An FHA construction loan is a one-time-close (construction-to-permanent) mortgage: you sign a single set of loan documents before construction begins, put down as little as 3.5% with a qualifying credit score, build with a licensed general contractor, and the same loan automatically becomes your permanent 15- or 30-year mortgage once the home is finished — no second closing and no re-qualifying. The rules below come straight from HUD Handbook 4000.1, the FHA’s underwriting rulebook, so you know exactly what a lender must document before funding a build in Colorado Springs, El Paso County, or anywhere in Colorado.

What an FHA construction-to-permanent loan actually is

HUD defines Construction to Permanent (CP) as “the construction of a dwelling on land owned or being purchased by the Borrower,” combining “the features of a construction loan with that of a traditional long-term permanent residential Mortgage using a single mortgage closing prior to the start of construction.” That single-closing structure is the whole point: the interim construction financing and the permanent FHA-insured mortgage are set up together, up front, in one transaction.

Two practical consequences follow. First, you lock your loan terms before a single nail is driven — you are not exposed to a second underwrite after the home is built. Second, the mortgage is not eligible for FHA insurance until after the final inspection or the local certificate of occupancy (CO) is issued, whichever is later, so the loan carries construction-only terms during the build and converts afterward. FHA’s cousin program, Building on Own Land, uses a two-step close instead; if you want the single-closing version, CP is the one to ask your broker about.

FHA construction loan down payment: 3.5% of the lesser of value or cost

The FHA down payment on a construction loan follows the same Minimum Required Investment (MRI) as any FHA purchase: at least 3.5% of the Adjusted Value with a minimum decision credit score of 580 or higher. Borrowers with scores of 500–579 are capped at 90% loan-to-value, meaning a 10% down payment; below 500, FHA financing is not available. (Individual lenders often set higher score overlays on construction files — general, confirm current.)

The twist unique to construction is how “value” is measured. FHA requires the lender to “use the lesser of the appraised value or the documented Acquisition Cost to determine the Adjusted Value,” then apply the purchase LTV percentage to that lesser figure. Your 3.5% is calculated against whichever is lower — the finished-home appraisal or your documented total cost to acquire land and build. Documented Acquisition Cost includes the builder’s price (or the sum of subcontractor bids and materials if you already own the lot), borrower-paid options and construction costs not in the builder’s price, closing costs on any interim land financing, and a land-value component described next.

How FHA counts your land — the six-month rule

Land equity can help satisfy your down payment, but FHA values the land differently depending on how long you have held it. Under Handbook 4000.1, the land component of Acquisition Cost is:

Not yet purchased, or owned six months or less at case-number assignment — the lesser of the cost of the land or its appraised value.

Owned more than six months at case-number assignment, or received as an acceptable gift — the appraised value of the land.

This matters for Colorado Springs buyers who bought a lot in Falcon, Monument, or the Meridian Ranch area a while back and have watched it appreciate: if you have owned it more than six months, FHA lets you credit the current appraised value, which can meaningfully reduce the cash you bring to closing. If the land was gifted, the lender must confirm the donor is not a prohibited source and collect standard gift documentation.

Core FHA construction-to-permanent rules per HUD Handbook 4000.1. General, confirm current.

