The real question is not “what is your debt-to-income ratio?” It is “how many actual dollars does your household have left after the mortgage and every other bill is paid?” In our professional opinion at 719 Lending, that second number, residual income, is a truer measure of whether you can genuinely afford a home than the debt-to-income (DTI) ratio alone. We call the gap between the two the Residual Income Effect.

Debt-to-income is the number everyone talks about. It is clean, it is universal, and every mortgage program uses it. But a ratio is blind to something a household can never ignore: the absolute number of dollars left in the checking account at the end of the month. Two borrowers can have wildly different financial realities and still look identical, or even backwards, on a DTI report. Here in Colorado Springs, where a huge share of our clients are active-duty service members at Fort Carson, Peterson and Schriever, veterans, and military families, this distinction is not academic. It is the difference between a payment that fits and a payment that quietly strangles a budget.

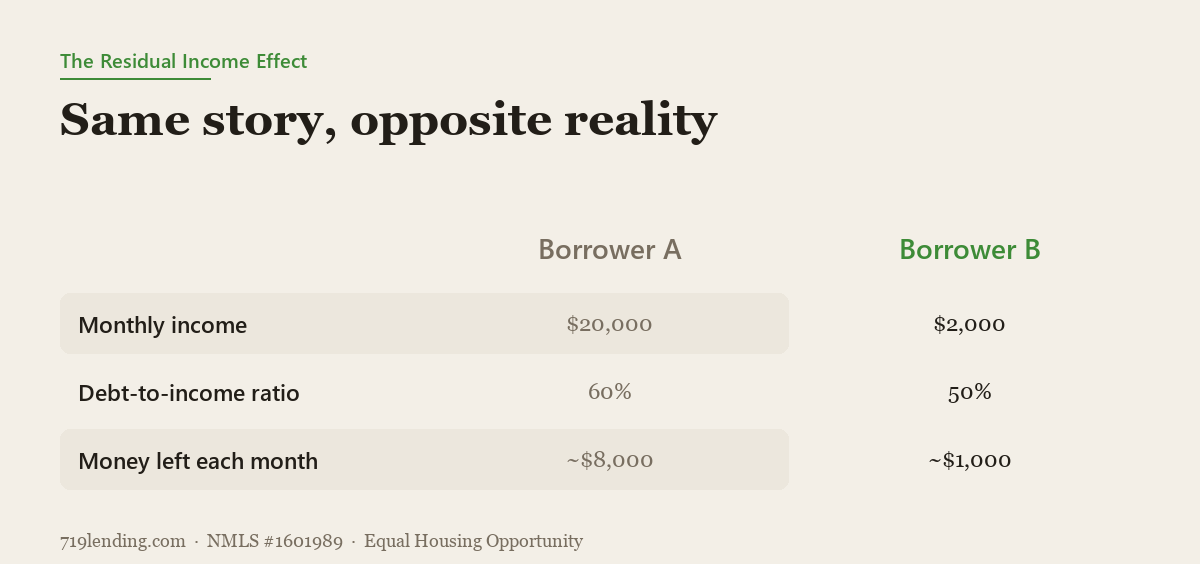

Borrower B has the lower, better-looking DTI, yet Borrower A has roughly eight times more actual money left over each month. That gap is the Residual Income Effect.

The Residual Income Effect: same story, opposite reality

Let us make this concrete with two borrowers. The math is a simplified illustration, but it exposes exactly what a ratio hides.

Borrower A earns $20,000 per month and carries a 60% DTI. Sixty percent of $20,000 is about $12,000 in monthly debts, which leaves roughly $8,000 per month of real cash.

Borrower B earns $2,000 per month and carries a 50% DTI. Fifty percent of $2,000 is about $1,000 in monthly debts, which leaves roughly $1,000 per month.

Look at what happened. Borrower B has the lower, better-looking DTI, yet Borrower A has roughly eight times more actual money left over every single month. The prettier ratio belongs to the household with dramatically less cushion. That is the Residual Income Effect in one snapshot: a lower ratio does not mean more affordability.

Measure

Borrower A

Borrower B

Monthly income

$20,000

$2,000

Debt-to-income ratio

60%

50%

Monthly debts

~$12,000

~$1,000

Money left each month

~$8,000

~$1,000

This is a simplified illustration. Real underwriting also weighs federal and state taxes, utilities, maintenance, and, critically, household size, because $1,000 left over means one thing for a single person and something very different for a family of five. But the core point survives all of that nuance: the ratio told you Borrower B was the safer bet, and the dollars told you the opposite.

