The 2026 mortgage waiting-period matrix by loan program — Chapter 7 and 13 bankruptcy, foreclosure, deed-in-lieu, and short sale seasoning for conventional, FHA, VA, and USDA loans, sourced from the actual guides.

Should You Pay Off a Collection Before a Mortgage? The Last-Activity Trap

No — you should not pay off a collection before a mortgage until you understand which credit scores your lender actually pulls and whether paying will help or quietly hurt. The intuition is reasonable: you have an old collection sitting on your report, so you clear it before applying. But mortgage lending runs on older FICO scoring models than the ones you see in a free credit app, and on those models a freshly touched collection can look newer and more damaging than the stale one you started with. Before you send a single dollar to a collection agency, it is worth understanding the score-version gap and the “last-activity” trap that catches so many well-intentioned buyers.

The score you see is not the score your mortgage uses

Most consumers check a free FICO or VantageScore through a banking app, a card issuer, or a credit-monitoring service. Those are usually recent models — FICO 8, FICO 9, or VantageScore 3.0/4.0. Mortgage underwriting does not use those. When a lender pulls a tri-merge report, it receives three “classic” FICO scores built on older algorithms.

- Experian reports FICO Score 2 (Experian/Fair Isaac Risk Model V2).

- TransUnion reports FICO Score 4 (FICO Risk Score, Classic 04).

- Equifax reports FICO Score 5 (Beacon 5.0).

The lender typically takes the middle of your three scores; on a joint application, each borrower’s median is found and the lower of the two usually drives pricing. Because these are the numbers that set your rate and approval, they — not your app score — are the ones that matter here. If you want the fuller picture of why the number on your phone rarely matches the underwriter’s, we walk through it in our guide on why your lender’s credit score is different from the one you see.

Why “just pay it off” can be the wrong move

Here is the crux. Newer scoring models treat paid collections kindly. According to FICO, collections reported as paid in full are disregarded by FICO Score 9, and medical collections are handled more gently — unpaid medical collections over $500 carry less weight than in older versions, and paid medical debt (and medical debt under $500) is no longer reported at all. VantageScore 3.0 and 4.0 similarly ignore paid collections.

The older mortgage models do not extend that grace the same way. FICO 8 still counts a paid collection (it only disregards collections whose original amount was under $100), and the classic mortgage versions — 2, 4, and 5 — predate the paid-collection forgiveness built into FICO 9 entirely. So the very act that would lift your app score can leave your mortgage score flat, or worse.

Our take: the single most common credit mistake we see from motivated buyers is paying an old collection the week before applying because a free app “rewarded” the payoff — on a score their mortgage will never use. The payoff helped the number they saw and did nothing for, or hurt, the number that priced their loan.

The last-activity trap: how paying can make an old debt look new

Age is one of the most powerful levers in a credit score. A collection from four years ago hurts far less than one from four months ago, because scoring models discount older derogatory events. That is exactly what makes paying an aged collection dangerous.

When you pay or settle an old collection, the account’s status and reporting date can update — a phenomenon informally called re-aging. On the older mortgage models, a collection that had quietly faded into the background can suddenly register as recent activity and pull your score down at the worst possible moment. You did the “responsible” thing and your score dropped.

There is a second, legal layer. The Consumer Financial Protection Bureau warns that making a partial payment or acknowledging you owe an old debt, even after the statute of limitations has expired, may restart the time period a collector has to sue you. Most states set that limitations window between three and six years. So paying a portion of a time-barred debt can revive a collector’s right to take you to court over the whole balance. That is a real-money risk that has nothing to do with your credit score.

If you do pay, get pay-for-delete in writing first

The only version of paying an old collection that reliably helps a mortgage score is a documented deletion — the collector agrees, in writing, to remove the tradeline entirely in exchange for payment, not merely mark it “paid.” Verbal promises are worthless here. Insist on the deletion language before any money moves, and keep the agreement. A tradeline that disappears cannot re-age; a tradeline marked “paid” can. Our guide on how to dispute credit-report errors before a mortgage covers the paper trail that makes these removals stick.

Before you pay a collection: five things that change your score

Every one of the levers below can move in the wrong direction if you act without a plan. This is why the timing conversation belongs with your loan officer, not a Saturday-afternoon impulse.

- Reporting date / last activity — paying can refresh the date and make an aged item look recent on mortgage models.

- Paid vs. unpaid status — helps on FICO 9/VantageScore, often neutral on the classic mortgage FICO 2/4/5.

