A VA construction loan lets an eligible veteran or service member in Colorado Springs build a primary residence with $0 down and no monthly mortgage insurance, financing the land and the construction inside one VA-guaranteed loan. The U.S. Department of Veterans Affairs guarantees the financing; a private lender funds it, closes it before ground is broken, and pays the builder in draws as the home goes up. Because it is structured as a purchase, the same signature VA benefits apply to a new build that apply to buying an existing home — no down payment as long as the price does not exceed the appraised value, and no private mortgage insurance (PMI) or mortgage insurance premium (MIP). Below we walk through exactly how these loans work, what changed at the VA in 2025, and what it means for building near Fort Carson, Peterson, or Schriever.

What a VA construction loan is and how it works

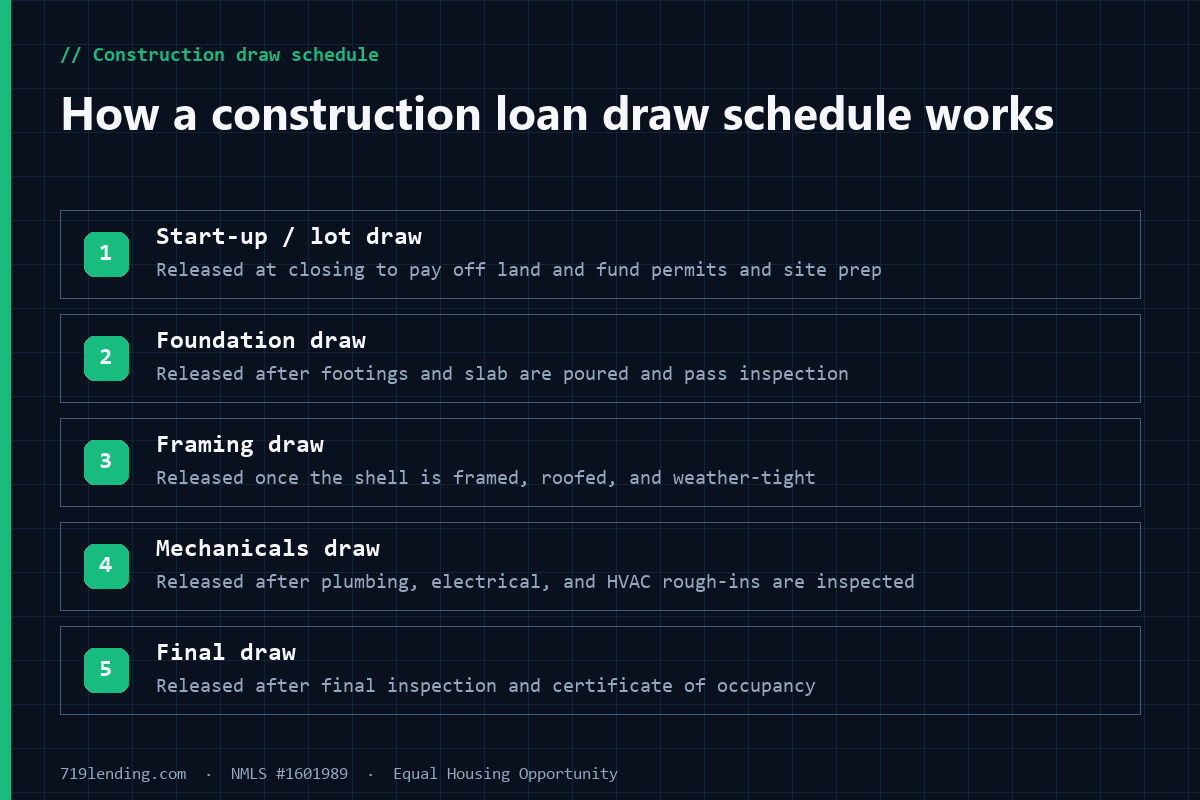

The VA calls this product a “construction/permanent home loan” — a single loan that finances the construction and purchase of a residence. Per the VA Lender’s Handbook (Pamphlet 26-7), the loan is closed before construction begins. At closing, proceeds cover the cost of the land (or pay off the balance owed on land the veteran already holds), and the remaining money goes into an escrow account. The lender then releases that escrow to the builder in draws as work is completed. A key protection: the lender must obtain the borrower’s written approval before each draw is paid to the builder.

Two structures exist, and the choice is permanent. A one-time close (the VA’s “one closing vehicle”) wraps construction and the permanent mortgage into a single closing before construction starts. A two-time close (the VA’s “two part closing vehicle”) closes the permanent financing after the Notice of Value conditions are met. The Handbook is explicit that once a loan vehicle is established, it cannot be modified into a different vehicle — so a one-time close cannot later be converted into a two-time close. We cover that trade-off in depth in our guide to one-time close vs two-time close construction loans.

One point that surprises many buyers: even a veteran who already owns the lot is treated as making a purchase in VA systems, not a refinance. The land balance is simply paid from the loan proceeds at closing.

VA-backed purchase-loan benefits carry into a construction/permanent loan. General, confirm current.

