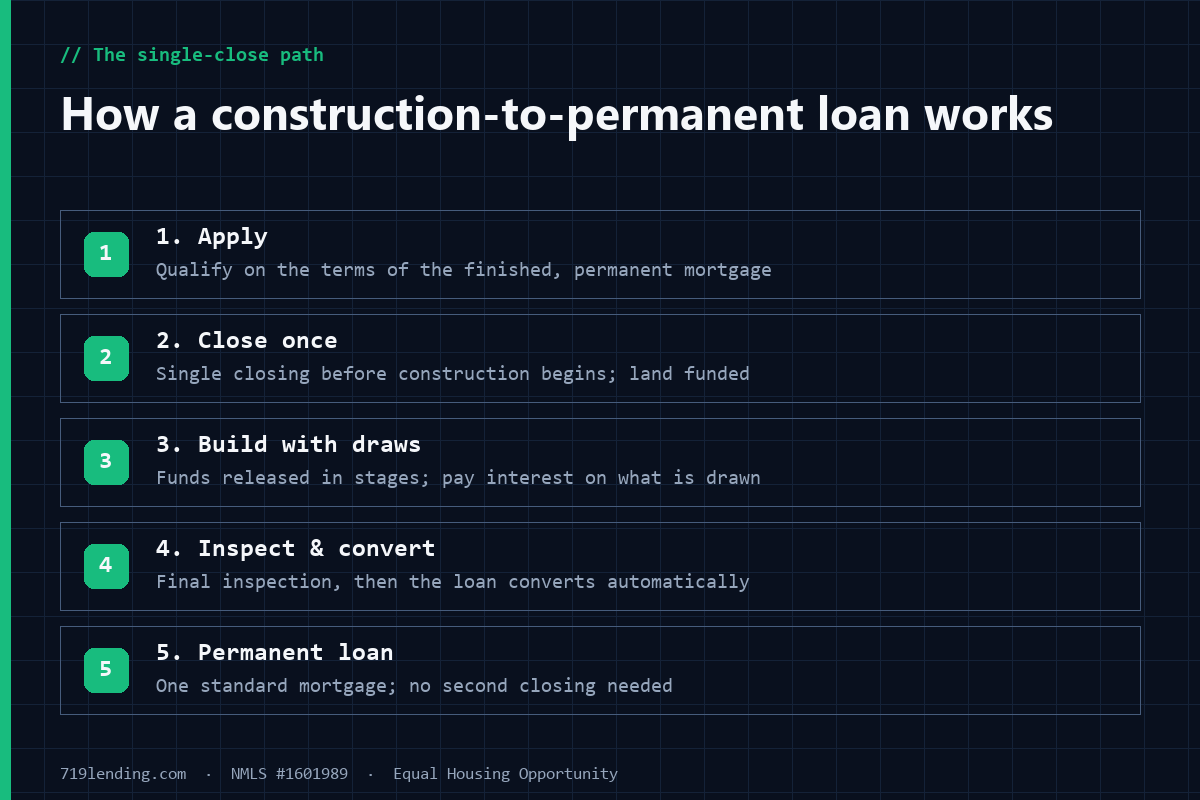

A construction-to-permanent loan (often called a single-close loan) finances the land, the build, and your long-term mortgage in one loan that closes once, before construction starts. During the build you draw funds in stages and typically pay interest only on what has been disbursed; when the home is finished, the loan automatically converts to a permanent mortgage without a second closing. That single structure is what separates building a home from buying an existing one, and it is the foundation for every construction loan program available in Colorado Springs and El Paso County.

This is the front-door guide to construction lending on the Front Range. Below you will find plain-English teasers on each piece of the process, each linking to a deep-dive: the loan structures, the five programs at a glance, using land equity as a down payment, how draws and inspections work, what underwriting checks, and the timeline. If you are weighing a build in Monument, Falcon, Peyton, or Black Forest, start here and branch out.

One loan, one closing, converting to a permanent mortgage when the home is complete.

