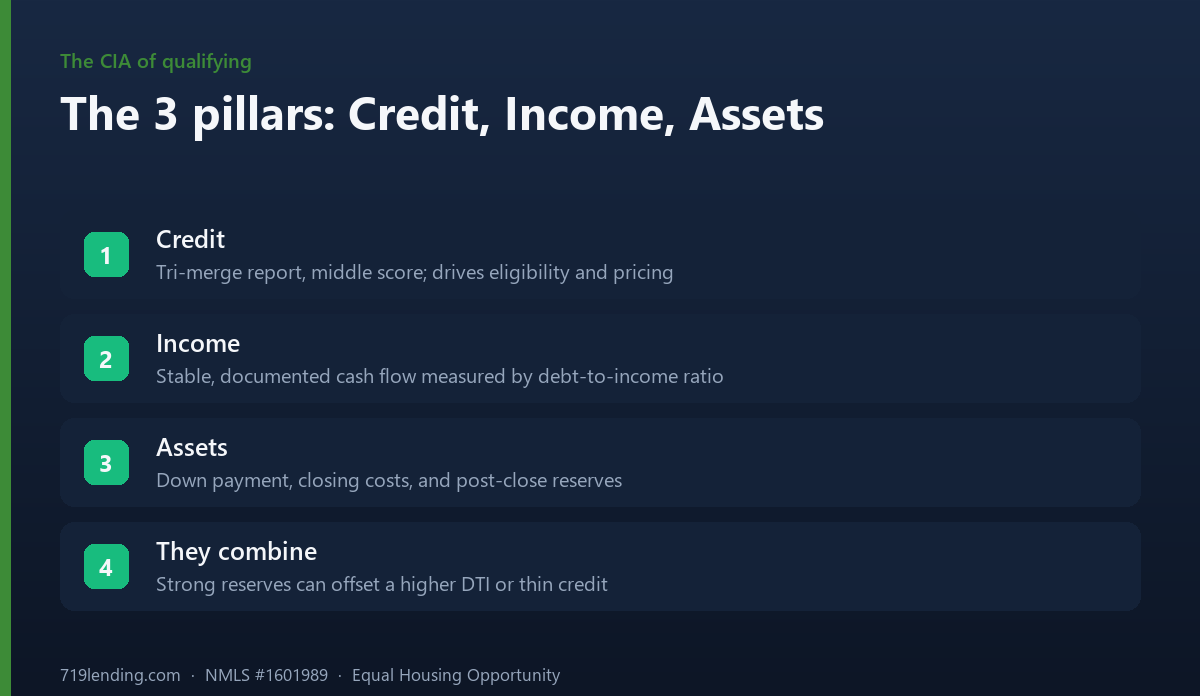

Credit, income, and assets are the three pillars every mortgage lender checks. Here is what each one means, why it matters, and how to strengthen it before you apply in Colorado Springs.

Beyond Your Credit Score: The Four C’s of Mortgage Approval

Mortgage approval rests on four factors underwriters call the Four C’s — Credit, Capacity, Capital, and Collateral — not on your credit score alone. A strong score helps, but it is only one piece of the file. Lenders underwrite the whole borrower: how you have handled debt, whether your income comfortably covers the payment, what savings you have behind you, and whether the home itself is worth what you are paying. Understand how these four pieces interact and you will understand why a 780 score can still get declined, and why a 640 score can still close.

Below, we walk through each C, root each one in a primary source, and explain how a Colorado Springs mortgage broker reads them together. Figures and thresholds below are general — confirm current numbers for your situation.

What are the Four C’s of mortgage approval?

The Four C’s are the classic underwriting framework lenders use to answer one question: how likely are you to repay this loan, and is it well secured? Each C examines a different part of your financial picture.

- Credit — how you have managed debt and payments in the past.

- Capacity — whether your income comfortably supports the new payment plus your other obligations.

- Capital — the cash and assets you bring to closing and hold in reserve afterward.

- Collateral — the property itself, and whether an appraisal supports the loan amount.

No single C carries the file. Underwriting is a weighing exercise: a weakness in one area can often be offset by strength in another. That is the whole point of looking beyond the score.