The veteran’s advantages: $0 down and no monthly mortgage insurance

The reason a VA build is worth the extra coordination is the benefit set. On a VA-backed purchase loan, VA.gov states there is “no down payment as long as the sales price isn’t higher than the home’s appraised value” and “no need for private mortgage insurance (PMI) or mortgage insurance premiums (MIP).” VA.gov also notes that nearly 90% of all VA-backed home loans are made without a down payment. Those advantages carry straight into a construction/permanent loan:

$0 down. Eligible veterans can finance up to 100% of the appraised value, so you are not tying up cash you would rather keep as a reserve during a build.

No monthly mortgage insurance. FHA and low-down conventional construction loans carry monthly mortgage insurance; VA does not, because the VA guaranty (up to 25% of the loan) stands in for it.

Competitive interest rates. The VA notes lenders offer competitive rates on VA-backed loans; the permanent rate is set at closing, and some lenders offer a “ceiling-floor” float where you lock no higher than a stated maximum and can capture a lower rate if the market moves.

Payments postponed until the home is done. You do not make a full principal payment on an unfinished house — more on that below.

Reusable entitlement. Once the loan is paid off or entitlement is restored, the benefit can be used again.

These figures are general — confirm current with a licensed lender for your scenario.

Typical VA one-time-close sequence per the VA Lender’s Handbook. General, confirm current.

How a VA one-time-close construction loan works, step by step

A one-time close moves in a predictable sequence. For a family relocating to the 4th Infantry Division at Fort Carson or a growing household in Falcon or Monument, understanding the order helps you plan the build timeline realistically:

Establish eligibility. Obtain your Certificate of Eligibility (COE) through your lender, VA.gov, or by mail, and get underwritten for the permanent loan at the maximum rate.

Lock in the builder, plans, and appraisal. The lender orders the appraisal for the proposed construction; the resulting Notice of Value sets the reasonable value the loan is measured against.

Close before construction. The loan closes prior to breaking ground. Land is paid off from proceeds and the construction budget is placed into escrow.

Draws during construction. The lender releases escrow to the builder in stages — but only after you give written approval for each draw.

Builder carries the construction period. The builder pays construction-period interest and the fees an interim construction lender would normally charge (see the next section).

Completion and final inspection report. The loan is not guaranteed until construction is 100% complete and all Notice of Value conditions are met; the lender obtains a clear final inspection/compliance report.

Guaranty and first payment. The Loan Guaranty Certificate is issued after the clear final report; your amortized payments begin once the home is complete.

Who pays what during construction

The VA draws a firm line between builder costs and veteran costs, which protects the veteran’s cash during the build. Under the Lender’s Handbook, on a construction/permanent home loan the builder is responsible for interest payments during the construction period and all fees normally paid by a builder who obtains an interim construction loan, including but not limited to:

Inspection fees

Title update fees

Hazard insurance during construction

Property taxes accruing during construction and similar carrying costs

Just as important, the Handbook states the veteran may not pay any fees that are the builder’s responsibility. The fees a veteran can pay are the ordinary allowable VA loan fees described in the Handbook’s fee chapter. Practically, this means the construction-period carrying costs sit with the builder, not with you.

Payments are postponed until the home is finished

A VA construction/permanent borrower begins making payments only after construction is complete. To make that work, the VA allows the initial payment on principal to be postponed for up to one year if necessary, while the loan is still amortized to achieve full repayment within its remaining term. The Handbook’s own example: if construction takes six months, a 30-year mortgage must be scheduled to fully repay in 29 years and 6 months. Rather than a balloon at the end, lenders typically set slightly larger equal payments that retire the loan within the original maturity. This is a meaningful cash-flow advantage over a stand-alone construction loan that demands interest payments on a house you cannot yet live in.

The funding fee — and who is exempt

VA loans carry no monthly mortgage insurance, but most borrowers pay a one-time VA funding fee that helps sustain the program. On a construction/permanent loan the Handbook specifies the funding fee is due at loan closing (prior to the start of construction) and must be paid to VA within 15 days of loan closing — it is not tied to when construction finishes. Per VA.gov, purchase-loan funding fee rates are:

Down payment

First-time use

Subsequent use

Less than 5% (including $0 down)

2.15%

3.3%

5% to 9.99%

1.5%

1.5%

10% or more

1.25%

1.25%

The fee can be paid in cash at closing or financed into the loan. Crucially, many Colorado Springs veterans owe no funding fee at all. Per VA.gov, you are exempt if you receive VA disability compensation, are eligible for it but receive retirement or active-duty pay instead, receive Dependency and Indemnity Compensation as a surviving spouse, or received a Purple Heart (with evidence by loan closing). These percentages are general — confirm current before you build.

The 2025 builder rule change every Colorado Springs buyer should know

Here is where recent information matters: as of March 31, 2025, the VA no longer requires a builder identification number (BIN). Under VA Circular 26-25-1, VA rescinded the requirement for builders to obtain a VA-issued builder ID before a Notice of Value is issued, noting that references to builder identification numbers will be removed from Chapters 7, 10, and 13 of the Lender’s Handbook in a future revision. If you read older articles insisting your builder must first get a “VA Builder ID,” that guidance is now outdated for standard VA-guaranteed construction loans.