- Statute of limitations — a partial payment can revive a collector’s right to sue on a time-barred debt.

- Deletion vs. “paid” notation — only a written deletion removes the tradeline; “paid” leaves it scoring.

- Underwriting DTI — on FHA/USDA, an unpaid non-medical balance can add an imputed payment to your ratio.

What underwriting actually requires (it’s less than you think)

Paying a collection to raise a score and paying a collection because a program requires it are two different questions. On the requirement side, the rules are more forgiving than most buyers assume — and they differ by loan type.

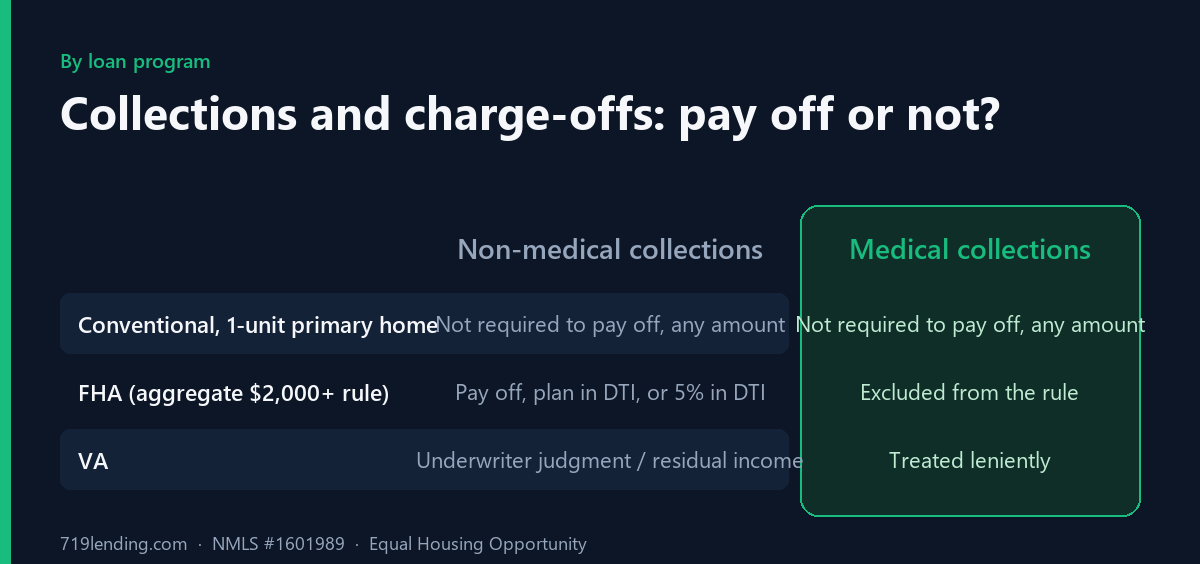

Conventional (Fannie Mae)

For manually underwritten loans, the Fannie Mae Selling Guide states that non-medical collection accounts and charge-offs on non-mortgage accounts do not have to be paid off at or prior to closing if the balance of an individual account is less than $250 or the total balance of all accounts is $1,000 or less on a one-unit principal residence. Second homes and investment properties carry their own stricter thresholds — for a second home, collections and charge-offs are generally required to be paid when the total exceeds $5,000. Critically, when the loan is run through Desktop Underwriter (DU) — as most conventional loans are — DU applies its own analysis and generally does not condition approval on paying non-mortgage collections. In other words, the automated system frequently lets an unpaid collection stand.

FHA

Under HUD Handbook 4000.1, if the total outstanding balance of all non-medical collection accounts is equal to or greater than $2,000, the lender must perform a capacity analysis: pay the balance in full, document a payment arrangement, or — absent that — include 5% of the outstanding balance as a monthly payment in your debt-to-income ratio. Medical collections are excluded from this treatment entirely. So a $10,000 non-medical collection can add a $500 imputed monthly payment to your DTI even though FHA never forces you to pay it. If that 5% figure breaks your ratio, a documented payment plan using the actual agreed payment can replace it.

VA and USDA

- VA does not require charge-offs and collection accounts to be paid off. The underwriter weighs them as part of overall credit; an unpaid collection handled by a steady repayment plan can even be read as a positive factor, while judgments and federal debts must be resolved.

- USDA mirrors the FHA logic: non-medical collections over $2,000 in aggregate trigger either a documented payment arrangement or a 5%-of-balance imputed payment in DTI, with medical collections excluded.

