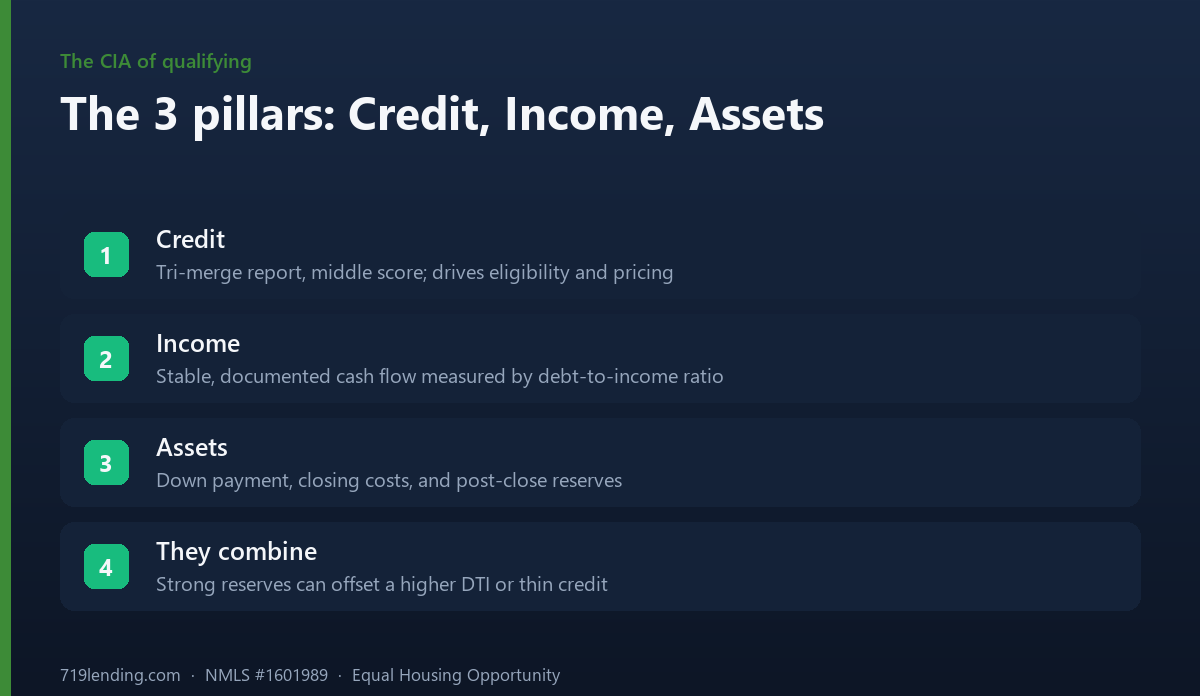

Credit, income, and assets are the three pillars every mortgage lender checks. Here is what each one means, why it matters, and how to strengthen it before you apply in Colorado Springs.

Mortgage Reserves: How Much Cash You Need After Closing (and Why)

Mortgage reserves are the liquid assets you have left over after you pay your down payment and closing costs, measured in the number of months of your full house payment those savings could cover. Lenders and the agencies that back most home loans call this “months of reserves,” and they measure it against your qualifying PITIA payment: principal, interest, taxes, insurance, and any HOA or association dues. For a well-qualified buyer purchasing a primary home in Colorado Springs, the required amount is often zero. But on tougher files, and on second homes and rentals, reserves can quietly decide whether your loan is approved or declined.

This guide explains what reserves are, when they are required, what money counts, and how the paper trail works. Figures below are general guidelines drawn from current agency rules and are meant to be educational; confirm current requirements for your specific loan with a licensed loan officer.

What mortgage reserves actually are

Fannie Mae’s Selling Guide puts it plainly: liquid financial reserves are “those liquid or near liquid assets that are available to a borrower after the mortgage closes.” In other words, reserves are not the money you bring to the closing table. They are what remains in your accounts once the down payment and closing costs are gone.

The measurement is always expressed in months. Fannie Mae counts reserves as “the number of months of the qualifying payment amount for the subject mortgage (based on PITIA)” that a borrower could pay. So if your total PITIA payment is $2,500 and you have $15,000 in eligible reserves after closing, you have six months of reserves. Critically, the guide states that “funds to close are subtracted from available assets when considering sufficient assets for reserves” — you cannot count the same dollar twice.

PITIA is the key term, because it is broader than the loan payment alone. It includes:

- Principal and interest on the mortgage itself.

- Property taxes, which in El Paso County are collected and escrowed monthly.

- Homeowners insurance, plus mortgage insurance if you put down less than 20%.

- Association dues (HOA), common in many Colorado Springs subdivisions and condos.

Reserves sit inside the broader picture of assets a lender reviews. If you want the full context on how income and debts fit together, see our guide to debt-to-income ratio when buying a home, and how a file clears underwriting once all the pieces line up.