Credit: your track record with debt

Credit is the C most borrowers fixate on, and it is genuinely important — but it measures history, not your bank balance. Your FICO Score is built from five categories with published weights. According to myFICO, the model is: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

Two categories do most of the work. Payment history at 35% is the single largest factor — lenders want to see that you pay accounts on time. Amounts owed at 30% looks heavily at your credit utilization, the share of available revolving credit you are actually using. Running your cards near their limits drags the score even if you never miss a payment.

What credit does not tell a lender is whether you can afford the home. A pristine 780 built on thin income still has to clear the other three C’s. Conversely, a lower score is not automatically a decline — many loan programs approve well below the numbers borrowers assume, and a strong down payment or healthy reserves can compensate. To see how income and debts translate into a realistic price range, run the numbers with our Colorado Springs affordability tools before you shop.

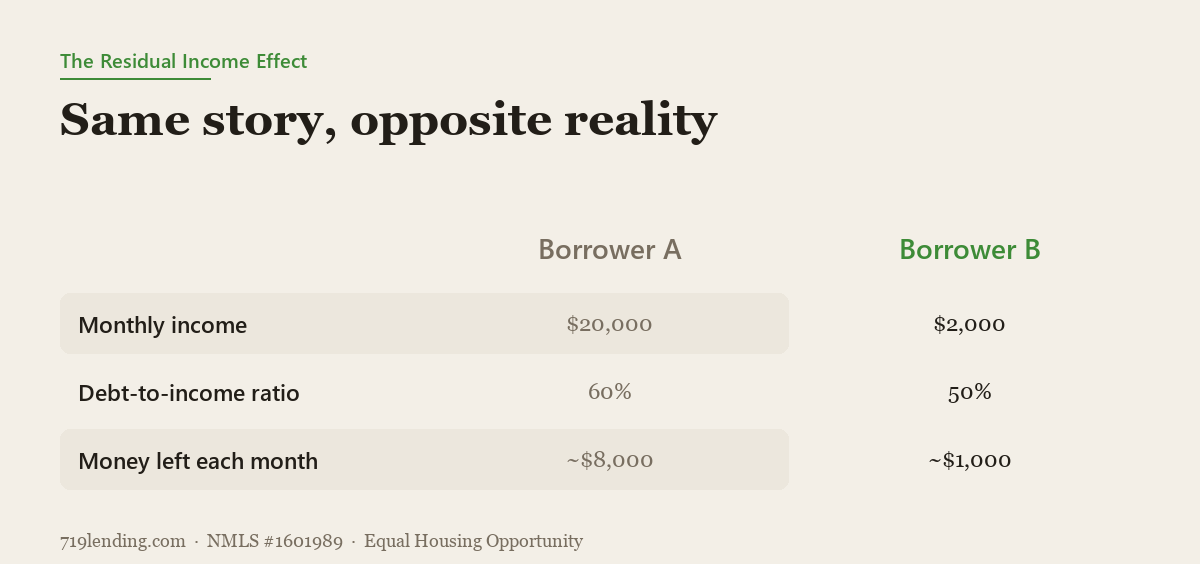

Capacity: can your income carry the payment?

Capacity is the “can you actually pay this every month?” C, and federal rules make it mandatory. Under the Consumer Financial Protection Bureau’s Ability-to-Repay rule, a lender generally may not originate a mortgage without making a reasonable, good-faith determination that you can repay it. The CFPB requires lenders to consider and document your income, assets, employment, credit history, and monthly expenses before approving the loan.

The core metric here is your debt-to-income ratio (DTI) — your total monthly debt payments divided by your gross monthly income. Underwriters look at both a “front-end” ratio (housing payment alone) and a “back-end” ratio (housing plus car loans, student loans, credit-card minimums, and other obligations). The Ability-to-Repay framework historically tied one path to a back-end DTI of 43% or less; the CFPB has since replaced that hard threshold in the qualified-mortgage rules with a price-based approach, but DTI remains central to how every lender evaluates capacity.

Colorado Springs buyers feel capacity acutely. When El Paso County home prices and rates push the monthly payment up, DTI is usually the constraint that decides how much home you qualify for — not your score. If you want to pressure-test this before you shop, our affordability tools model exactly how income and debts translate into a price range.

