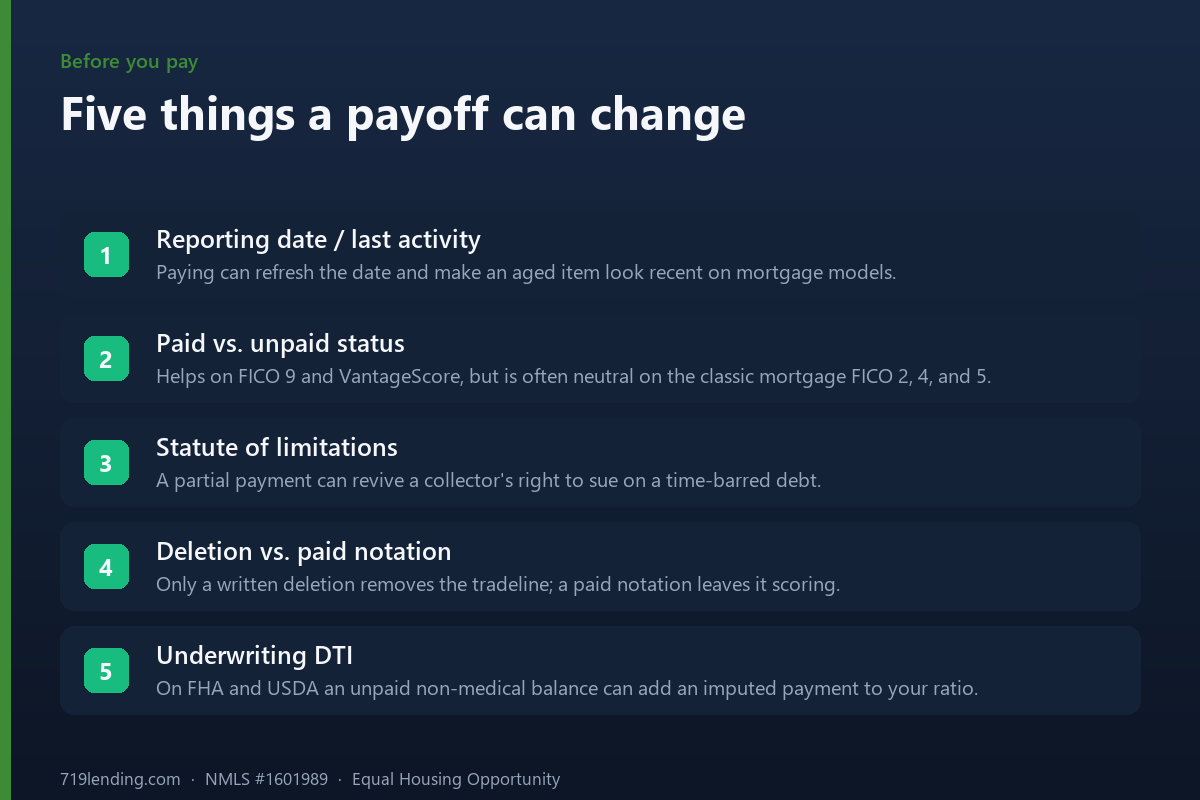

Paying off a collection before a mortgage can backfire on the older FICO models lenders actually use. Here's the last-activity trap and what underwriting really requires.

Mortgage Waiting Periods After Bankruptcy, Foreclosure, or Short Sale (2026)

The mortgage waiting period after a bankruptcy, foreclosure, or short sale runs from two to seven years, and the exact clock depends on which loan program you use and which event happened. A Chapter 13 bankruptcy can make you eligible in as little as 12 months on some programs, while a standard conventional foreclosure carries a seven-year wait. These timelines are set by the four rulebooks that govern almost every U.S. mortgage: the Fannie Mae Selling Guide (conventional), HUD Handbook 4000.1 (FHA), the VA Lender’s Handbook, and USDA Handbook HB-1-3555. This guide pulls the actual numbers from those guides and lays them out side by side.

One point matters more than any other, so we will say it up front: these are the waits to become eligible to apply, not a promise of approval. Passing the seasoning clock gets your file to the starting line. Whether you close still depends on rebuilt credit, verifiable income, and capacity to repay.

How the waiting-period clock actually works

The single most common mistake borrowers make is counting from the wrong date. The clock does not start when you filed for bankruptcy or when you first missed a payment. It starts on the date the event was legally completed. Across the programs, the trigger dates are:

- Bankruptcy — the discharge date (or, in some cases, the dismissal date), not the filing date.

- Foreclosure — the completion date, when title transfers out of your name.

- Deed-in-lieu and short sale (pre-foreclosure sale) — the date the sale or transfer was completed.

On conventional loans, Fannie Mae is explicit that the waiting period “commences on the completion, discharge, or dismissal date (as applicable) of the derogatory credit event and ends on the disbursement date of the new loan.” In plain terms: you need the seasoning satisfied by the day your new loan funds, not merely the day you apply. Because a purchase can take 30 to 45 days to close, it is worth counting your eligible date to the projected closing, not to the application date.