A few consequences follow from that circular:

Builders still must be licensed. They are expected to meet all state and local licensing requirements — Colorado contractor licensing and El Paso County / City of Colorado Springs building codes still apply and still protect you.

VA no longer does its own construction inspections. The circular confirms VA ceased compliance inspections for new and proposed construction back in February 2006, relying instead on local building inspections and 1- or 10-year construction warranties.

Complaints route locally. Rather than interceding with builders, VA now directs veterans to local building departments, licensing boards, or legal counsel for construction disputes.

Two exceptions remain. A builder ID is still required for a Specially Adapted Housing (SAH) grant and for the Native American Direct Loan (NADL) program.

Our take: the BIN change is a net positive — it removes a paperwork bottleneck that used to delay closings — but it also means the VA is not a construction watchdog. Choose a licensed, established Colorado Springs builder and lean on a strong construction contract and local inspections. That has always been the real protection; now it is the primary one.

Building near Fort Carson, Peterson, and Schriever

Colorado Springs is one of the strongest VA-loan markets in the country because of the density of active-duty, Guard, Reserve, and retired service members tied to Fort Carson, Peterson Space Force Base, Schriever Space Force Base, and the Air Force Academy. New-construction corridors east and south of the city — Falcon, Peyton, Fountain, Widefield, and the Banning Lewis Ranch area — put buyers within reasonable commutes of the installations. A VA construction loan is a natural fit when existing inventory near a duty station is tight and a veteran would rather build to fit their family than compete for a resale.

Because Colorado has active seasons for weather delays, build the postponed-payment window and a realistic completion timeline into your planning, and confirm your builder is comfortable carrying construction-period interest and fees as the VA requires. If a full ground-up build is more than you need, compare it against a renovation-style option in our breakdown of a construction loan vs a HELOC vs a renovation loan, and see the broader landscape in our construction loans in Colorado pillar guide and our side-by-side of FHA, VA, USDA, and conventional construction loans compared.

Is a VA construction loan right for you?

For an eligible borrower, the math is compelling: no down payment, no monthly mortgage insurance, postponed payments until move-in, and construction-period carrying costs shifted to the builder. The trade-offs are that fewer lenders originate one-time-close VA construction loans, the process requires more coordination than a resale purchase, and your build must satisfy VA appraisal and completion standards plus local inspections. If you already have a VA benefit and a lot (or a builder) in mind, it is worth a conversation. As your local mortgage broker in Colorado Springs, we can confirm your entitlement, funding-fee status, and whether a one-time or two-time close fits your build. You can also review your broader financing options on our VA loans in Colorado Springs page.

Frequently asked questions

Do I really need $0 down to build with a VA construction loan? Per VA.gov, a VA-backed purchase loan requires no down payment as long as the sales price is not higher than the home’s appraised value, and this carries into a construction/permanent loan. A larger down payment is optional and lowers your funding fee tier. Figures are general — confirm current.

Can I convert a one-time close into a two-time close later? No. The VA Lender’s Handbook states that once a loan vehicle is established it cannot be modified into a different loan vehicle, so a one-time close cannot be converted to a two-time close after it is set up.

Does my builder still need a VA Builder ID in 2026? Not for a standard VA-guaranteed construction loan. VA Circular 26-25-1 (effective March 31, 2025) rescinded the builder-ID requirement for issuing the Notice of Value or processing the loan. Builders must still meet state and local licensing. A builder ID is still required for SAH grants and NADL loans.

Who pays the interest and fees while my Colorado Springs home is being built? The builder. Under the Handbook, on a construction/permanent loan the builder is responsible for construction-period interest plus fees such as inspection fees, title update fees, and hazard insurance during construction, and the veteran may not pay fees that are the builder’s responsibility.

When do my payments start? After construction is complete. The VA allows the initial principal payment to be postponed up to one year if needed, while the loan is amortized to fully repay within its remaining term.

Am I exempt from the VA funding fee? You may be. Per VA.gov, veterans who receive VA disability compensation (or are eligible but take retirement/active-duty pay), surviving spouses receiving Dependency and Indemnity Compensation, and Purple Heart recipients are exempt. The fee is otherwise due within 15 days of loan closing and can be financed. Confirm your status with a lender.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. All rates, fees, and figures are general — confirm current with a licensed loan originator; they are not an offer or guarantee of any particular loan, rate, or approval. Last updated: July 2026.

How construction loan money is released: draws, inspections, written borrower approval, interest reserves, and contingency reserves — with FHA, VA, USDA, and conventional rules explained.

How conventional construction-to-permanent loans work under Fannie Mae (Selling Guide B5-3.1) and Freddie Mac (Guide 4602), with 2026 rule changes, for Colorado Springs builders.

USDA single-close construction loans let you build a rural Colorado home with $0 down and one closing. See the guarantee timing, builder rules, reserves, and El Paso County eligibility.