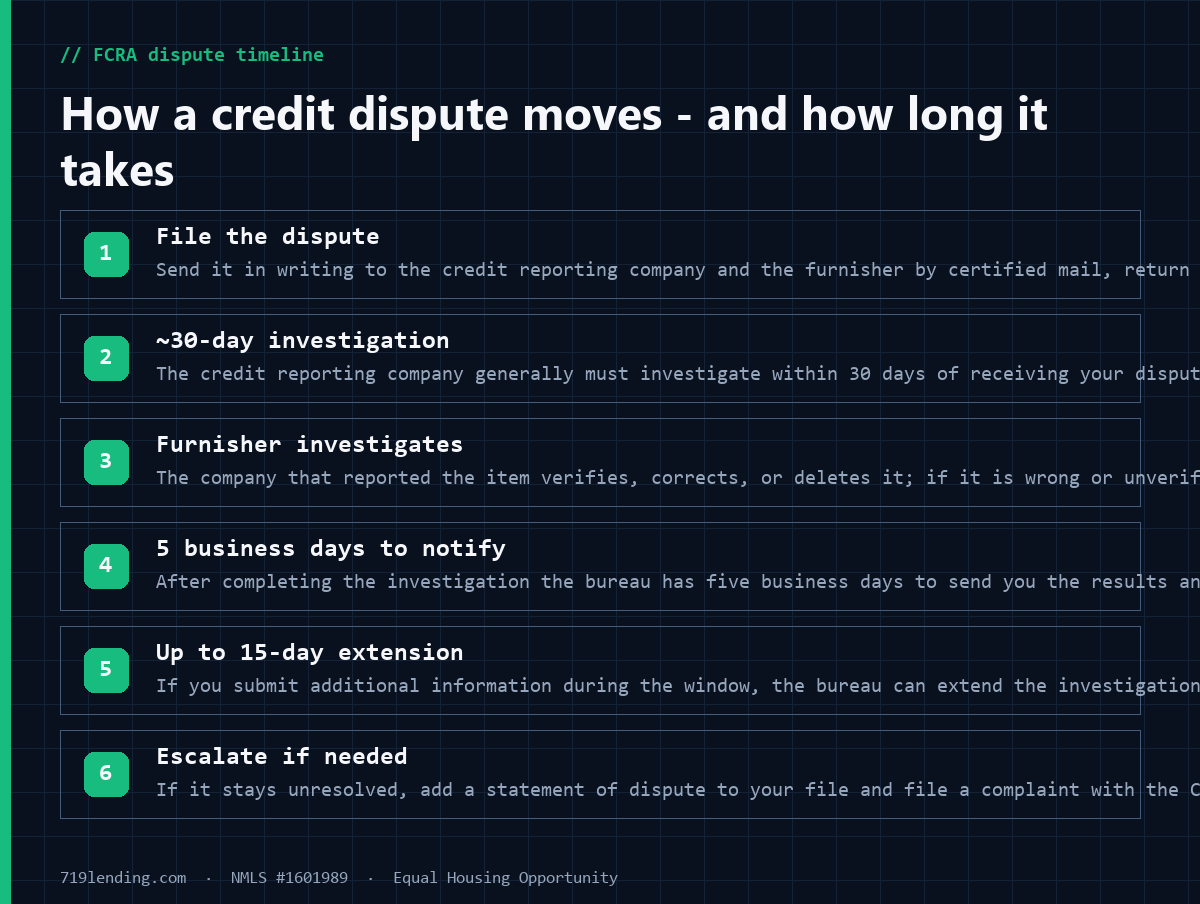

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Does Shopping for a Mortgage Hurt Your Credit?

Shopping for a mortgage does not meaningfully hurt your credit, and the fear of it costs borrowers real money. A single hard mortgage inquiry usually takes off fewer than five points, the effect is temporary, and the major scoring models are built to bundle all of your rate-shopping mortgage inquiries into what counts as a single inquiry. That is the whole point of this article: you can let a mortgage broker pull your credit once and shop many lenders on your behalf without wrecking your score. Below is exactly how the models treat these inquiries, the short window you want to shop inside, and why comparing lenders is the financially smart move even though a pull touches your credit.