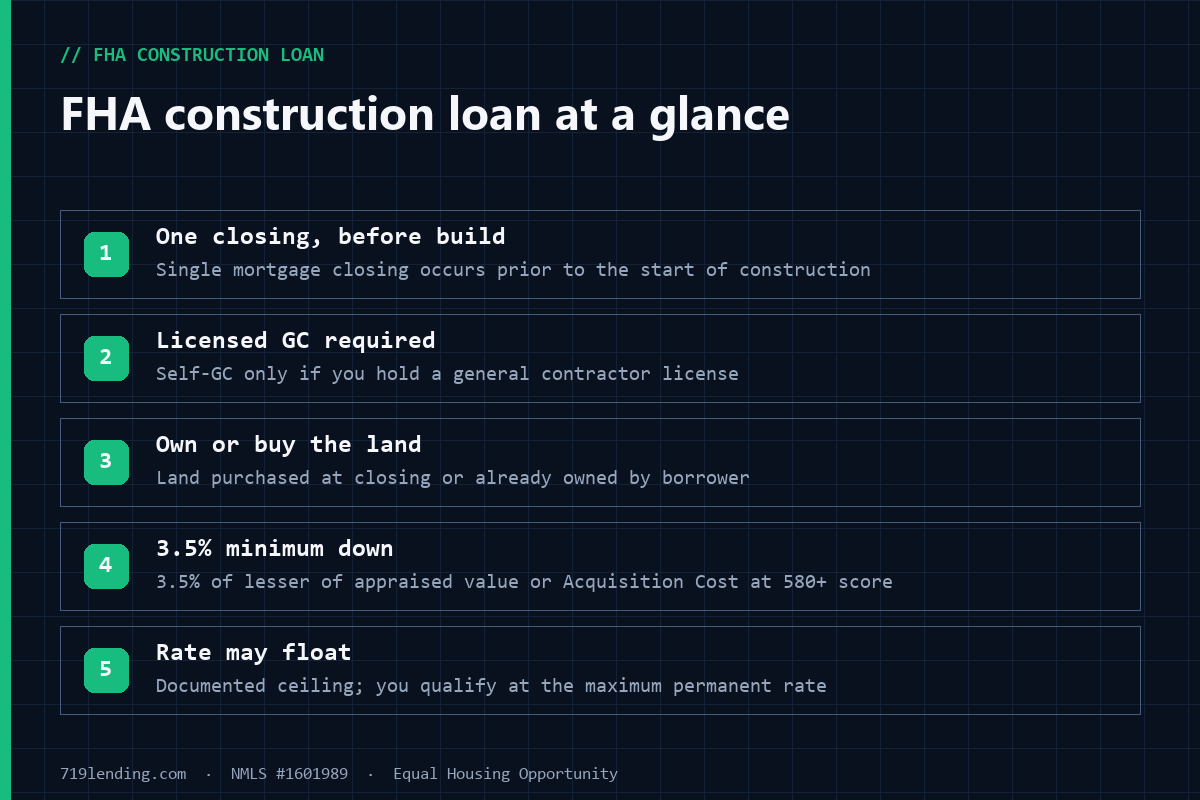

FHA construction loan at a glance

Every FHA construction loan runs on the same core mechanics, verified against HUD Handbook 4000.1:

One closing, before construction. A single mortgage closing occurs prior to the start of construction; there is no separate permanent-loan closing.

Licensed general contractor required. You must contract with a licensed general contractor; you may act as your own GC only if you are yourself a licensed general contractor.

Own or buy the land at closing. The borrower must either be purchasing the land at the construction-loan closing or already own it.

3.5% minimum down. Minimum Required Investment is 3.5% of Adjusted Value (the lesser of appraised value or documented Acquisition Cost) at 580+ credit.

Your interest rate can float during the build

FHA anticipates that rates move during a months-long construction period. During construction, “the interest rate may be variable,” but the lender and borrower must sign an agreement that documents the range in which the rate may float, documents the point of rate lock-in, specifies that the permanent mortgage “will not exceed a specific maximum interest rate,” and permits you to lock at a lower rate if one becomes available and you have not already locked.

The underwriting safeguard is strict: the lender must qualify you “for the Mortgage at the maximum rate at which the permanent Mortgage may be set.” In plain terms, FHA makes sure you can afford the worst-case rate before it approves the file — so a rate that ticks up during your build does not blow up your approval after the home is done.

Our take: The float-with-a-ceiling design is one of the most borrower-friendly features in the FHA toolbox, and it is under-explained by most lenders. Because you qualify at the ceiling, a Colorado Springs buyer who breaks ground in a rising-rate stretch is not gambling the entire approval on where rates land at completion. We think that certainty is worth as much as the low down payment for first-time builders.