What a construction-to-permanent loan is and how it differs from buying an existing home

When you buy an existing home, the collateral already exists and the lender can appraise and fund it today. When you build, there is no house yet, so the lender is financing a promise: plans, a builder contract, a budget, and a timeline. A construction-to-permanent loan bridges that gap by funding the project in draws as work is completed, then rolling into a standard mortgage once the home passes final inspection.

Fannie Mae, which sets the rules most conventional lenders follow, requires that single-closing construction-to-permanent loans be underwritten based on the terms of the permanent financing, and that the construction period have no single phase longer than 12 months, with the total period not exceeding 18 months. That is why your rate and payment are set around the finished mortgage, not the interim build loan. For a full breakdown of eligibility and paperwork, see our guide to construction loan requirements.

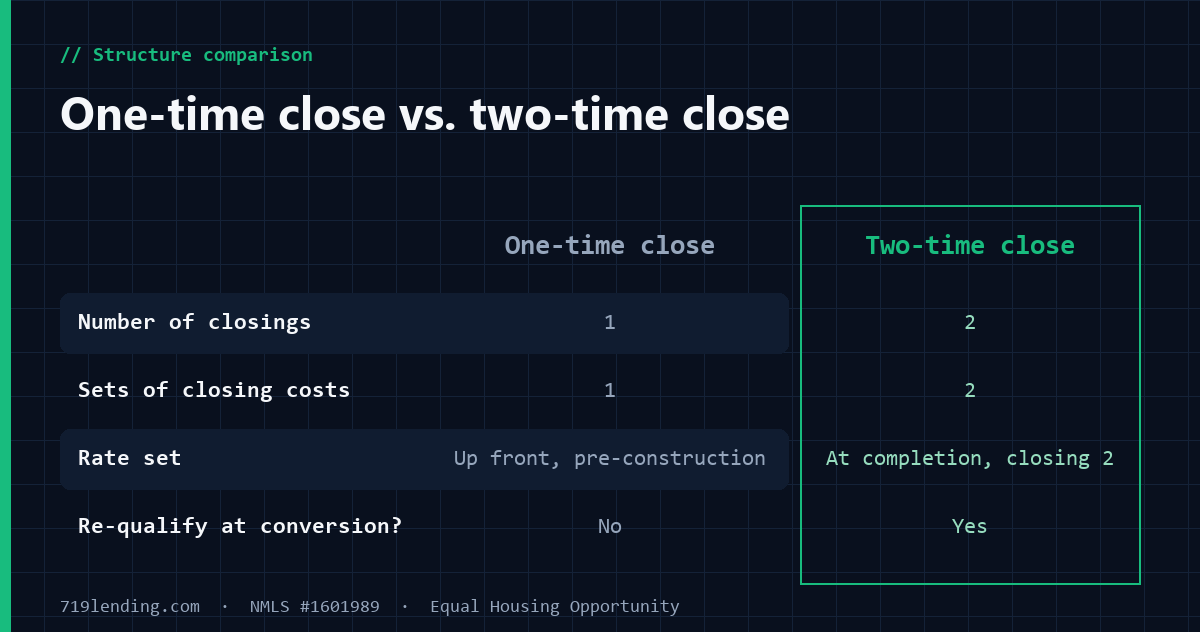

Single-close vs two-close construction loans in brief

There are two ways to structure the financing, and choosing correctly can save you a second set of closing costs and a second rate lock.

Single-close (one-time close): One loan, one closing, before construction begins. It converts to permanent financing when the home is done. Freddie Mac’s rules, updated effective February 4, 2026, now allow the terms of a One-Time Close loan to be modified at conversion to permanent financing, adding flexibility for borrowers whose rate environment shifts during the build.

Two-close (two-time close): A short-term construction loan first, then a separate permanent loan that pays it off. Under both Freddie Mac and Fannie Mae rules, that permanent loan is classified as a refinance, not a purchase, and typically requires that at least one borrower has held title to the land for six months or more before the permanent loan closes.

Which one fits depends on your rate outlook, your builder’s timeline, and how long you have owned your lot. We walk through the trade-offs in detail in one-time close vs two-time close construction loan.

