Mortgage reserves are the liquid cash left after your down payment and closing costs, measured in months of your PITIA payment. Here is how much you need and why.

Credit, Income, and Assets: The 3 Things Every Lender Checks

Every mortgage lender evaluates three core pillars before approving your loan: your credit, your income, and your assets. Underwriters sometimes shorthand these as the “three Cs” of a file, and if you understand what each one measures, you stop guessing about whether you qualify and start building a file that gets a clean “yes.” This is the plain-English overview of what you actually need, why each pillar matters, what strengthens it, and the mistakes that quietly sink applications here in Colorado Springs and across El Paso County.

The short version: a lender is answering one question in three parts. Will you pay the loan back (credit), can you afford it month to month (income), and do you have the cash to close and cushion (assets)? Get all three in shape before you shop, and the rest of the process gets dramatically easier.

Pillar 1: Credit — will you pay it back?

Credit is your track record of borrowing and repaying. For a mortgage, lenders don’t just glance at one number from a free app. They typically pull a tri-merge credit report that combines your files from the three bureaus (Equifax, Experian, and TransUnion), then use the middle of the three scores to price and qualify your loan. On a joint application, they generally take the lower of the two borrowers’ middle scores.

The scores lenders see are usually not the FICO 8 or VantageScore you check for free. Mortgage files rely on older, mortgage-specific models, commonly FICO Score 2, FICO Score 4, and FICO Score 5. That is why the number your credit-card app shows can differ from the score a loan officer quotes. As of 2026 the Federal Housing Finance Agency allows approved lenders, on an interim basis, to choose between Classic FICO and VantageScore 4.0 for loans sold to Fannie Mae and Freddie Mac, and to use either tri-merge or bi-merge reporting, with newer models like FICO 10T planned for future use (this landscape is changing — confirm current requirements).

Why credit matters

Your score does two jobs. First, eligibility: each loan program has a minimum. Second, and just as important, pricing. A stronger score generally earns better pricing, while a weaker score costs more over the life of the loan. That is why two neighbors with identical incomes can be offered meaningfully different terms.

What strengthens your credit

- Pay every bill on time. Payment history is the single largest factor in your score.

- Lower your credit-card utilization. Carrying small balances relative to your limits helps; maxed-out cards hurt.

- Leave old accounts open. Length of history counts, so don’t close your oldest card right before applying.

- Avoid new debt while shopping. Financing a car or opening store cards mid-process can drop your score and your buying power.

Common credit mistakes

The classic errors are opening new credit right before or during an application, letting a single payment go 30 days late, and disputing accurate items in a panic, which can temporarily freeze a tradeline. Another is assuming your free app score is what the lender will use. Pull your actual mortgage-model scores or ask a broker to run a soft check early, so there are no surprises.

Pillar 2: Income — can you afford the payment?

Income, sometimes called capacity, measures whether your monthly cash flow can comfortably carry the new payment plus your other obligations. Fannie Mae’s underwriting standards put it plainly: “A stable and predictable flow of income is a foundational element in loan underwriting,” and the lender must document that income “is stable, has a documented history of receipt, and is reasonably expected to continue.”

The math tool underwriters use is your debt-to-income ratio (DTI). As the Consumer Financial Protection Bureau explains, you add up your monthly debt payments and divide by your gross monthly income. If your future mortgage plus car loan and other minimums total $2,000, and you earn $6,000 a month before taxes, your DTI is about 33 percent. Many loan programs treat a DTI at or below 43 percent as a common guideline, though this varies widely: some programs allow considerably higher with compensating factors, and the CFPB notes different loan products and lenders set different limits (this is a general benchmark, not a hard federal cap — confirm current guidelines for your situation).

Why income matters and how history works

Lenders want to see that the income will keep coming. For most wage earners, a roughly two-year look-back at employment and earnings is the norm, which is why underwriters ask for recent pay stubs, W-2s, and sometimes tax returns. The goal is not to catch you out; it is to confirm the paycheck is stable and likely to continue.

How self-employed income differs

If you own 25 percent or more of a business, Fannie Mae treats you as self-employed, and the documentation is deeper. Instead of pay stubs, underwriters analyze your personal and often business tax returns, typically over a two-year history, to confirm the income is stable and likely to continue. Business write-offs that lower your taxable income can also lower your qualifying income, so self-employed borrowers should plan ahead. Our self-employed mortgage guide walks through how that calculation actually works and how to present a strong file.

What strengthens your income pillar

- Pay down or pay off high-minimum debts (cards, personal loans) to lower your DTI.

- Avoid new monthly obligations before and during the process — a new car payment can shrink the home price you qualify for.

- Keep your job history steady. Staying in the same field and documenting bonuses or overtime consistently helps.

- Document everything. Deposit and keep records of all income, especially if you are self-employed or paid in cash.

Pillar 3: Assets — do you have the cash to close and cushion?

