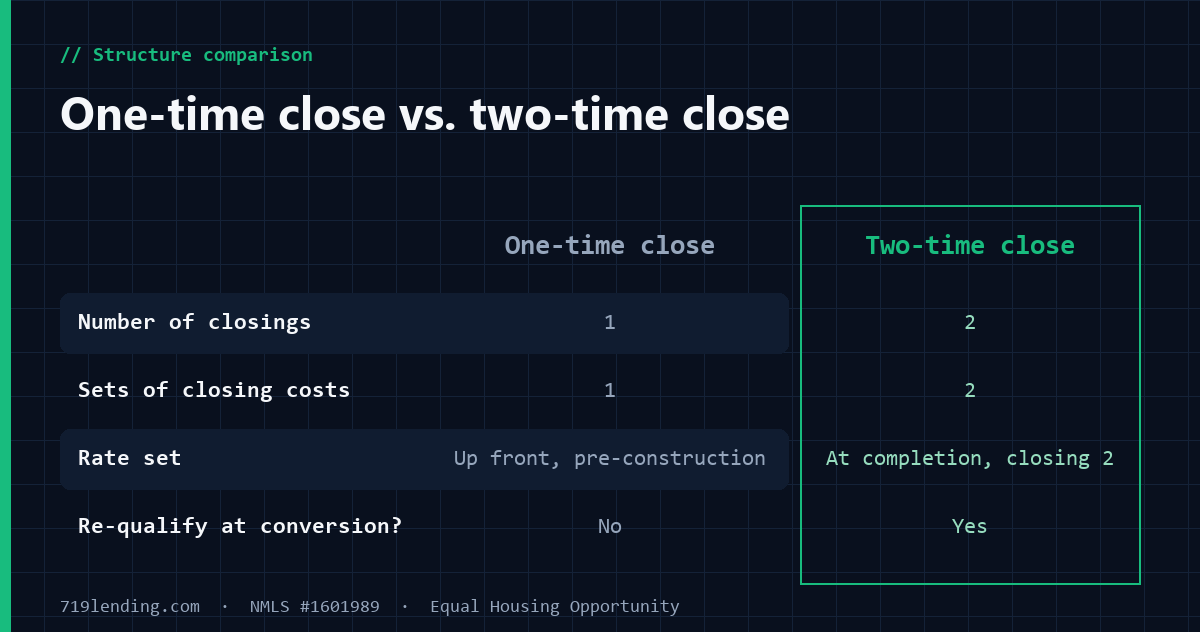

One-time close vs. two-time close at a glance

The core distinctions, side by side:

Feature

One-time close

Two-time close

Number of closings

1

2

Sets of closing costs

1

2

Permanent rate exposure

Set up front, before construction

Set at second closing, at completion

Re-qualify at conversion?

No

Yes (new credit, income, appraisal)

Second loan classified as

N/A (auto-converts)

Refinance (Freddie, apps on/after 2/4/2026)

Our take: for most Colorado buyers, the one-time close is the cleaner path

Our take: For the majority of Colorado Springs and El Paso County buyers we work with, especially first-time builders and active-duty and veteran families near Fort Carson using VA financing, the one-time close is the cleaner structure. You close once, you pay one set of costs, and you lock your permanent terms before a single truss is set, so a jump in rates during a nine-month build cannot ambush you at the finish line. You also skip the re-qualification gauntlet, which matters if there is any chance your income, debts, or the completed appraisal could shift.

The two-time close earns its place in two situations: when your build is genuinely going to run past the conventional 18-month window (which forces a two-close), or when a borrower has a specific reason to keep the permanent loan separate and is comfortable carrying the rate and re-qualification risk. Both are legitimate; they are just less common. That said, every build is different, and the right structure depends on your program, timeline, and finances, which is exactly the conversation to have with a broker before you break ground.

Frequently asked questions

Is a one-time close the same as construction-to-permanent financing? Yes. “One-time close,” “single-close,” and “construction-to-permanent” all describe the same structure: one closing before construction that automatically converts to your permanent mortgage when the home is complete, with one set of closing costs.

Do FHA, VA, and USDA offer two-time close construction loans? No. FHA (HUD Handbook 4000.1), VA (Pamphlet 26-7), and USDA (HB-1-3555) construction programs are all one-time close by design. The two-time close option exists mainly on conventional loans through Fannie Mae and Freddie Mac.

Why would I ever choose a two-time close? Usually because you have to. If a conventional build will exceed Fannie Mae’s 18-month total construction limit, the lender must process it as a two-closing transaction. Some borrowers also choose it to keep the permanent loan separate, accepting the extra costs and re-qualification.

What changed with Freddie Mac two-time close loans in 2026? For applications received on or after February 4, 2026, Freddie Mac requires all two-time close construction-to-permanent mortgages to be delivered as refinance mortgages (no-cash-out or cash-out), regardless of when the borrower acquired the land. The permanent loan cannot be treated as a purchase. This figure is general; confirm current details with your lender.

Do I have to re-qualify with a one-time close? No. A one-time close underwrites you once, before construction. A two-time close requires you to re-qualify at the second closing with a new credit check, re-verified income, and a new appraisal of the finished home.

Which is cheaper, one-time or two-time close? A one-time close is generally less expensive because you pay closing costs only once. A two-time close involves two closings and two sets of closing costs. Actual costs vary by lender and loan amount; general, confirm current.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. Figures and program rules are general, confirm current with your lender before making decisions. Last updated: July 2026.

FHA, VA, USDA, and conventional (Fannie/Freddie) construction loans compared for 2026 — down payment, one-time vs. two-time close, when the guarantee happens, and owner-builder rules, verified against each agency's guide.

How construction-to-permanent (single-close) loans work in Colorado Springs and El Paso County: the five loan programs, down payments, draws, underwriting, and timeline.