The mortgage seasoning matrix by loan program (2026)

Here is the core comparison. Every figure below is the standard waiting period drawn from the current program guide; extenuating-circumstance reductions are covered in the next section. Treat all figures as general and confirm current guidance for your file, because guides are updated and lenders add their own overlays.

| Event | Conventional (Fannie Mae) | FHA (HUD 4000.1) | VA | USDA |

|---|---|---|---|---|

| Chapter 7 bankruptcy | 4 years from discharge or dismissal | 2 years from discharge | 2 years from discharge | 3 years from discharge |

| Chapter 13 bankruptcy | 2 years from discharge / 4 years from dismissal | 12 months of on-time plan payments + court approval | 12 months of on-time plan payments + court approval | 12 months of on-time plan payments |

| Foreclosure | 7 years from completion | 3 years from title transfer | 2 years from completion | 3 years from completion |

| Deed-in-lieu / short sale | 4 years from completion | 3 years from title transfer | 2 years (often none if payments stayed current) | 3 years from completion |

Conventional loans: the strictest foreclosure wait

The Fannie Mae Selling Guide section B3-5.3-07 governs conventional seasoning, and it is the toughest on foreclosure. The standard periods are:

- Chapter 7 or Chapter 11 bankruptcy — 4 years from the discharge or dismissal date.

- Chapter 13 bankruptcy — 2 years from the discharge date, or 4 years from the dismissal date.

- Multiple bankruptcy filings (more than one in the past seven years) — 5 years from the most recent discharge or dismissal.

- Foreclosure — 7 years from the completion date.

- Deed-in-lieu of foreclosure, pre-foreclosure (short) sale, or mortgage charge-off — 4 years from the completion date.

Fannie Mae also addresses the case where a mortgage was included in a bankruptcy and later foreclosed. When both a bankruptcy and a foreclosure are disclosed, the lender may apply the bankruptcy waiting period if it can document that the mortgage was discharged in the bankruptcy; otherwise the greater of the two applicable waiting periods controls. That distinction can save years, so the documentation is worth chasing down.

FHA loans: two years after Chapter 7, three after foreclosure

HUD Handbook 4000.1 sets the FHA rules, and they are generally more forgiving than conventional on bankruptcy but similar on property-loss events:

- Chapter 7 bankruptcy — a minimum of 2 years from the discharge date.

- Chapter 13 bankruptcy — you may qualify after 12 months of on-time payments under the plan, with written court or trustee approval to enter a new mortgage obligation.

- Foreclosure — 3 years from the date title transferred out of your name.

- Short sale and deed-in-lieu — 3 years from the completion date. FHA can treat a short sale as carrying no waiting period if the borrower was current on all mortgage and installment debts in the 12 months before the sale, but late payments in that window trigger the full three-year wait.

VA loans: the shortest foreclosure wait, with an entitlement catch

The VA Lender’s Handbook does not impose a rigid seasoning grid the way FHA and conventional do; it directs lenders to judge whether the borrower has re-established satisfactory credit. In practice, the widely applied benchmarks are:

- Chapter 7 bankruptcy — a bankruptcy discharged more than two years ago may generally be disregarded; the standard wait is 2 years from the discharge date. A bankruptcy discharged within the last one to two years is usually not, by itself, a sufficient basis to deny the loan if the borrower has since re-established good credit.

- Chapter 13 bankruptcy — favorable consideration is possible after at least 12 months of satisfactory plan payments with trustee or court approval.

- Foreclosure — the standard VA waiting period is 2 years from the completion date, the shortest of the four programs.

- Short sale / deed-in-lieu — often treated like foreclosure at up to 2 years, but frequently no wait if payments stayed current through the sale.

There is a VA-specific wrinkle that has nothing to do with the calendar: if the home you lost was financed with a VA loan, the foreclosure ties up the entitlement on that old loan. Until that entitlement is restored or the VA is repaid, your remaining (or second-tier) entitlement limits how much you can borrow without a down payment on the next VA purchase. Seasoning and entitlement are two separate hurdles here.

USDA loans: three years, softened by the automated system

USDA Handbook HB-1-3555, Chapter 10, frames its rules around whether an event is “adverse credit” as of the application date:

- Chapter 7 bankruptcy — discharged 36 months (3 years) or more before application is generally not treated as adverse; inside that window a documented credit exception is needed.

- Chapter 13 bankruptcy — eligible after 12 months of successful plan payments, sooner with documented exceptional circumstances.

- Foreclosure, deed-in-lieu, or short sale — recorded 36 months or more before application requires no credit exception.

USDA’s automated underwriting engine (GUS) can still return an “Accept” on shorter timelines; when GUS refers a file to manual review, a written credit exception documenting the circumstances is required. That flexibility is real, but it is discretionary, not a guarantee.