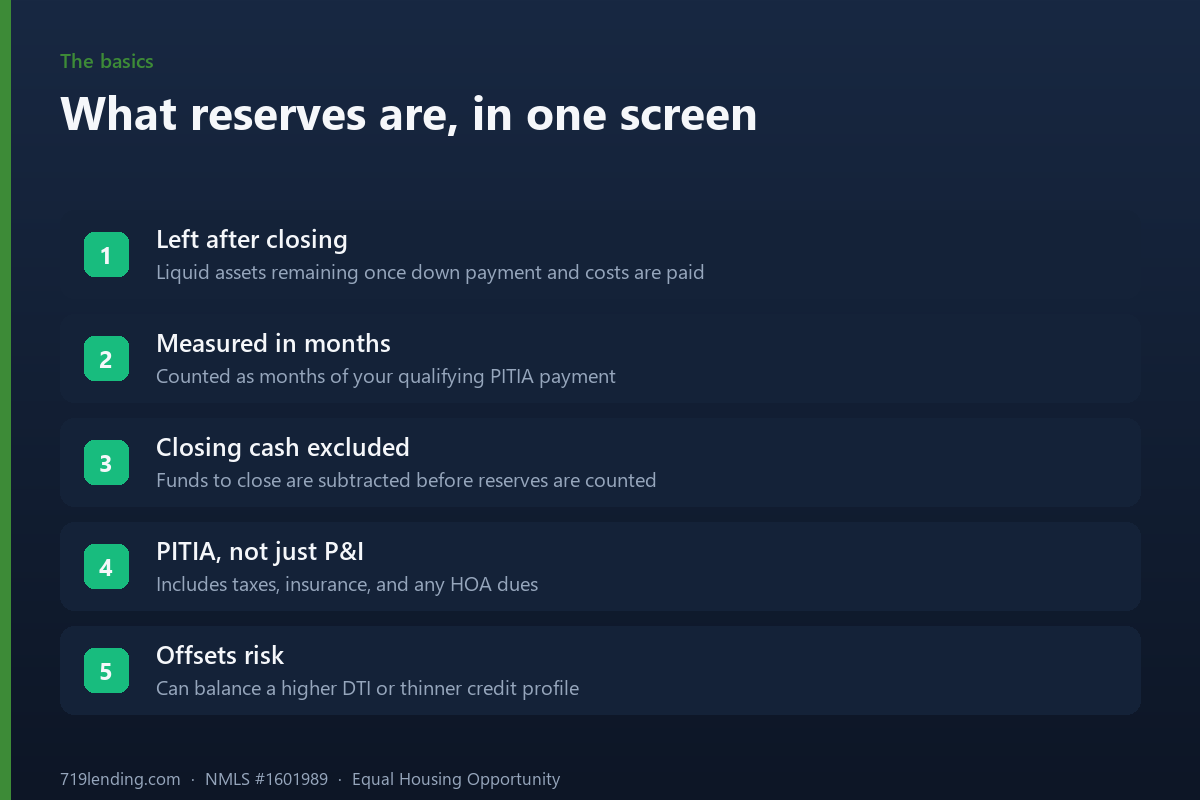

Assets, sometimes called capital, are the documented funds you bring to the table. They cover three things: your down payment, your closing costs, and your reserves — the cash cushion left over after closing. Every dollar has to be sourced and seasoned, meaning the lender can trace where it came from and confirm it is genuinely yours.

Reserves are worth understanding because borrowers often overlook them. Fannie Mae measures reserves “by the number of months of the qualifying payment amount for the subject mortgage (based on PITIA)” — that is principal, interest, taxes, insurance, and any association dues — that you could cover from your remaining assets after closing. Importantly, Fannie Mae sets no minimum reserve requirement for a one-unit primary residence in most cases, while second homes, two- to four-unit properties, and investment properties do require documented reserves (often two months for a second home and six for investment or multi-unit). Liquid financial reserves can include checking and savings, stocks, bonds, mutual funds, certificates of deposit, money market funds, and the vested balance in a retirement account, though lenders often count retirement funds at a discounted value. Our deeper explainer on mortgage reserves breaks down how many months different programs expect.

Why assets matter

Assets prove two things: that you can actually fund the purchase, and that you have a buffer if life throws a curveball after you move in. A borrower with strong reserves is a lower risk, which is one reason reserves can help offset a weaker spot elsewhere in the file.

What strengthens your assets

- Build a documented paper trail. Keep funds in your accounts and avoid large, unexplained cash deposits, which trigger sourcing questions.

- Use gift funds correctly. Gifts from family are often allowed but need a signed gift letter and a clear transfer trail.

- Explore down payment assistance. Colorado programs can bridge the gap; see our overview of how much a down payment really costs.

- Leave a cushion. Don’t drain every account to the last dollar for the down payment; underwriters want to see reserves remain.

Common asset mistakes

The biggest one is moving money around right before or during underwriting. Transfers between accounts, cash deposits, or a sudden windfall all have to be explained and documented. Another is forgetting closing costs, which in El Paso County commonly run a few percent of the purchase price on top of the down payment. Plan for the full cash-to-close figure, not just the down payment.