See it for your own budget. Run your numbers through our VA residual income calculator to see how much your household would actually have left over each month — the figure a VA loan weighs directly and most other programs overlook.

What debt-to-income actually measures, and what it misses

To be fair to DTI, it is a genuinely useful tool, and we use it every day. The Consumer Financial Protection Bureau defines your debt-to-income ratio as all of your monthly debt payments divided by your gross monthly income. Add up the mortgage, the car payment, the student loans, the credit card minimums, divide by what you earn before taxes, and you get a percentage. Lenders lean on it because it is fast, standardized, and reasonably predictive across large pools of borrowers.

The problem is structural, not accidental. A ratio, by design, throws away the dollar amounts and keeps only the proportion. It cannot tell the difference between 50% of $2,000 and 50% of $20,000, even though those two households live in completely different financial universes. It also has no idea how many people that leftover money has to feed, clothe, and house. Residual income captures exactly what the ratio discards: the real dollars, measured against the real size of the household.

Why residual income deserves more weight than it gets

Our take, and we want to label this clearly as opinion: in our professional view at 719 Lending, residual income deserves more weight across the mortgage industry than it currently receives. This is the informed opinion of a broker team that sits across the table from real Colorado Springs households every week, not an established regulatory standard. Most of the industry treats DTI as the headline number and residual income as an afterthought. We think that emphasis is backwards for a meaningful slice of borrowers.

Here is the honest boundary between fact and opinion. The fact is that one major mortgage program already requires a minimum residual income and has for decades. The opinion is that the rest of the industry would serve borrowers better by giving that same measure more standing. We are not saying DTI should be thrown out. We are saying the money left over tells you something the ratio simply cannot, and that “something” is often the whole story.

VA is the only major program that requires a minimum residual income openly, measuring real leftover dollars against region, household size, and loan amount.