When reserves are required and how much varies

Here is the part that surprises many first-time buyers: for a standard, well-qualified purchase of a primary home, there is frequently no reserve requirement at all. Fannie Mae’s Selling Guide states directly that “there is no minimum reserve requirement for one-unit principal residence transactions” underwritten to its standard rules.

The requirement climbs as risk rises. Under current agency guidelines, the general pattern looks like this:

| Property type | Typical reserve requirement |

|---|---|

| One-unit primary residence | Often none (0 months) |

| Second home | 2 months of PITIA |

| Investment property (1-unit) | 6 months of PITIA |

| Two- to four-unit property | 6 months of PITIA |

These are conventional (Fannie Mae) baselines and are general — confirm current figures for your loan. Other programs set their own bars. FHA, for example, requires reserves equal to three months’ payments after closing on three- and four-unit properties, per HUD Handbook 4000.1. Jumbo and non-QM loans routinely ask for more — six, nine, or twelve months is common — because those loans fall outside agency backing. If you are self-employed or using a bank-statement program, reserves are almost always part of the conversation; our guide to qualifying for a mortgage when you are self-employed covers how those files are built.

Reserves also stack when you already own real estate. Fannie Mae requires additional reserves calculated as a percentage of the combined unpaid balances on your other financed properties — roughly 2% for one to four financed properties, 4% for five or six, and 6% for seven to ten. A borrower with several rentals can face a meaningful reserve figure on top of the base requirement for the new loan.

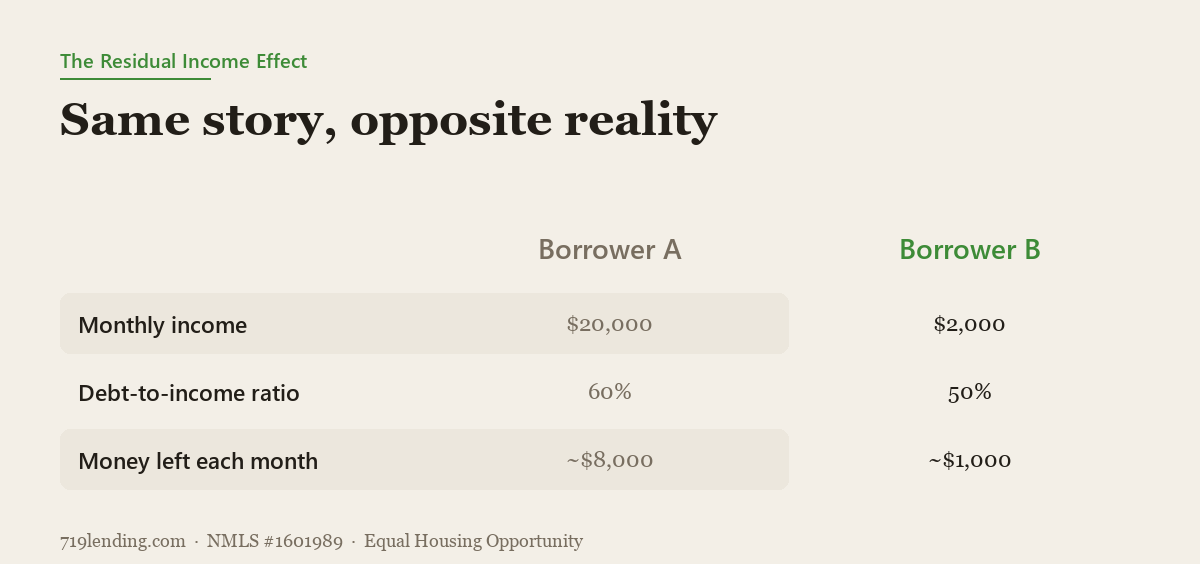

Reserves can also be used affirmatively — to offset a risk factor an underwriter flags. A thinner credit profile, a higher debt-to-income ratio, or a recent job change can sometimes be balanced by strong reserves, because months of payments in the bank is direct evidence you can weather a rough patch.

Our take: reserves are the quiet difference between an approval and a decline on tougher files. Two buyers with identical income and credit can get different answers when one has drained every account to close and the other kept six months of payments in savings. We have watched borderline files clear underwriting on the strength of reserves alone.

What counts as reserves and what does not

Not every dollar you own qualifies. Lenders want assets that are genuinely liquid — money you could actually reach if your income stopped. The clearest, cleanest sources are your everyday deposit accounts.

Generally counts toward reserves:

- Checking and savings balances, verified through recent statements.

- Money market accounts and CDs, treated as depository funds.

- Vested retirement funds — Fannie Mae confirms that vested funds from IRA, SEP, Keogh, and 401(k) accounts are “acceptable sources of funds for the down payment, closing costs, and reserves.” Helpfully, when they are used for reserves, “Fannie Mae does not require the funds to be withdrawn from the account(s).”

- Stocks, bonds, and mutual funds in non-retirement brokerage accounts, subject to valuation rules.

Generally does not count:

- Unvested retirement funds — money you do not yet own outright cannot be counted.

- Retirement funds you cannot withdraw — the account must permit withdrawals regardless of employment status.

- Business funds without documentation that using them will not harm the business.