How the three pillars work together

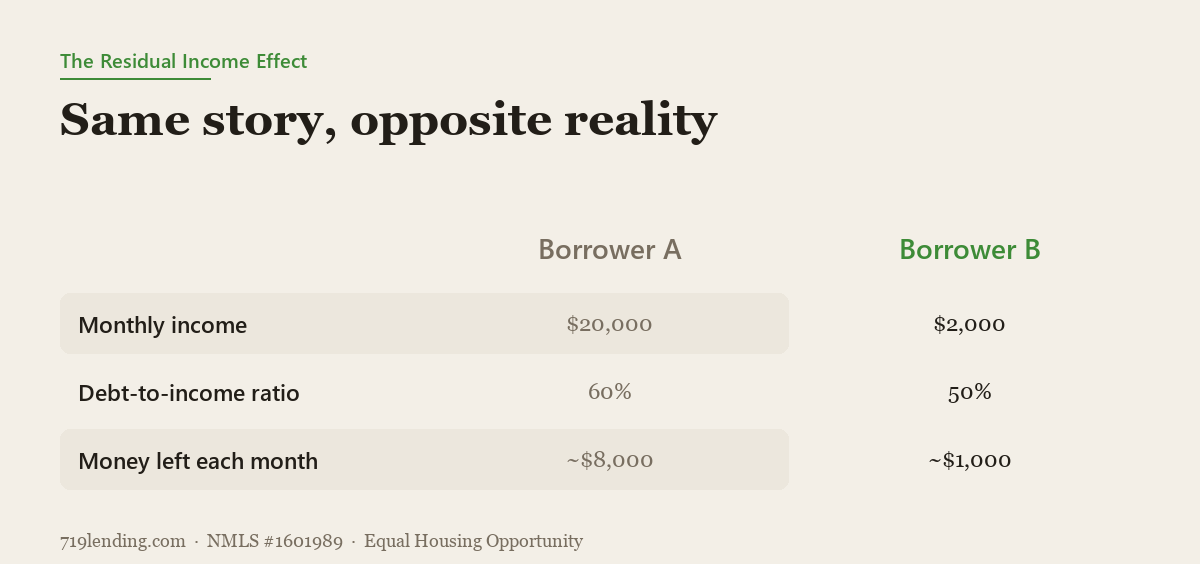

Here is the part borrowers miss: credit, income, and assets are not pass-fail gates evaluated in isolation. Underwriters look at the whole picture, and strength in one pillar can offset a weakness in another. Deep reserves can support a borrower with a slightly higher DTI. Very low debt can make room for a shorter credit history. A large down payment reduces risk across the board.

This is exactly why lenders often teach the “four Cs of mortgage approval” — credit, capacity, capital, and collateral (the property itself). The three pillars in this article are the first three Cs; collateral, established through the appraisal, is the fourth, and these compensating factors are weighed together rather than in isolation. If you want to see how it all fits together, that companion piece is the natural next read.

Our take: get all three pillars in shape before you shop, not after you fall in love with a house. The borrowers who close smoothly in Colorado Springs are the ones who pulled their real scores, cleaned up their DTI, and built a documented cash cushion months ahead of time. A quick pre-approval conversation early can show you exactly which pillar to strengthen, and by how much. When you’re ready to map your own numbers, use our tool to estimate what home price you can afford, then talk with a Colorado Springs mortgage broker who can pressure-test all three pillars against real programs.

Frequently asked questions

Which credit score do mortgage lenders actually use? Lenders typically pull a tri-merge report from the three bureaus and use the middle score, usually from older mortgage-specific FICO models (commonly FICO 2, 4, and 5). That number can differ from the free score in your banking app, which usually shows FICO 8 or VantageScore.

What debt-to-income ratio do I need to qualify? A DTI at or below 43 percent is a common program guideline, calculated as total monthly debt payments divided by gross monthly income. It is not a hard federal cap — many programs allow higher DTIs with compensating factors like strong reserves. This is general; confirm current guidelines for your loan.

What counts as assets, and what are reserves? Assets are documented funds for your down payment, closing costs, and reserves. Reserves are the cash cushion left after closing, measured in months of your full housing payment (PITIA). Checking, savings, investments, and vested retirement accounts can all count, though retirement funds are often counted at a discounted value.

How is self-employed income evaluated differently? If you own 25 percent or more of a business, lenders analyze your tax returns rather than pay stubs, usually over a two-year history, to determine stable and continuing income. Business deductions that lower taxable income can also lower your qualifying income.

Can strength in one pillar make up for a weakness in another? Often, yes. Underwriters review the full file, so strong reserves or a large down payment can help offset a higher DTI or a shorter credit history. That is the logic behind the broader four Cs of approval.

What should I do first if I want to buy in Colorado Springs? Pull your real mortgage scores, add up your monthly debts to estimate DTI, and confirm your documented cash-to-close plus reserves. Then get a pre-approval so a loan officer can tell you which pillar, if any, needs work before you make offers.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by any government agency, including FHA, VA, USDA, or CHFA. Figures and ranges above are general — confirm current guidelines for your situation. This article is educational and not personalized financial, investment, or lending advice; consult a qualified professional about your circumstances. Home values can rise or fall, and past performance is not a guarantee of future results. Last updated: July 2026.

Related Posts