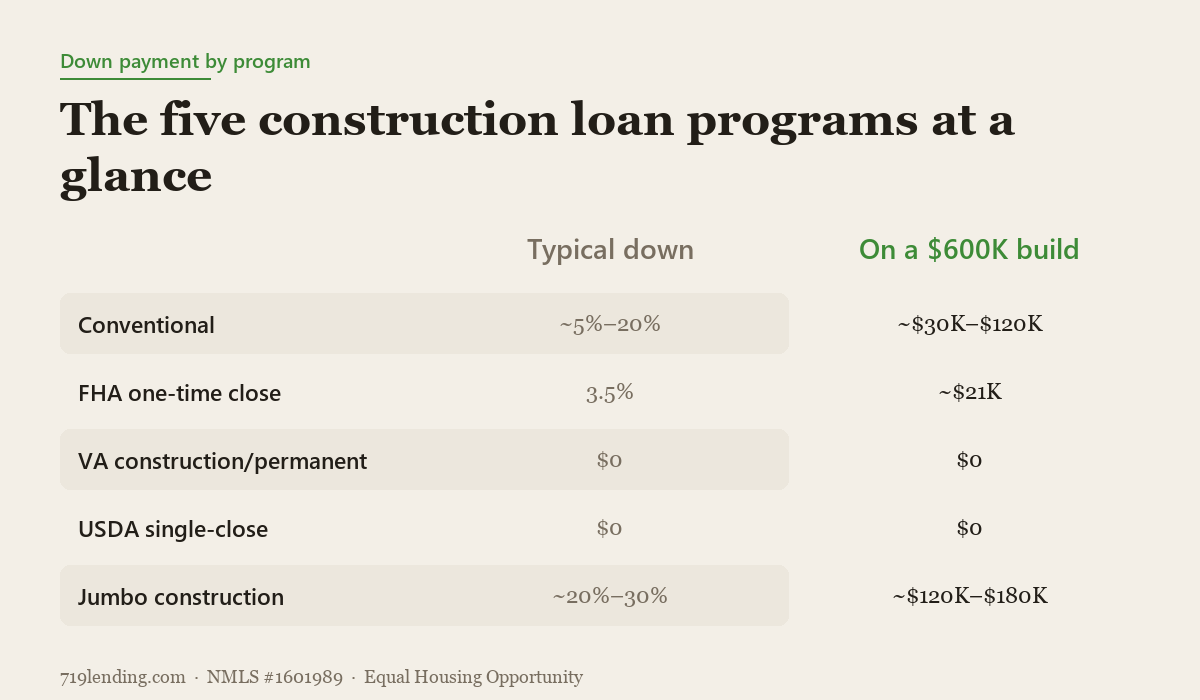

Typical minimum down by program on a $600K build. General, confirm current.

The five construction loan programs at a glance

Colorado builders can access five broad program families, each with its own down-payment floor. The figures below are general starting points; your actual requirement depends on credit, the property, and the lender’s overlays.