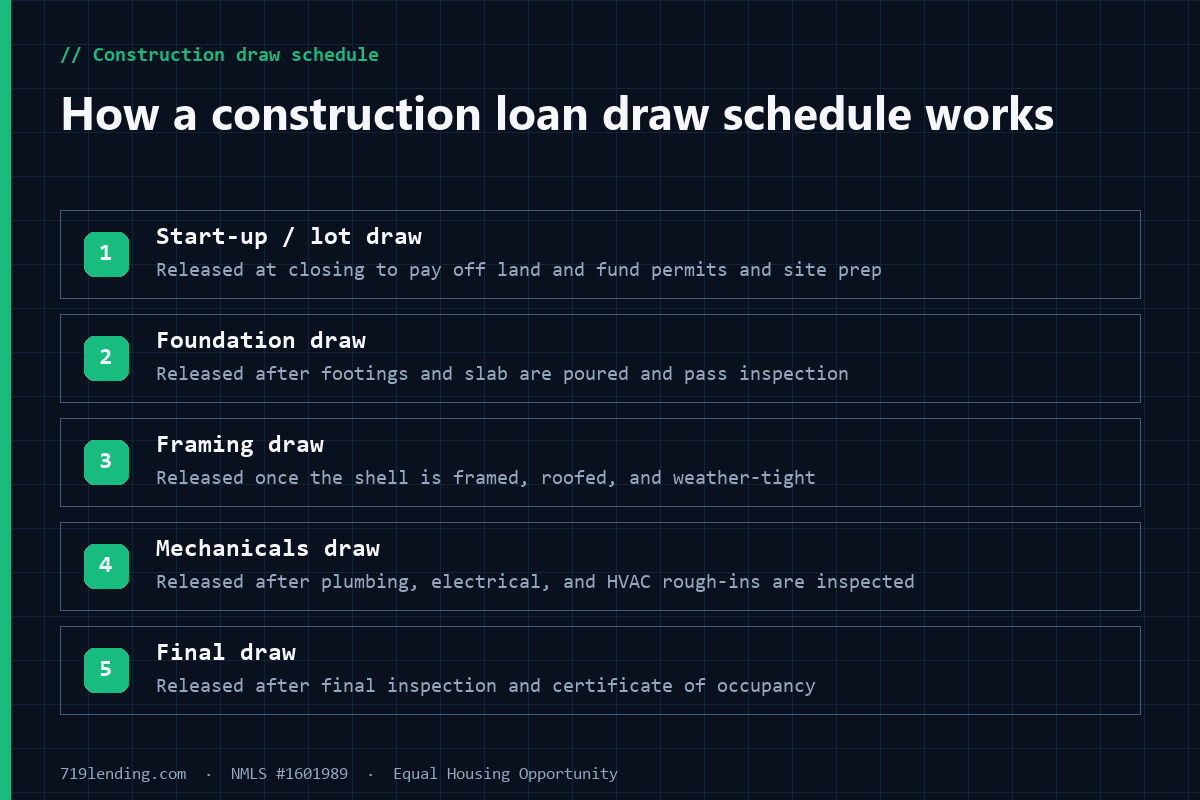

How the money is released: the construction escrow and draws

At closing, after funds are disbursed to buy the land, “the balance of the mortgage proceeds must be placed in an escrow account to be disbursed as construction progresses.” The rule that protects you most: the lender “must obtain the Borrower’s written authorization for each draw prior to disbursing funds to the contractor.” No draw goes to your builder without your sign-off. When construction is complete, the escrow account must be fully extinguished, and any leftover funds are applied to your permanent loan’s principal balance rather than pocketed by anyone.

The build itself must clear FHA’s new-construction inspection standard. For proposed site-built housing, that means either copies of the building permit and the certificate of occupancy, or three inspections — footing, framing, and final — performed by a qualified inspector such as an ICC-certified combination inspector or the local authority having jurisdiction. In El Paso County, the Pikes Peak Regional Building Department handles permits and inspections, so most Colorado Springs builds satisfy this through the permit-and-CO path.