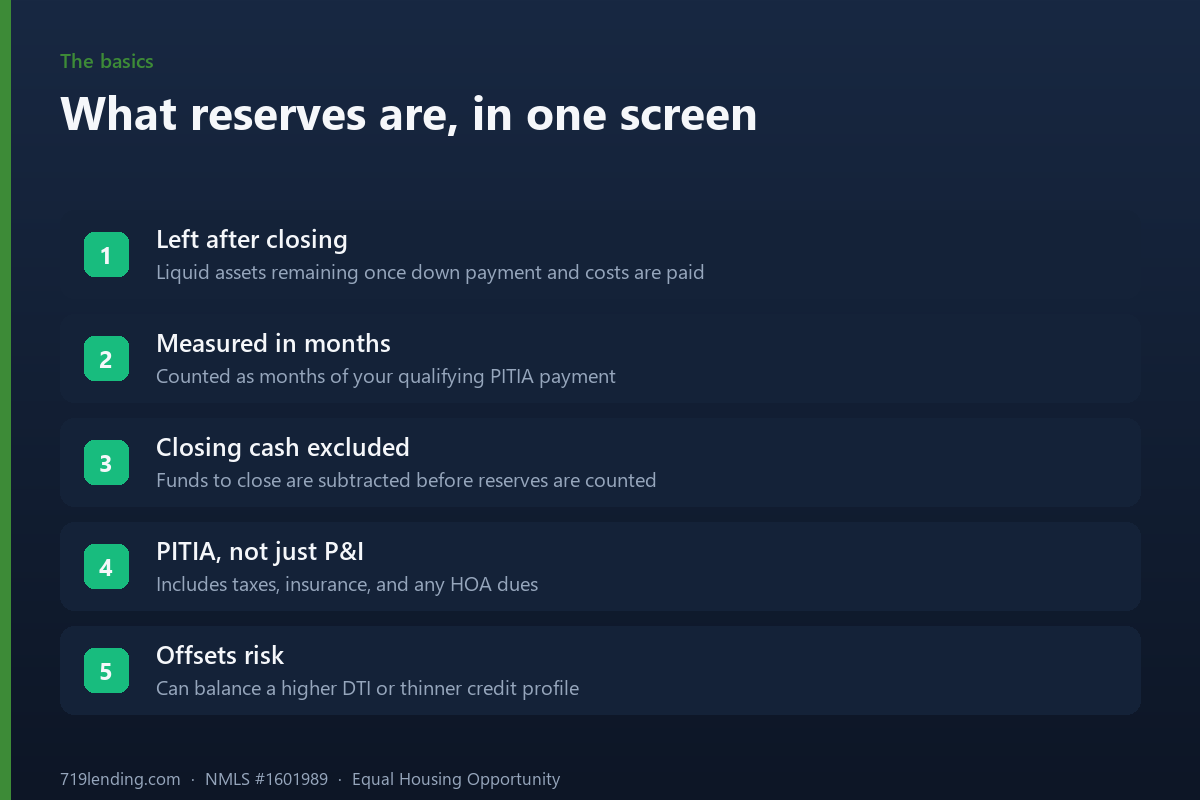

Capital: your down payment and reserves

Capital is the cash behind the deal — both what you put down and what remains after closing. The down payment reduces the loan amount and signals commitment. But underwriters look past closing day to your reserves: liquid savings you could tap to keep paying the mortgage if income hiccups.

Fannie Mae’s Selling Guide defines reserves precisely. In section B3-4.1-01, reserves are “liquid financial reserves” — assets available to a borrower after the mortgage closes — measured by the number of months of the qualifying payment (PITIA — principal, interest, taxes, insurance, and any HOA dues) that a borrower could cover with those assets. Crucially, the funds you need to close are subtracted first; only what is left over counts as reserves.

How many months you need depends on the loan and property. Fannie Mae sets no minimum reserve requirement for many one-unit primary residences, while second homes and investment properties carry higher requirements. Reserves also act as a compensating factor: a borrower with a middling score or a higher DTI who shows several months of PITIA in the bank presents a materially lower risk. If you are weighing how much to put down versus how much to keep liquid, our affordability tools let you test how reserves and down payment trade off against your monthly payment.

Our take: reserves are the most under-appreciated C. Borrowers pour everything into the down payment, then arrive at closing with nothing behind them. A slightly smaller down payment that leaves a cushion in the bank often makes for a stronger file than an all-in payment that empties the account.