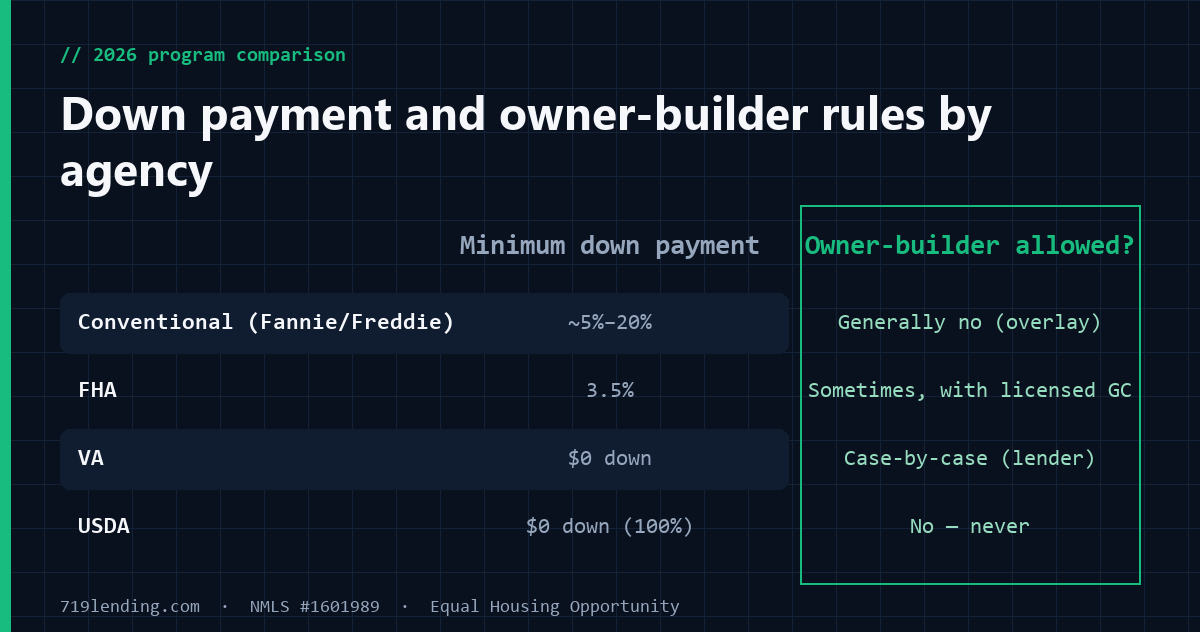

Conventional: The most common path for well-qualified borrowers. Fannie Mae requires the borrower to contribute their own funds for the minimum down payment unless the loan-to-value ratio is at or below 80%. See conventional construction loan.

FHA: The FHA one-time close program (HUD Handbook 4000.1) allows 96.5% financing — a 3.5% down payment — for borrowers with a minimum decision credit score of 580 or higher. See FHA construction loan, and our broader FHA loan Colorado overview.

USDA: The USDA single-close program offers 100% financing (no money down) in eligible rural areas — which include large parts of eastern and northern El Paso County. See USDA construction loan.

Jumbo: For builds above the conforming loan limit, expect a larger down payment. See our construction loan down payment guide for how much cash you will actually need.

Using land equity as your down payment

One of the most useful facts in construction lending: if you already own your lot, its value can often stand in for some or all of your cash down payment. Because the appraisal values the land as part of the completed project, the equity you hold in that land counts toward the deal.

The VA is explicit about this — ownership of the land prior to construction is eligible to count toward reducing the funding fee, provided the appraisal assigns a value to the unimproved land. Conventional and other programs treat lot equity similarly within their LTV rules. If you bought a parcel in Peyton or Black Forest years ago, that equity may mean little or nothing out of pocket at closing. We break the math down in construction loan down payment.

How construction draws and inspections work

You do not receive the full loan amount at closing. Instead, funds are released in a series of draws tied to completed phases of construction — foundation, framing, mechanicals, drywall, and final. Before each draw, the lender typically orders an inspection to confirm the work is done, and you generally pay interest only on the funds disbursed so far, which keeps early-build payments low.

USDA’s single-close program even lets lenders escrow up to 10% of the amount for cost overruns, and escrow up to 12 months of loan payments during construction, so borrowers are not stretched paying rent and a mortgage at once. The number of draws, who signs off, and how contingency funds work vary by program and builder. See the full mechanics in how construction loan draws work.

What underwriting checks — including your builder

A construction loan underwrites two parties, not one. The lender reviews you — credit, income, assets, and debt-to-income — the same way any mortgage would. But it also reviews the project and the builder: the construction contract, the fixed budget, the plans and specifications, the appraisal of the completed home, and the builder’s licensing, insurance, and track record.

This dual review is why construction files take longer to approve than a purchase. A disorganized budget or an unvetted builder can stall an otherwise strong application. Our construction loan requirements guide lists exactly what documentation you and your builder need to assemble before you apply. If you would rather build your own home without a general contractor, read owner-builder construction loan first — the bar is higher, and note that some programs (including USDA’s single-close) do not allow owner-builders at all.

