A conventional construction loan is a construction-to-permanent mortgage backed by Fannie Mae or Freddie Mac that finances the build and then converts to a standard 15- or 30-year mortgage — with no FHA, VA, or USDA insurance behind it. Fannie Mae and Freddie Mac each publish their own construction rules, and while the two programs rhyme, they differ in the details that decide whether your file closes cleanly: what the loan can be used for, how long the build can run, how old your paperwork can get, and whether cash-out is even on the table. This guide walks through both agencies’ current requirements as written in their canonical guides, and flags the 2026 changes that reshaped the Freddie side.

If you are building in El Paso County — a new home on acreage in Black Forest, an infill lot in Old Colorado City, or a first house near Fort Carson — the conventional route is often the cleanest path for borrowers with solid credit and a standard down payment. For a wider view of every program, start with our overview of construction loans in Colorado and the side-by-side comparison of FHA, VA, USDA, and conventional construction loans.

What a conventional construction loan is (and is not)

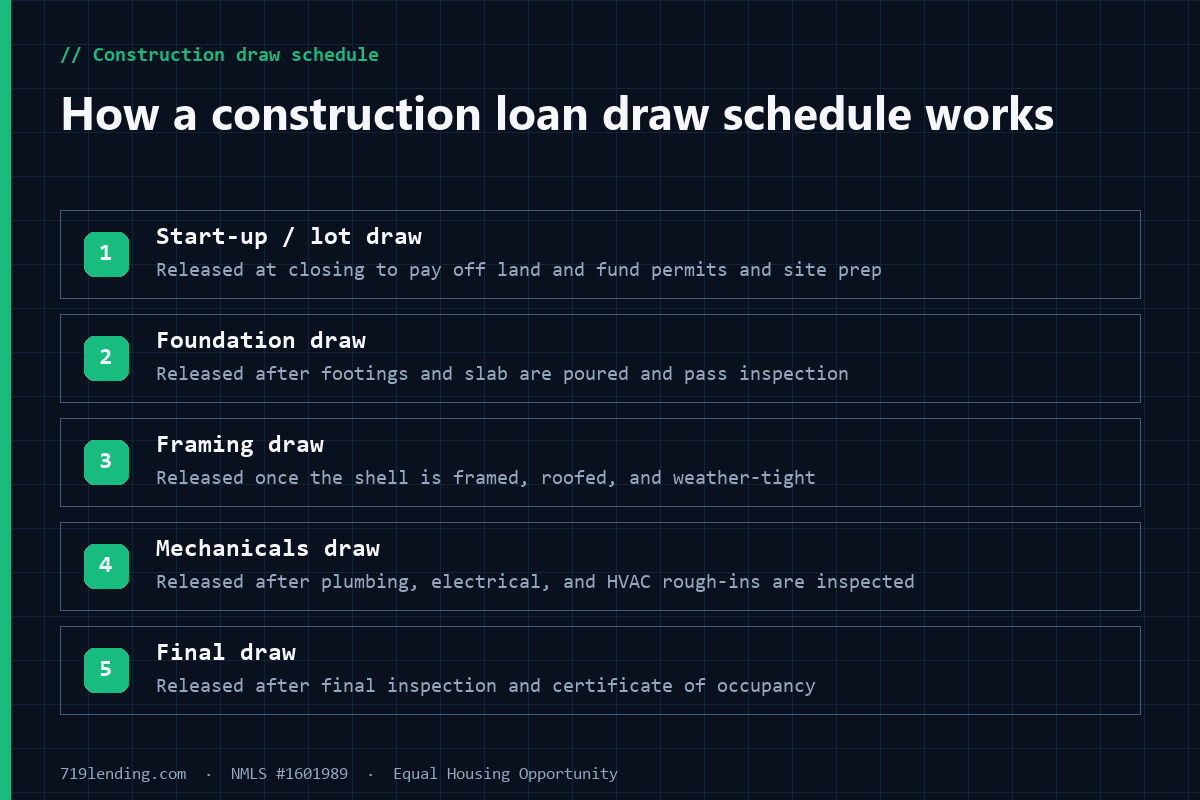

“Conventional” simply means the loan conforms to Fannie Mae or Freddie Mac guidelines and is not insured or guaranteed by a government agency. A conventional construction-to-permanent loan bundles the construction phase and the eventual permanent mortgage into one financing arrangement. During construction, the lender advances funds in stages (draws) as the home is built; once the certificate of occupancy is issued and the build is complete, the loan converts to permanent financing.