Extenuating circumstances: how the clock can shrink

Every program lets a documented one-time hardship reduce the wait. This is not a hardship of your own making — a spending problem or steadily rising debt will not qualify. Guides describe events “beyond the borrower’s control,” such as a serious illness, the death of a wage earner, or an involuntary job loss from a layoff or plant closing. When granted, the reductions are meaningful:

- Conventional Chapter 7 / 11 bankruptcy — from 4 years down to 2 years.

- Conventional deed-in-lieu, short sale, or charge-off — from 4 years down to 2 years.

- Conventional foreclosure — from 7 years down to 3 years, but capped at a maximum 90% loan-to-value and limited to a principal-residence purchase or a limited cash-out refinance.

- FHA Chapter 7 bankruptcy and property-loss events — potentially down to 12 months with documented extenuating circumstances and re-established credit.

The burden is on you. Lenders require a written explanation plus third-party documentation — termination notices, medical bills, a death certificate — and evidence that the event was a one-time occurrence and that your credit has recovered since.

Our take: the extenuating-circumstance exception is real and underused, but it is not a rate quote you request — it is a case you build. In our experience the files that win it show a clean, documented paper trail connecting the hardship to the default, and a spotless payment record afterward. If your story is “money got tight,” it will not clear; if it is “my spouse died and I have a stack of records proving it,” it often will.

What to do during the seasoning window

Waiting passively is a wasted year. The point of the seasoning period, from the guides’ perspective, is to see whether you have re-established credit — so use the time to build the file the underwriter will need. The CFPB’s guidance on rebuilding credit lines up with what the mortgage guides reward:

- Pay everything on time. A single 30-day late in the seasoning window can reset expectations and, on some programs, extend the wait. Payment history is the heaviest factor.

- Open and manage new tradelines. A secured card or credit-builder loan, used lightly and paid on time, demonstrates re-established credit — exactly what VA and USDA underwriters look for.

- Keep balances low. High utilization suppresses your score right when you need it to recover.

- Clean up your reports. Dispute genuine errors early so they are resolved before you apply, and know how to read your mortgage credit report so nothing surprises you at application.

- Document the hardship now. If you intend to request an extenuating-circumstances reduction, gather the paperwork while it is easy to obtain — not two years later.

For a program-by-program view of how fast a rebuilt profile can move the needle, see our guide on how long it takes to raise your credit score to buy a house.

Eligible is not the same as approvable

Our strongest opinion in this article: treat the matrix above as the floor, not the finish line. A borrower who is technically past a two-year FHA bankruptcy wait but has a 560 score, no recent tradelines, and an unexplained collection is eligible on paper and unlikely to close in practice. The guides say so themselves — Fannie Mae pairs the waiting period with a re-established-credit requirement, and the VA and USDA make credit re-establishment the entire test. Seasoning proves time has passed. Approval proves you are a different borrower than the one who defaulted.

Frequently asked questions

Does the mortgage waiting period start from my bankruptcy filing date or my discharge date? The discharge date, not the filing date. Every major program counts the clock from when the bankruptcy was discharged (or in some conventional cases, dismissed), and for foreclosures and short sales from the completion or title-transfer date.

What is the shortest waiting period after a foreclosure? Among the major programs, the VA loan carries the shortest standard foreclosure wait at 2 years from completion. FHA and USDA are 3 years, and conventional is the longest at 7 years (reducible to 3 years with documented extenuating circumstances and a 90% loan-to-value cap).

Can I get a mortgage during an active Chapter 13 bankruptcy? Yes, on some programs. FHA, VA, and USDA can allow financing after 12 months of on-time Chapter 13 plan payments, and FHA and VA additionally require written court or trustee approval to take on the new mortgage. Conventional generally waits until 2 years from discharge.

Do extenuating circumstances really shorten the wait? They can, but only with documentation. The event must be a one-time hardship beyond your control — a serious illness, the death of a wage earner, or an involuntary job loss — supported by third-party records, plus evidence that you have re-established credit since. It is a case you document, not a box you check.

Is a short sale treated the same as a foreclosure? Not always, and that can work in your favor. On FHA and VA, if you stayed current on your mortgage through the short sale, the waiting period can be reduced or eliminated. If you were delinquent going into the sale, expect it to be treated closer to a foreclosure.

If I clear the waiting period, am I guaranteed to be approved? No. Clearing the seasoning clock only makes you eligible to apply. Approval still depends on re-established credit, verifiable income, and your capacity to repay — the guides pair every waiting period with a credit-re-establishment requirement for exactly this reason.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, endorsed by, or acting on behalf of the FHA, VA, USDA, HUD, or any government agency; FHA, VA, and USDA are registered programs of their respective agencies. All waiting periods, thresholds, and figures in this article are general, may change, and should be confirmed against current program guidelines and your specific loan file — confirm current. This article is educational and not a commitment to lend or a guarantee of any loan term. Last updated: June 2026.

Related Posts