When your mortgage starts amortizing — the 60-day rule

You do not start making full principal-and-interest payments the day the roof goes on. Under Handbook 4000.1, “Amortization of the permanent Mortgage must begin no later than the first of the month following 60 Days from the date of the final inspection or issuance of the CO.” The loan must also be endorsed for FHA insurance within 60 days of the final inspection or CO, whichever is later. That window gives the lender time to complete the title update, confirm the construction escrow was fully drawn, and convert your file to permanent status.

Amortization begins within ~60 days of final inspection or CO. General, confirm current.

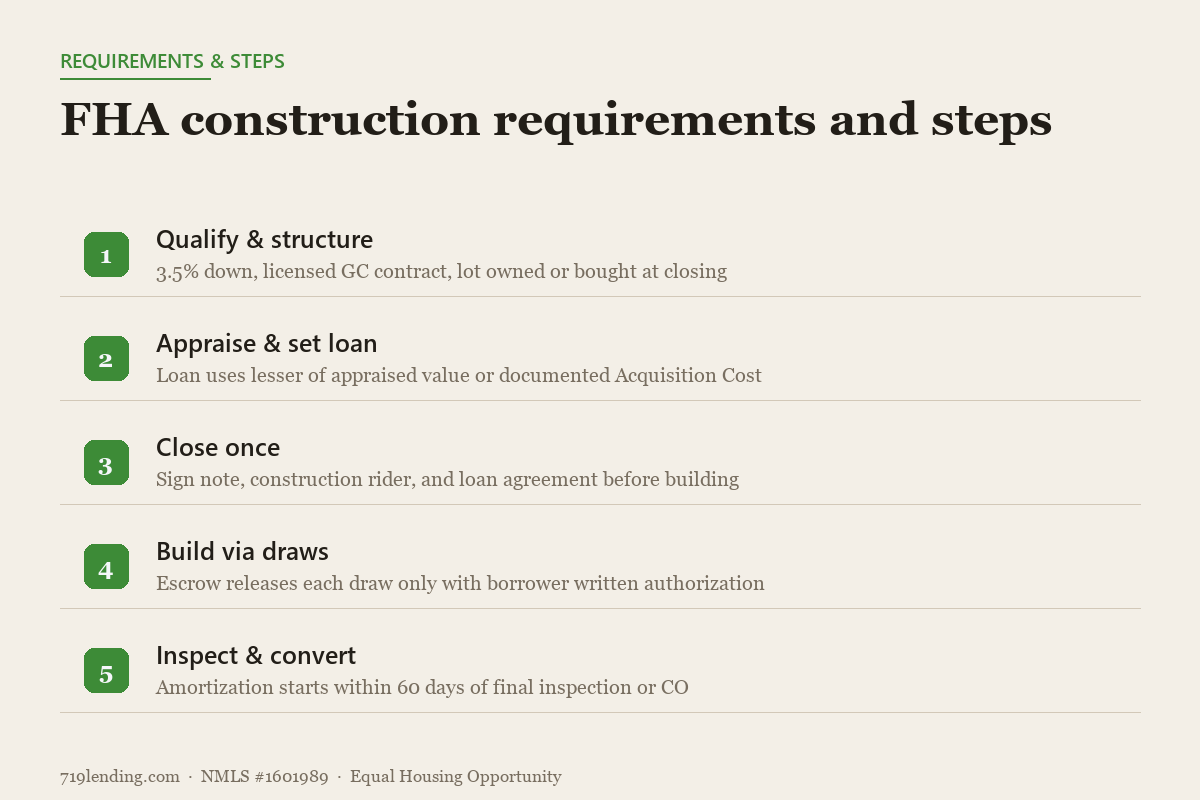

FHA construction requirements and steps

Here is the sequence an FHA construction-to-permanent file follows, from application to first payment:

Qualify and structure. Verify 3.5% down (580+ score), a licensed GC contract, and a lot you own or will buy at closing.

Appraise and set the loan. The finished-home appraisal and documented Acquisition Cost are compared; the loan uses the lesser figure.