Two structures exist, and the naming differs by agency:

Single-closing (Fannie) / One-Time Close (Freddie) — one closing covers both the construction period and the permanent loan. You sign once, up front.

Two-closing (Fannie) / Two-Time Close (Freddie) — the interim construction loan closes first, then a second, separate closing puts the permanent mortgage in place.

The trade-off is familiar to anyone who has read our explainer on one-time close versus two-time close construction loans: a single closing means one set of costs and a locked structure, while two closings add a second round of underwriting and fees but more flexibility if the build runs long or plans change.

The details borrowers most often miss on Fannie Mae and Freddie Mac construction files.

Fannie Mae single-closing construction rules (Selling Guide B5-3.1)

Fannie Mae treats the construction phase of a single-closing loan as atemporary loan that is exempt from the ability-to-repay rules under Regulation Z, and requires the lender to underwrite the file based on the terms of the permanent financing. The rules that most often catch borrowers off guard:

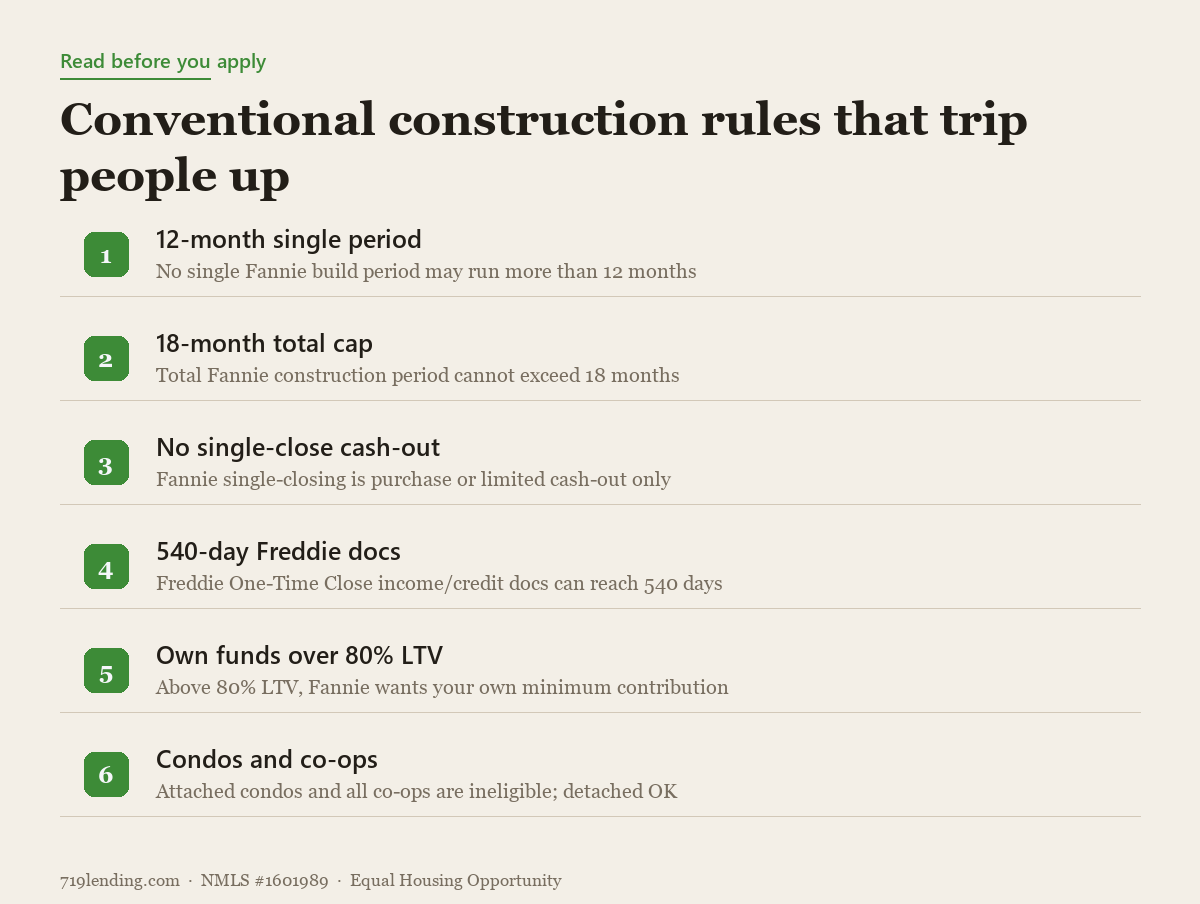

Time limits. No single construction period may run more than 12 months, and the total construction period may not exceed 18 months. If the build blows past those limits, Fannie requires the lender to process it as a two-closing transaction instead.