What VA residual income actually measures

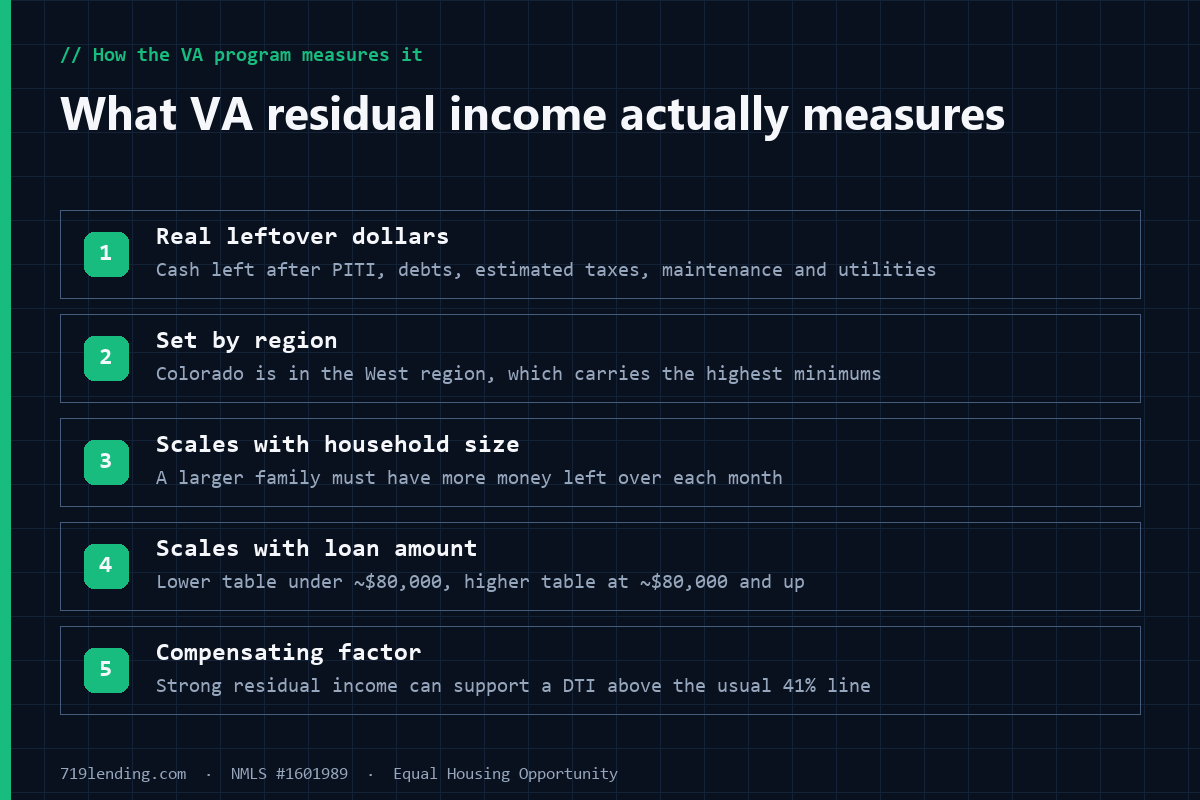

The VA loan program is, in fact, the only major mortgage program that requires a minimum residual income openly. This is not marketing language; it is written into the VA Lender’s Handbook (VA Pamphlet 26-7), and the program itself is administered through the VA home loan program. For our military community, this is one of the most underappreciated strengths of the VA benefit, and it is a direct reason the program performs so well.

Here is how VA residual income works:

It measures real leftover dollars. VA calculates the money a household has left each month after the mortgage payment (principal, interest, taxes, and insurance), all other monthly debts, an estimate for federal and state taxes, and an estimate for home maintenance and utilities.

It is set by region. VA publishes different minimums for the Northeast, Midwest, South, and West. Colorado sits in the West region, which carries the highest minimums because living costs run higher.

It scales with household size. A larger family must have more money left over. The requirement is not one flat number; it grows with the number of people in the home.

It scales with loan amount. VA uses a lower table for loans under roughly $80,000 and a higher table for loans of roughly $80,000 and up.

To put real figures on it, for the West region on loans of roughly $80,000 and above, the published monthly minimums run about $491 for a household of one, $823 for two, $990 for three, $1,117 for four, and $1,158 for five (general, confirm current). These are floors, not targets, and they exist so that a veteran or service member is not approved for a payment that looks fine on paper but leaves nothing to live on.

Why the VA program can approve higher DTIs and still perform

This is where residual income stops being a technicality and starts being the entire point. Because VA verifies that a household has genuine dollars left over, the program can responsibly approve borrowers at higher DTIs than other programs typically allow, and those loans still perform. When a VA borrower’s residual income runs well above the guideline (VA recognizes exceeding it by 20% as a meaningful cushion), strong residual income becomes the key compensating factor that supports a DTI above the usual 41% comfort line.

Think back to our two borrowers. A rigid DTI-only rulebook might wave through Borrower B’s 50% ratio and hesitate on Borrower A’s 60%, exactly backwards from where the real risk sits. A residual-income lens catches that. VA has been underwriting this way for decades, and the program is historically associated with strong loan performance and low foreclosure rates, which we view as real-world evidence that measuring the dollars left over works.

VA requires it, FHA may consider it, the rest mostly do not

To keep the “only one” claim precise, here is exactly how each major program treats residual income:

VA: requires it. A minimum residual income is a hard, published requirement on every VA loan.

FHA: may consider it.HUD Handbook 4000.1 lists residual income only as anoptional compensating factor in manual underwriting. Notably, FHA explicitly modeled its residual-income calculation on the VA’s tables in Chapter 4 of the VA handbook, but it stops short of requiring a minimum.

Conventional (Fannie Mae and Freddie Mac): does not require it. These programs lean on ratios, primarily DTI, rather than a residual-income floor.

USDA: does not require it. USDA also underwrites primarily to ratios rather than a residual-income minimum.

So the accurate, defensible statement is this: VA requires a minimum residual income openly, FHA may consider it as an optional compensating factor, and conventional and USDA loans mostly do not use a residual-income minimum at all. That is precisely why we think the VA model deserves a wider audience.

What the Residual Income Effect means for Colorado Springs buyers

If you are buying near Fort Carson, Peterson Space Force Base, or Schriever, or anywhere along the Front Range, the practical takeaway is simple. Do not let a clean DTI convince you a payment is comfortable, and do not let a slightly high DTI convince you a payment is impossible. Ask the better question: after this mortgage and everything else, how many real dollars are left, and is that enough for the size of my household and the cost of living here?

That is the conversation we actually have with clients. We will run your DTI, of course, because every program requires it. But we will also sit down and look at the dollars left over, the way the VA program does by design, so you are choosing a payment that fits your life and not just your ratio. If you want to understand where your capacity really sits, our guides on what home price you can afford and how income functions as capacity in a mortgage are a good place to start, and capacity is one of the pillars we break down in the four C’s of mortgage approval.