Close once, before building. Sign the note, construction rider, and construction loan agreement in a single closing.

Build with authorized draws. Funds release from escrow as work progresses, each draw requiring your written authorization.

Inspect and convert. Final inspection or CO triggers conversion; the loan is endorsed and begins amortizing within the 60-day window.

FHA mortgage insurance on a construction loan

Because it is an FHA loan, mortgage insurance applies. The Upfront Mortgage Insurance Premium (UFMIP) is 1.75% of the base loan amount and may be financed into the loan; lenders “must remit upfront MIP within 10 calendar days of the mortgage closing or disbursement date, whichever is later.” The annual MIP for most new FHA borrowers is 0.55% (per Mortgagee Letter 2023-05, effective for endorsements on or after March 20, 2023), paid monthly. These figures are general — confirm current with your broker, as premiums are subject to change by HUD.

How it fits Colorado Springs and El Paso County

Colorado Springs remains a strong new-construction market, and the FHA loan limit generally accommodates it. For 2026, the FHA one-unit “floor” is $541,287 (per HUD Mortgagee Letter 2025-23, effective for case numbers on or after January 1, 2026), and El Paso County sits at that floor because local median prices fall below the high-cost threshold. With the Springs’ median sale price running in the mid-$400,000s, most Fort Carson-area families, first-time builders, and move-up buyers building a modest custom home fit comfortably under the cap. If you are weighing your options, it is worth understanding how the FHA loan compares with conventional, VA, and USDA construction financing before you commit. Pair the CP loan with the state’s down-payment and buyer assistance and it becomes one of the more accessible ways to build rather than buy. All figures general — confirm current.

Frequently asked questions

Does an FHA construction loan really close only once? Yes. HUD defines it as a construction-to-permanent loan “using a single mortgage closing prior to the start of construction.” You sign one set of documents before building; the same loan converts to your permanent FHA mortgage after the final inspection or certificate of occupancy, with no second closing and no re-qualifying.

How much do I need to put down on an FHA construction loan? The minimum is 3.5% of the Adjusted Value with a 580+ credit score. Adjusted Value is the lesser of the finished-home appraised value or your documented Acquisition Cost, so your 3.5% is calculated against whichever is lower. Scores of 500–579 require 10% down. Figures general — confirm current.

Can I be my own general contractor? Only if you are a licensed general contractor. HUD requires that you contract with a licensed general contractor to build the home, and it permits you to act as your own GC solely when you personally hold that license. Otherwise you must hire a licensed builder.

What happens to my interest rate while the home is being built? The rate may float during construction within a documented range, but the agreement must set a maximum rate the permanent mortgage cannot exceed, and the lender must qualify you at that maximum. If rates fall and you have not locked, you may lock at the lower rate.

When do I start making mortgage payments? Amortization of the permanent mortgage begins no later than the first of the month following 60 days from the final inspection or the issuance of the certificate of occupancy. During construction, funds release from escrow as work progresses, each draw requiring your written authorization.

Is the FHA loan limit high enough to build in Colorado Springs? For most buyers, yes. The 2026 FHA one-unit floor is $541,287, and El Paso County is at that floor. With local median prices in the mid-$400,000s, a typical Colorado Springs build fits under the cap. Confirm your specific project’s numbers with a broker — general, confirm current.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. All rates, fees, limits, and program figures are general and subject to change — confirm current details with a licensed loan officer. This article is educational and is not a commitment to lend or an offer of credit; approval and terms depend on underwriting. Last updated: July 2026.

How construction loan money is released: draws, inspections, written borrower approval, interest reserves, and contingency reserves — with FHA, VA, USDA, and conventional rules explained.

How conventional construction-to-permanent loans work under Fannie Mae (Selling Guide B5-3.1) and Freddie Mac (Guide 4602), with 2026 rule changes, for Colorado Springs builders.

USDA single-close construction loans let you build a rural Colorado home with $0 down and one closing. See the guarantee timing, builder rules, reserves, and El Paso County eligibility.