Allowed purposes. A single-closing loan can only be a purchase or a limited cash-out refinance. Cash-out refinances are not eligible in a single-closing construction-to-permanent loan.

How LTV is measured. On a purchase, the loan-to-value ratio uses the loan amount divided by the lesser of the “as completed” appraised value or the purchase price (the cost of construction plus the sales price of the lot). On a limited cash-out refinance, LTV is based on the “as completed” appraised value.

Document age. Credit and appraisal documents must be no more than four months old at the note date. At conversion to permanent financing they can be more than four but no more than 18 months old, but only if the loan was run through Desktop Underwriter with an Approve/Eligible recommendation and the LTV, CLTV, and HCLTV ratios are all 95% or less.

Your own money. The borrower must contribute the minimum down payment from their own funds unless the LTV is 80% or less (or the transaction otherwise qualifies for gift, grant, or employer-assistance funds on a one-unit principal residence).

Property eligibility matters here. Attached units in a condo project and all co-op properties are ineligible for conventional construction-to-permanent financing. Detached condos and manufactured homes can qualify, subject to the applicable project-review and property requirements. Because we build custom infographics from these figures, the numbers above also appear in the charts on this page so the prose and the visuals always agree.

Freddie Mac construction rules and the 2026 changes (Guide 4602)

Freddie Mac restructured its construction offering for loans with application received dates on or after February 4, 2026, renaming the product line from “Construction Conversion Mortgages” to “Construction to Permanent Mortgages” and changing how the two-close version is delivered. The key points under Guide Section 4602:

Two-Time Close is now a refinance. For applications on or after February 4, 2026, all Two-Time Close construction-to-permanent mortgages are consideredrefinance mortgages — either “no cash-out” or cash-out — regardless of whether the borrower owned the land before the interim construction financing closed. It cannot be delivered as a purchase.

One-Time Close document-age flexibility. For certain One-Time Close transactions, Freddie now permits income, employment, and credit report documentation up to 540 calendar days before the Effective Date of Permanent Financing — far longer than the usual limits — recognizing that a build takes time. Asset documentation must be dated no more than 120 days before the note date of the interim construction financing, and the appraisal effective date must be no more than four months before the interim closing (with an appraisal update required if it is more than 120 days before the permanent effective date). Confirm the current qualifying criteria on your specific file.

What counts as cash-out. Paying off unsecured liens or construction costs the borrower paid outside the secured interim construction financing is treated as cash-out to the borrower if it exceeds the greater of $2,000 or 1% of the loan amount.

Six months on title for cash-out. For a cash-out structure, at least one borrower must have been on title to the land for six months or more before the Effective Date of Permanent Financing. Freddie removed the six-month minimum only where a borrower inherited or was legally awarded the land.

Our take: the February 2026 Freddie changes are borrower-friendly. Treating Two-Time Close as a refinance simplifies delivery, and the 540-day document window is a real relief on custom builds that stretch past a year — a scenario we see often on acreage builds east of Colorado Springs where site work and weather add months.

How the two agencies differ on the details that decide whether your file closes cleanly.

Fannie versus Freddie: the differences that actually matter

Both agencies get you to the same place — a completed home on a permanent conventional mortgage — but the paths diverge on document age, how the two-close version is treated, and terminology. The comparison chart on this page lays the two side by side. In practice, the most consequential differences are:

Document-age generosity. Fannie allows up to 18 months on credit and appraisal documents at conversion (with DU Approve/Eligible and LTV of 95% or less); Freddie’s 2026 rules stretch income, employment, and credit documentation to 540 days (about 18 months) on qualifying One-Time Close files. Both acknowledge that construction takes time — but they measure and condition it differently.