The through-line across all four: paying is rarely a hard requirement — it is a DTI or scoring decision. That is precisely why it should be made deliberately.

How paid collections are treated across the models

The table below is the whole argument in one place. Notice that the column on the left is the one your mortgage runs on.

| Scenario | Mortgage FICO 2 / 4 / 5 | FICO 9 & VantageScore 3.0/4.0 |

|---|---|---|

| Paid non-medical collection | Still counted; can still weigh on score | Disregarded once paid |

| Unpaid non-medical collection | Counted as derogatory | Counted as derogatory |

| Paid medical collection | Counted on classic models | Not reported / disregarded |

| Unpaid medical over $500 | Counted with older weighting | Counted with reduced weight |

| Recently re-aged (paid) old item | Can look recent and hurt | Paid status softens the blow |

| Deleted via written agreement | Removed — best-case outcome | Removed — best-case outcome |

A practical playbook

Here is how we coach borrowers through a collection during the mortgage window. Treat it as sequencing, not a to-do list to blitz.

- Do nothing impulsively. Do not pay a collection the week you plan to apply. The score effect on mortgage models is unpredictable and the timing risk is real.

- Pull the actual mortgage scores first. Have a loan officer run a soft or full tri-merge so you know your FICO 2/4/5 and which collections are even dragging on them.

- Let underwriting tell you what’s required. Often the answer is “nothing” on conventional, or “a documented plan” on FHA/USDA — cheaper and safer than a full payoff.

- If you pay, demand deletion in writing. Only a removed tradeline reliably helps. A “paid” notation can re-age the item.

- Use a rapid rescore for documented changes. If you secure a deletion or payoff, a lender-ordered rapid rescore can update your mortgage scores in days rather than a full cycle. Our explainer on rapid rescore and how lenders update credit in days shows when it is worth ordering.

- Coordinate with your loan officer on every move. The whole point is to change the right number at the right time — a broker who shops your file across wholesale lenders can also tell you which investor overlays care about that specific collection.

In our experience, the buyers who get burned are the ones who optimize for the score in their pocket instead of the score in the underwriter’s file. Sometimes the best move on a stale collection is to leave it alone, document a letter of explanation, and let the loan close. If you want the broader map of what number opens which door, start with our pillar on what credit score you need to buy a house and work outward from there.

Frequently asked questions

Will paying off a collection raise my credit score before a mortgage? Not necessarily. On the newer FICO 9 and VantageScore models you see in free apps, paying a collection helps. But mortgage lenders use older FICO 2, 4, and 5 models that still count paid non-medical collections, so the payoff may not move — or could even lower — the score that actually prices your loan.

What is the “last-activity trap” or re-aging? When you pay or settle an old collection, the account’s reporting date can refresh, making an aged item look recent. On older mortgage scoring models, a recent-looking derogatory can hurt more than the stale one did — so a well-intentioned payoff backfires right before application.

Does paying an old debt restart the statute of limitations? It can. The CFPB warns that making a partial payment or even acknowledging an old debt may restart the limitations period, which is typically three to six years by state. That can revive a collector’s right to sue you for the full balance, so old, time-barred debts deserve caution.

Does FHA require me to pay off collections? No. FHA does not force payoff, but if your non-medical collections total $2,000 or more, the lender must either use a documented payment arrangement or add 5% of the balance to your debt-to-income ratio as an imputed payment. Medical collections are excluded. All figures are general — confirm current program rules with your lender.

Do conventional (Fannie Mae) loans make me pay collections? Usually not. For manually underwritten loans, non-medical collections do not require payoff if an individual account is under $250 or the total is $1,000 or less on a one-unit primary home, and Desktop Underwriter generally does not condition approval on paying non-mortgage collections. Second homes and investment properties carry stricter thresholds.

If I decide to pay, how do I protect my score? Get a “pay-for-delete” agreement in writing before you send money, so the tradeline is removed rather than merely marked “paid.” A deleted item cannot re-age. Then ask your loan officer whether a rapid rescore can update your mortgage scores in days once the change is documented.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by FHA, VA, USDA, HUD, or any government agency; FHA, VA, and USDA are registered programs of their respective federal agencies. This article is educational and not credit, legal, or tax advice; consult a licensed professional about your situation. All scores, thresholds, dollar figures, and program rules are general and subject to change — confirm current guidelines with your loan officer before acting. Last updated: June 2026.

Related Posts