Residual income is also why reserves matter, why student-loan payments hit DTI harder than people expect, and why the down-payment decision changes your monthly cushion. Our resources on mortgage reserves and on how student loans affect qualifying dig into those pieces.

Talk to us about a VA loan and whether you truly fit a payment. If you are a veteran, service member, or military family, the VA benefit was built around exactly this idea, and it is our flagship expertise. Learn more about the program on our VA loan in Colorado Springs page, or reach out directly to our Colorado Springs mortgage broker team. We will help you look past the ratio to the dollars that actually decide whether a home is affordable.

Frequently asked questions

What is residual income? Residual income is the actual dollars a household has left over each month after paying the mortgage (principal, interest, taxes, and insurance), all other debts, an estimate for taxes, and an estimate for maintenance and utilities. Unlike DTI, it measures real money remaining rather than a proportion.

Which loan programs use residual income? The VA loan program requires a minimum residual income openly. FHA (HUD Handbook 4000.1) lists it only as an optional compensating factor in manual underwriting. Conventional (Fannie Mae and Freddie Mac) and USDA loans mostly rely on ratios like DTI rather than a residual-income minimum.

Is residual income more important than DTI? In our professional opinion at 719 Lending, residual income is often a truer measure of real affordability because it captures the actual dollars left and the household’s size, which a DTI ratio ignores. That is our informed view, not a universal industry rule. Every program still uses DTI, so both numbers matter.

What is the VA’s residual income requirement? VA sets minimum residual income by region (Northeast, Midwest, South, West), household size, and loan amount (a lower table under roughly $80,000, a higher table at roughly $80,000 and up). Colorado is in the West region. For West-region loans of about $80,000 and up, figures run roughly $491 for one person up to $1,158 for five (general, confirm current).

Can a high DTI still get approved? Yes, particularly on a VA loan. When a borrower’s residual income runs comfortably above the VA guideline, that strong residual income acts as a compensating factor that can support a DTI above the usual 41% line. Approval is never guaranteed and always depends on the full file.

Why does the VA loan perform so well at higher DTIs? Because VA verifies that borrowers have genuine dollars left over after all obligations, not just an acceptable ratio. That focus on real leftover cash is widely credited as a reason VA loans are historically associated with strong performance and low foreclosure rates.

719 Lending, NMLS #1601989. Equal Housing Opportunity. The VA loan program is a U.S. government program; 719 Lending is not affiliated with or endorsed by the VA or any government agency. Figures shown are general illustrations, confirm current amounts and guidelines with us, as programs and published tables change. Nothing here guarantees approval, a specific residual income figure, or any rate. Last updated: July 2026.