Two-close treatment. Fannie’s two-closing transaction can be a purchase or a refinance; Freddie’s Two-Time Close is now always a refinance for 2026 applications. That changes fee disclosures and seasoning math.

Naming. “Single-closing” and “two-closing” (Fannie) versus “One-Time Close” and “Two-Time Close” (Freddie) describe the same two structures. Do not let a lender’s shorthand confuse which agency’s rulebook governs your file.

Rate and cost differences between the two are driven more by the individual lender and the day’s market than by the agency itself — see our page on construction loan rates for how pricing is built, and how construction loan draws work for the mechanics of the build phase common to both.

Is a conventional construction loan right for your Colorado Springs build?

Conventional construction financing tends to fit borrowers who have strong credit, a documented down payment, and a standard build on an eligible property type. If you are putting less down or your profile is closer to the margins, a government program may reach further — compare the FHA construction loan and, for eligible service members and veterans stationed at or retired near Fort Carson and Peterson, the VA construction loan in Colorado Springs. Rural parcels in El Paso and Teller Counties may qualify for a USDA construction loan.

A few practical checks before you commit to the conventional route:

Confirm your property type is eligible — remember attached condos and all co-ops are out on the conventional side.

Map your build timeline against the 12-month single-period and 18-month total limits (Fannie) so you do not accidentally force a two-close conversion.

Decide early between single/one-time close and two/two-time close, because it drives your closing costs and how many rounds of underwriting you face.

Line up your down payment from eligible sources, since above 80% LTV Fannie wants your own funds for the minimum contribution.

Because the agency rulebooks shift — Freddie’s own construction rules changed materially in February 2026 — the smartest move is to have a broker who reads the guides and shops both agencies plus the government programs for your file. That is exactly what we do as a mortgage broker in Colorado Springs.

Frequently asked questions

Is a conventional construction loan the same as an FHA or VA construction loan? No. Conventional construction loans follow Fannie Mae or Freddie Mac guidelines and carry no government insurance or guarantee. FHA, VA, and USDA construction loans are backed by their respective agencies and have their own down-payment, eligibility, and mortgage-insurance rules. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency.

Can I take cash out with a conventional construction loan? Not on a Fannie Mae single-closing loan — those are limited to purchase or limited cash-out refinance. Freddie Mac allows cash-out on qualifying construction-to-permanent transactions, where paying off unsecured liens or out-of-pocket construction costs above the greater of $2,000 or 1% of the loan amount counts as cash-out, and at least one borrower generally must have been on title six months or more.

How long can the construction phase last? On a Fannie Mae single-closing loan, no single construction period may exceed 12 months and the total may not exceed 18 months; go longer and it must be processed as a two-closing transaction. Freddie’s One-Time Close rules allow qualifying income, employment, and credit documentation up to 540 days old at the permanent effective date, which accommodates longer builds.

What down payment do I need for a conventional construction loan? It depends on the loan-to-value ratio and program, and figures are general — confirm current. On Fannie Mae files, if your LTV is above 80% you generally must contribute the minimum down payment from your own funds rather than relying entirely on gifts, unless the transaction qualifies for gift, grant, or employer assistance on a one-unit principal residence.

Are condos and manufactured homes eligible? Attached condo units and all co-op properties are ineligible for conventional construction-to-permanent financing. Detached condos and manufactured homes can be eligible, subject to the applicable project-review and property requirements.

Did the rules for these loans change recently? Yes. Freddie Mac’s updates for applications received on or after February 4, 2026 renamed the product to “Construction to Permanent Mortgages,” made all Two-Time Close transactions refinance mortgages, and introduced the 540-day document-age allowance for certain One-Time Close loans. Always confirm the current guide before you apply.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. Figures and program rules are general — confirm current. Last updated: July 2026.

How construction loan money is released: draws, inspections, written borrower approval, interest reserves, and contingency reserves — with FHA, VA, USDA, and conventional rules explained.

USDA single-close construction loans let you build a rural Colorado home with $0 down and one closing. See the guarantee timing, builder rules, reserves, and El Paso County eligibility.

How VA construction loans let eligible Colorado Springs veterans build a home with $0 down and no monthly mortgage insurance. One-time close vs two-time close, draws, funding fee, and the 2025 builder-ID change explained.