Collateral: the property and the appraisal

Collateral is the C that is not about you at all — it is about the house. A mortgage is a secured loan: the property backs the debt, and if the borrower defaults, the lender can foreclose and sell it. That is why the lender cares deeply what the home is actually worth.

The tool that answers that question is the appraisal. The CFPB describes an appraisal as “a written document that shows an opinion of how much a property is worth,” prepared as an independent assessment of value. Lenders order it to confirm the collateral supports the loan.

The number that matters is the lesser of the purchase price or the appraised value. If a Colorado Springs home appraises below the agreed price, the lender bases the loan on the lower figure — and the buyer must cover the gap, renegotiate, or walk. Collateral can quietly sink an otherwise strong file: perfect credit, ample income, and healthy reserves do not matter if the appraisal comes in short and there is no plan to bridge it.

How the Four C’s work together

The reason the score alone never approves a loan is that underwriters read the four C’s as a system, not a checklist. A weakness in one C can be offset by strength in another — that is the essence of manual underwriting, where an underwriter weighs compensating factors rather than reading a single number.

Consider how the offsets actually work:

- Lower credit, strong capital. A 640 score paired with a large down payment and several months of reserves can clear where a thin file would not.

- Higher DTI, strong reserves. A stretched capacity ratio is easier for an underwriter to accept when the borrower shows months of PITIA saved.

- Strong credit and income, weak collateral. Even a flawless borrower stalls if the appraisal does not support the price — a reminder that collateral is independent of the other three.

This is why two borrowers with identical scores can get different answers, and why chasing a few more score points is often the wrong focus. The file wins or loses on the balance of all four C’s.

Strengthening each C before you apply

Because the C’s interact, the smartest preparation strengthens the whole file rather than one number. Here is where to focus.

| The C | What it measures | How to strengthen it |

|---|---|---|

| Credit | Payment history and utilization | Pay on time; lower revolving balances before applying |

| Capacity | Income vs. debt (DTI) | Pay down or pay off installment debts; avoid new financing |

| Capital | Down payment and reserves | Build savings; document and season funds; keep a cushion |

| Collateral | Property value via appraisal | Choose realistic offer prices; plan for an appraisal gap |

First-time buyers in Colorado have extra levers on the Capital side — down payment assistance and first-time buyer programs can shore up that C without draining reserves. And because the four C’s trade off against each other in ways that are hard to see from the outside, the highest-value move is having a broker read your full file early, before you fall in love with a house.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by any government agency, including FHA, VA, USDA, or CHFA. Figures, thresholds, and program requirements above are general — confirm current details for your situation. This article is educational and is not personalized financial, investment, tax, or legal advice; real estate values can rise or fall, and past performance is not a guarantee of future results. Consider consulting a licensed financial advisor. Last updated: July 2026.

Frequently asked questions

What are the Four C’s of mortgage approval? They are Credit (your debt track record), Capacity (income versus debt, measured by DTI), Capital (down payment and reserves), and Collateral (the property, confirmed by appraisal). Lenders weigh all four together rather than approving on any single factor.

Is my credit score the most important factor? It is important but not the only one. Your FICO Score is built mostly from payment history (35%) and amounts owed (30%), per myFICO — yet a strong score cannot approve a loan if your income, reserves, or appraisal fall short. Underwriters read the whole file.

Can I still get approved with a lower credit score? Often, yes. A lower score can be offset by compensating factors like a larger down payment, strong reserves, or a lower DTI. Many programs approve below the numbers borrowers assume — the other three C’s do a lot of the work.

What is DTI and why does it matter? Debt-to-income ratio is your total monthly debt payments divided by gross monthly income. The CFPB’s Ability-to-Repay rule requires lenders to document income and debts and confirm you can repay; DTI is the central measure of that capacity.

What are mortgage reserves? Reserves are liquid assets left after closing, measured in months of your PITIA payment, per Fannie Mae’s Selling Guide. They act as a safety cushion and a powerful compensating factor when another C is weaker.

What happens if the home appraises below the purchase price? The lender bases the loan on the lower of price or appraised value, so you would need to cover the difference, renegotiate, or walk away. Collateral is evaluated independently of your credit, income, and assets.

Related Posts