The construction loan timeline

From application to move-in, a Colorado build typically runs several months longer than a purchase because the house has to be built. Fannie Mae’s framework caps the construction phase at 12 months for any single period and 18 months total for single-closing loans, which sets the outer boundary most lenders work within. Between plan approval, permitting through El Paso County or the City of Colorado Springs, the build itself, inspections, and the conversion to permanent financing, planning ahead matters.

We lay out a realistic, phase-by-phase schedule — and where delays tend to happen — in the construction loan timeline guide.

Who construction loans are for, and the Colorado Springs building context

Construction financing fits buyers who cannot find the right existing home, want to build on land they already own, or are pursuing new construction in the region’s growing corridors. El Paso County has active building in Monument, Falcon, Peyton, and Black Forest, along with continued growth near Fort Carson and the northern I-25 corridor. Many of these areas include parcels eligible for USDA rural financing, and the mix of veterans and service members tied to Fort Carson, Peterson Space Force Base, and the Air Force Academy makes the VA construction/permanent loan especially relevant here.

Our take: for most first-time builders in El Paso County, the single-close structure is the safer default — it locks the process into one closing and removes the risk of not qualifying for a second loan after you have already spent months building. But if you expect rates to fall meaningfully during a long build, the two-close route (or Freddie Mac’s new option to modify a One-Time Close at conversion) deserves a serious look. This is a judgment call, not a rule, and it is exactly the kind of thing a broker should model with you. First-time buyers should also review Colorado first-time home buyer programs.

Work with a Colorado Springs broker who does construction lending

Construction loans are among the most complex products in residential lending, and program rules genuinely change — Freddie Mac’s February 2026 update is proof. As an independent broker, we shop your build across multiple construction lenders rather than fitting you into one bank’s single program. Start with our mortgage broker Colorado Springs team, and see the full field of options in construction loan lenders Colorado.

Frequently asked questions

What is the difference between a construction-to-permanent loan and a regular mortgage? A regular mortgage funds the purchase of a home that already exists. A construction-to-permanent loan funds the land and the build in stages (draws), then converts to a standard mortgage once the home is finished — all under one loan for a single-close structure.

How much do I need to put down on a construction loan in Colorado? It depends on the program. General starting points: conventional roughly 5%–20%, FHA 3.5% (at a 580+ credit score), VA and USDA $0 for eligible borrowers, and jumbo roughly 20%–30%. These are general figures — confirm current requirements with a lender.

Can the land I already own count as my down payment? Often, yes. Because the appraisal values the completed project including the lot, the equity in land you already own can offset some or all of the cash down payment. The VA specifically allows land ownership to reduce the funding fee. Amounts vary by program.

Do I make payments while my home is being built? With most construction loans you pay interest only on the funds drawn so far during the build, which keeps early payments low. USDA’s single-close program even allows escrowing up to 12 months of payments during construction, and VA construction/permanent borrowers can postpone the first principal payment for up to a year.

How long can construction take with these loans? For single-closing conventional loans, Fannie Mae caps any single construction period at 12 months and the total period at 18 months. Actual build times depend on the project, weather, and permitting through El Paso County or the City of Colorado Springs.

Is a single-close or two-close loan better? Single-close usually wins for simplicity and to avoid re-qualifying, but a two-close (or Freddie Mac’s option to modify a One-Time Close at conversion) can make sense if you expect rates to drop during a long build. It is a case-by-case decision worth modeling with a broker.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. All figures and program rules are general — confirm current details with a licensed loan officer, as agency guidelines change. Last updated: July 2026.

One-time close vs. two-time close construction loans explained for Colorado Springs buyers: closings, costs, rate exposure, re-qualification, and which programs use which.

FHA, VA, USDA, and conventional (Fannie/Freddie) construction loans compared for 2026 — down payment, one-time vs. two-time close, when the guarantee happens, and owner-builder rules, verified against each agency's guide.