Hard inquiry vs. soft inquiry: only one touches your score

Every credit check falls into one of two buckets, and the difference is what most of the worry comes down to.

- Soft inquiry (soft pull): Checking your own credit, a lender pre-qualifying you for an offer, or an existing creditor reviewing your account. A soft pull is only visible to you and, per FICO, will never harm your score. Getting your own credit report is a soft inquiry, so you can look as often as you like.

- Hard inquiry (hard pull): When you apply and a lender pulls your credit to make a lending decision, such as a mortgage, auto loan, or credit card application. A hard inquiry is visible to lenders and can have a small, temporary effect on your score.

When a mortgage lender or broker pulls your credit to price a loan, that is a hard inquiry. So yes, it registers, but the size of that ding is far smaller than most people fear, and the models go a step further to protect people who are shopping.

How much does one mortgage inquiry actually cost you?

Not much. According to FICO, for most people one additional hard inquiry results in the loss of fewer than five points, and inquiries live inside the “new credit” category, which is only about 10% of your FICO Score. In other words, a single mortgage pull is a small, single-digit, temporary effect for most borrowers (general figures, and individual results vary, so confirm current). There is no such thing as a 40-point inquiry.

The effect also fades on its own. FICO reports that hard inquiries stay on your credit report for up to two years, but they only factor into your FICO Score for about one year. So even in the rare case where an inquiry nudges your score, it is temporary by design.

The key point: rate-shopping inquiries get bundled into one

Here is the part that removes the real barrier. The scoring models know that a rational borrower shops around for one mortgage, not many. So instead of penalizing you for each lender you talk to, they de-duplicate your mortgage inquiries. Multiple mortgage inquiries that land inside a short window count as a single inquiry for scoring purposes.

Two protections are actually working at once inside the FICO model:

- A de-duplication window. FICO counts multiple mortgage, auto, or student loan inquiries that fall within a defined shopping period as just one inquiry. In newer FICO versions that window is 45 days; older FICO versions still in use allow a 14-day span (general figures, version-dependent, confirm current).

- A buffer period before scoring. FICO also ignores auto, mortgage, and student loan inquiries made in the 30 days prior to scoring. So if you apply and get scored inside that window, those brand-new mortgage inquiries do not weigh on the score at all yet.

VantageScore, the model behind many free consumer credit apps, works the same way with a tighter window: it uses a 14-day rolling window in which multiple inquiries from mortgage or auto lenders are treated as a single search for credit. The CFPB describes the same protection for consumers, noting that within a 45-day window multiple credit checks from mortgage lenders are recorded as a single inquiry, precisely because lenders realize you are only going to buy one home.

One important limit: this rate-shopping grouping applies to mortgage, auto, and student loan inquiries. Credit card inquiries do not get bundled this way, so each new card application is scored as its own inquiry. Shopping for a mortgage is protected; opening new credit cards during the process is not.

The FICO and VantageScore shopping windows side by side

The two dominant scoring families draw their rate-shopping windows differently, which is why one safe rule beats memorizing both.

| Feature | FICO (mortgage versions) | VantageScore |

|---|---|---|

| Rate-shopping window | 45 days (newer); 14 days (older versions) | 14-day rolling window |

| Buffer before inquiries score | Ignores mortgage inquiries in the 30 days prior to scoring | Not published the same way |

| Loan types grouped | Mortgage, auto, student loan | Mortgage and auto |

| Credit cards grouped? | No | No |

General figures, version-dependent and subject to change; confirm current with the scoring provider. The safe move that satisfies both models: cluster every mortgage credit pull into a tight window of about 14 days. Do that, and you are comfortably inside VantageScore’s 14-day window and FICO’s larger 45-day window at the same time.

Why a broker can shop many lenders without wrecking your score

This is where the mortgage angle matters most. A mortgage broker is not a single lender; a broker shops your file across many wholesale lenders to find a competitive combination of rate, program, and fees. Borrowers sometimes hesitate because they picture a dozen separate hard pulls hammering their score. That is not how it works.