- Borrowed funds, gift funds earmarked for closing, or cash you cannot source — undocumented cash is not liquid reserve in an underwriter’s eyes.

One important nuance on retirement accounts: while Fannie Mae counts vested balances, some programs and investors apply a discount — counting only a portion of the vested, withdrawable balance to account for taxes and early-withdrawal penalties. The exact treatment varies by loan type and investor, so confirm how your retirement funds will be counted before you rely on them. The principle to remember: retirement money can help, but it is usually worth less on paper than the same amount sitting in savings.

How lenders verify and season your reserves

Showing the money is only half the job. Lenders must also confirm where it came from, because reserves are meant to reflect your own stable savings — not a temporary balance staged to pass underwriting. Two rules drive most of the friction here.

The two-month look-back. Depository assets are typically verified with bank statements covering the most recent two months, roughly 60 days. That window is why loan officers say funds need to be “seasoned” — money that has quietly sat in your account for a couple of months needs no explanation.

Large-deposit documentation. Anything that lands suddenly draws scrutiny. Fannie Mae defines a large deposit as “a single deposit that exceeds 50% of the total monthly qualifying income for the loan.” If a deposit that size appears and its source is not obvious from the statement — a payroll direct deposit or a tax refund, for instance, is self-explanatory — the underwriter will ask for a paper trail proving it is not borrowed money or an undisclosed loan. A $9,000 transfer with no explanation can stall a file for days.

The practical takeaway: move money early. If you plan to shift funds from a brokerage account or consolidate savings before applying, do it well before your two-month window so the balances are seasoned and the deposits are documented.

How to build reserves and why you should not drain them to close

Because reserves are measured after closing, the goal is to reach the table with your safety cushion intact. Buyers who stretch to cover the maximum down payment sometimes arrive with strong equity but zero reserves — and on a second home or investment property, that can sink the approval outright.

A few practical moves for Colorado Springs buyers:

- Separate your closing money from your reserve money. Keep the down payment and closing costs in one account and your reserve cushion in another so it is easy to document each.

- Do not over-commit to the down payment. Putting less down and keeping cash in reserve is sometimes the stronger file, especially when reserves offset another risk factor. Weigh this against the cost of mortgage insurance; our guide on how to save for a down payment lays out the trade-offs.

- Use down payment assistance to preserve cash. Assistance programs can reduce the cash you need at closing, leaving more in reserve. See our overview of down payment assistance.

- Season deposits early. Get money into the account you will use at least two months before you apply, so it clears the look-back cleanly.

- Right-size your target price. A lower PITIA means each month of reserves costs less to hit. Running the numbers on whether you can afford a mortgage up front keeps the reserve math manageable.

Remember that reserves interact with everything else in your file. A comfortable cushion can make an underwriter more forgiving on other lines; an empty one removes your margin for error entirely.

Frequently asked questions

Are mortgage reserves the same as my down payment? No. Your down payment and closing costs are the cash you bring to closing. Reserves are what is left in your accounts afterward. Fannie Mae explicitly subtracts your funds to close before counting reserves, so the two never overlap.

How many months of reserves do I need to buy a home in Colorado Springs? For a well-qualified buyer purchasing a one-unit primary residence with a conventional loan, the requirement is frequently zero. Second homes generally require about two months of PITIA and investment properties about six months, and jumbo or non-QM loans can require more. These are general figures — confirm current requirements for your loan.

Can I use my 401(k) or IRA as reserves? Yes, vested and withdrawable retirement funds are acceptable, and Fannie Mae does not require you to actually withdraw them to count them for reserves. Be aware that some programs count only a discounted portion of the balance, so retirement money is often worth less on paper than the same amount in savings.

What is a “large deposit” and why does it matter? Fannie Mae defines it as a single deposit that exceeds 50% of your total monthly qualifying income. If the source is not clearly identified on your statement, the underwriter will ask for documentation to confirm it is not undisclosed borrowed money. Unexplained large deposits are one of the most common causes of underwriting delays.

Do reserves have to be cash sitting in the bank? Not entirely. Checking, savings, money market accounts, and CDs are the cleanest sources, but vested retirement accounts and non-retirement brokerage holdings can also count, subject to valuation and withdrawal rules. Unvested funds and undocumented business funds generally do not count.

Will strong reserves help me get approved with weaker credit or income? They can. Reserves are treated as a compensating factor — evidence you can keep paying through a disruption — so months of payments in the bank sometimes offset a higher debt-to-income ratio or a thinner credit profile. They are not a guarantee, but they meaningfully strengthen a borderline file.

This article is educational and is not personalized financial or investment advice; consider consulting a financial advisor about your own situation. Real estate values can rise or fall, and past performance is not a guarantee of future results. All figures and ranges above are general — confirm current requirements for your loan. 719 Lending is not affiliated with or endorsed by any government agency, including the FHA, VA, USDA, or CHFA. 719 Lending, NMLS #1601989. Equal Housing Opportunity. Last updated: July 2026.

Related Posts