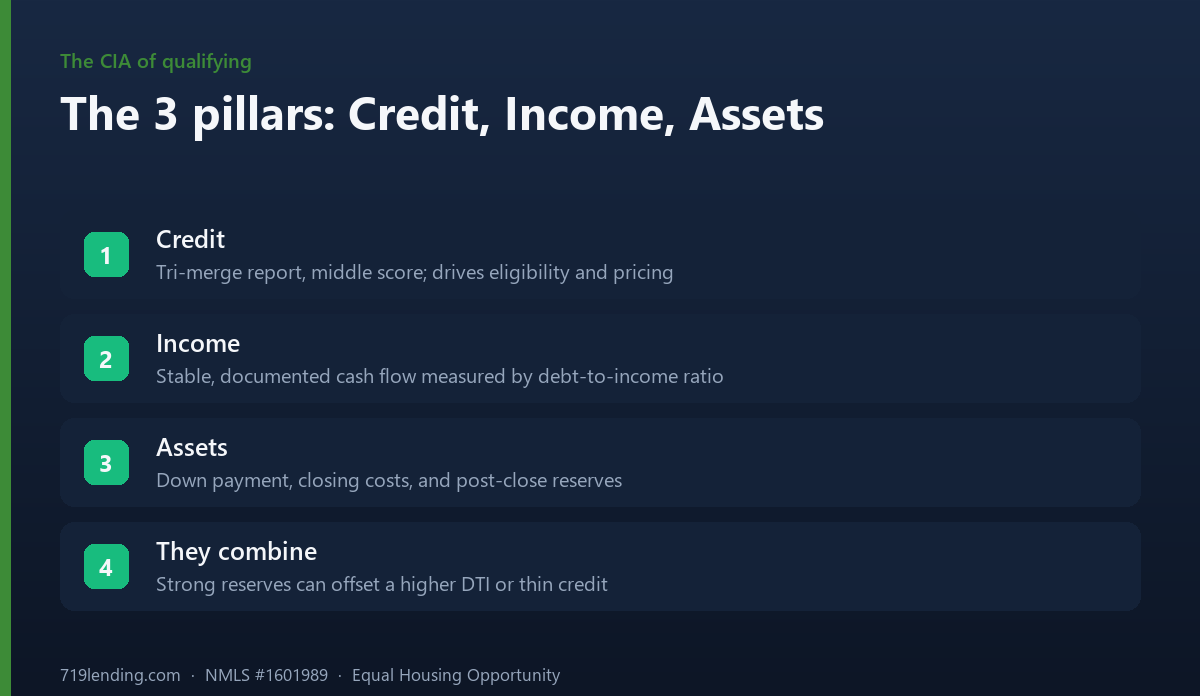

Credit, income, and assets are the three pillars every mortgage lender checks. Here is what each one means, why it matters, and how to strengthen it before you apply in Colorado Springs.

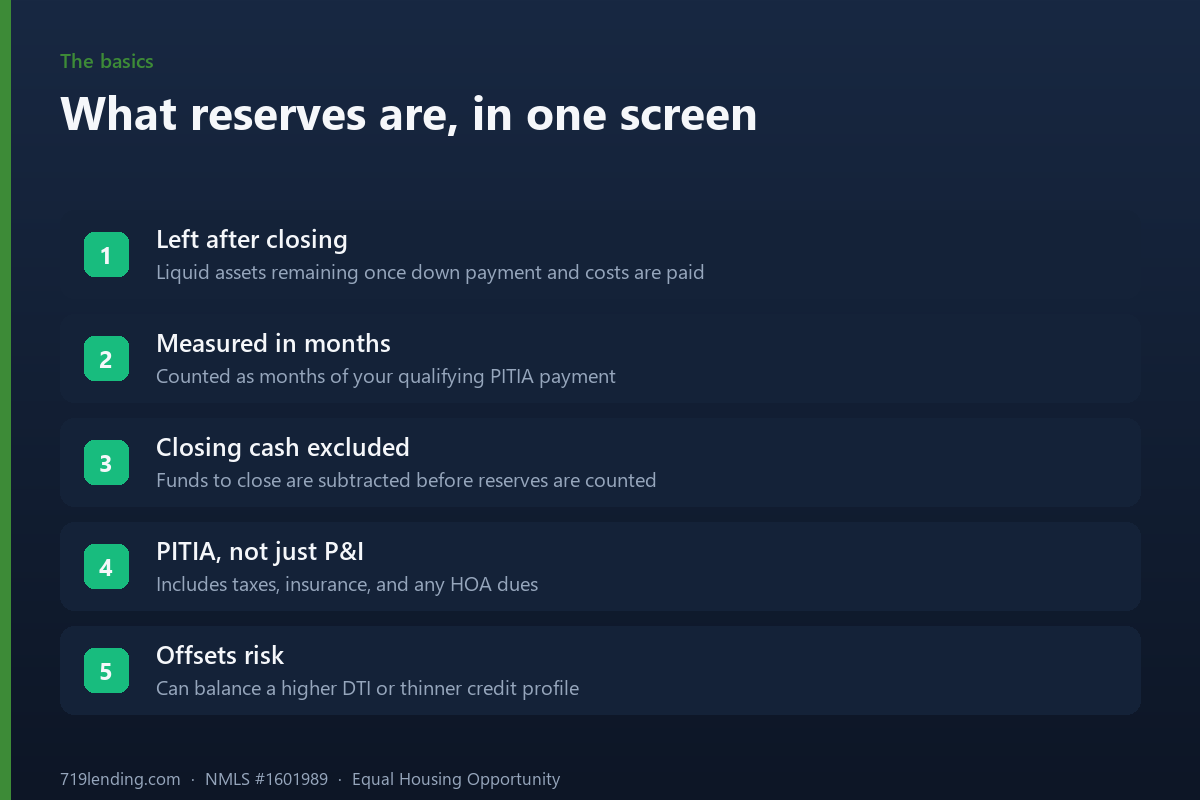

Mortgage reserves are the liquid cash left after your down payment and closing costs, measured in months of your PITIA payment. Here is how much you need and why.

A great credit score alone doesn't approve a mortgage. Learn the Four C's underwriters actually weigh — Credit, Capacity, Capital, Collateral — and how a Colorado Springs broker reads the whole file.