First, the broker generally pulls your credit one time. Federal mortgage requirements push toward a merged report rather than a bureau-by-bureau scramble. Fannie Mae’s Selling Guide directs lenders to request a three-in-file merged “tri-merge” credit report covering all three national bureaus, Equifax, Experian, and TransUnion. That single tri-merge pull is the file the broker then uses to shop your loan around. You are not re-pulled for every lender the broker quotes.

Second, even in cases where more than one hard mortgage inquiry does hit your report, the de-duplication and buffer rules above collapse them toward a single inquiry as long as they land in the same short window. So letting one broker pull once and shop widely is one of the most credit-friendly ways to comparison shop a mortgage.

The CFPB and every major scoring provider agree the benefit of shopping dwarfs the cost. You are borrowing hundreds of thousands of dollars over decades; a difference of an eighth or a quarter of a percent in rate can be worth thousands over the life of the loan. Trading a possible few-point, temporary inquiry effect for that is not a close call.

How to shop your mortgage the safe way

Put the rules to work with a simple game plan:

- Check your own credit first (soft pull). Look at your reports and scores before anyone applies. Your own check never harms your score, so clean up errors and know where you stand ahead of time.

- Get pre-qualified where possible before a hard pull. Many lenders and brokers can give a soft-pull estimate to narrow the field before a formal application.

- Cluster all mortgage credit pulls into about 14 days. Keeping every mortgage inquiry inside a two-week burst keeps you safely inside both the FICO and VantageScore rate-shopping windows.

- Let one broker pull once and shop it. A broker’s single tri-merge pull can be shopped across many wholesale lenders, so you compare offers without stacking separate hard inquiries.

- Do not open new credit cards or finance a car mid-process. Those inquiries are not bundled with your mortgage shopping, and new debt can also change your debt-to-income ratio right when it matters. When in doubt, ask your loan officer before applying for anything.

Follow that sequence and the honest answer to whether shopping hurts your credit is: barely, briefly, and not enough to matter next to the money you can save.

Frequently asked questions

Does shopping for a mortgage hurt your credit score? Only slightly and temporarily. A single hard mortgage inquiry typically costs most people fewer than five points, per FICO, and inquiries are part of the “new credit” category that makes up only about 10% of your score. The scoring models also bundle multiple mortgage inquiries made in a short window into a single inquiry, so shopping several lenders is treated much like one (general figures, confirm current).

How many days do I have to shop before it counts as multiple inquiries? FICO uses a rate-shopping window of 45 days for newer versions (14 days in older versions), and VantageScore uses a 14-day rolling window. To stay safe under both, cluster all of your mortgage credit pulls into roughly a 14-day span. These windows are version-dependent, so confirm current.

What is the difference between a hard and soft credit inquiry? A soft inquiry, such as checking your own credit or a pre-qualification, has no effect on your score and is only visible to you. A hard inquiry happens when you formally apply and a lender pulls your credit to lend; it is visible to lenders and can have a small, temporary effect.

Does letting a mortgage broker pull my credit hurt my score more than one lender? No. A broker generally pulls one merged tri-merge report and shops that single file to many wholesale lenders, so you are not re-pulled for each lender. Any mortgage inquiries that do register in the same short window are de-duplicated toward a single inquiry by the scoring models.

Do credit card inquiries get the same rate-shopping protection? No. The rate-shopping bundling applies to mortgage, auto, and student loan inquiries. Each credit card application is scored as its own hard inquiry, so avoid opening new cards while your mortgage is in process.

How long do mortgage inquiries stay on my credit report? Hard inquiries can remain on your report for up to two years, but per FICO they only factor into your FICO Score for about one year, and the effect for most borrowers is minor and fades over time.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is a licensed mortgage broker and is not affiliated with, or endorsed by, any government agency; FHA, VA, USDA, and CHFA are government programs referenced for educational purposes only. Point-swing figures, scoring windows, and program details above are general and version-dependent, are for education only, are not a promise of any specific score change, credit decision, or interest rate, and should be confirmed current. Last updated: June 2026.

Related Posts