Yes – your credit score directly affects your mortgage rate. On a conventional loan, pricing is risk-based and steps through credit-score bands, so crossing a threshold like 680, 700, 720, or 740 can change both your interest rate and your monthly mortgage insurance. A higher score generally means a lower rate and cheaper mortgage insurance at the same time. (Ranges below are general – confirm current with a licensed loan officer.)

Most people know a good score “helps.” What they do not see is how the score turns into dollars on a mortgage. It is not a vague bonus – on conventional loans it runs through a published pricing grid. This post connects your score to the actual numbers on your loan estimate, and shows why a small, well-timed credit move before you apply can be worth real money.

Mortgage rates are risk-based pricing

Lenders set your rate using risk-based pricing. The Consumer Financial Protection Bureau defines it plainly: risk-based pricing is when a lender offers less favorable terms – such as a higher interest rate – based on your credit report and application. Higher scores signal lower risk, so they earn lower rates; lower scores signal more risk, so they cost more.

Your income is not on your credit report, and it is not part of your score. Income and debts decide your debt-to-income ratio (DTI) – a separate qualifier. Your credit score is the piece that prices the risk of the loan itself. Think of it this way: DTI helps decide whether you qualify; your score helps decide at what price.

General – confirm current. On conventional loans your priced rate is set where your credit-score band meets your LTV band, with mortgage insurance layered on top; FHA prices its insurance differently. Source: Fannie Mae LLPA Matrix; HUD FHA INFO 2023-11; CFPB risk-based pricing.

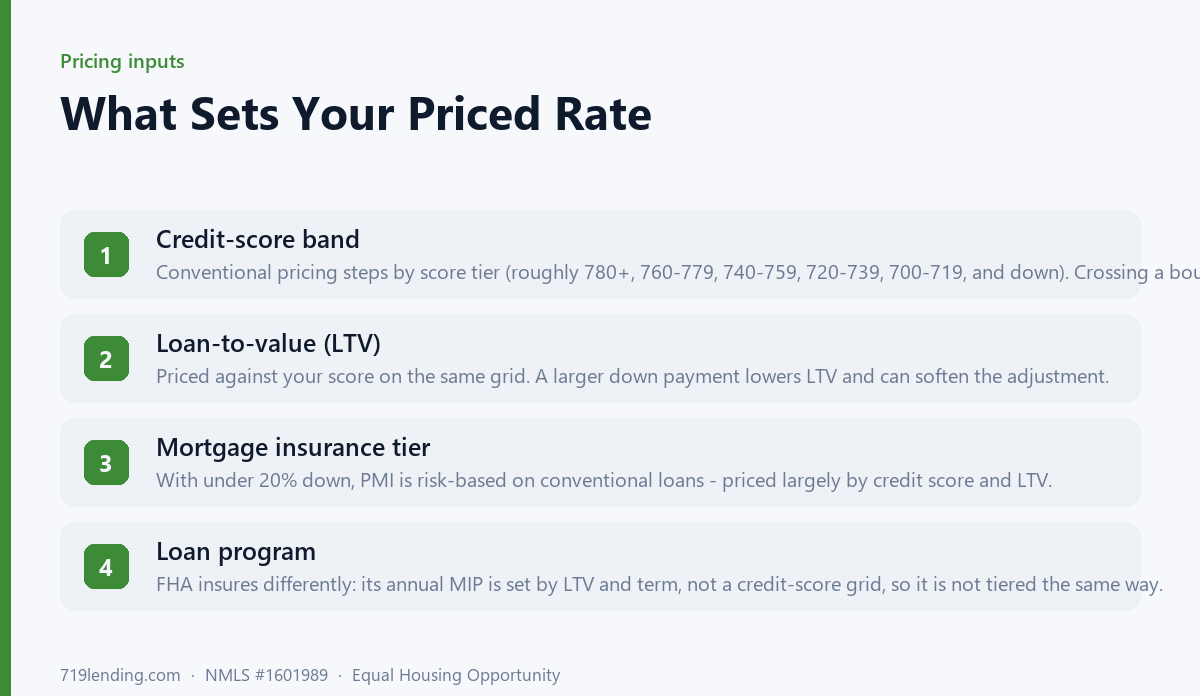

How credit-score pricing tiers work on conventional loans

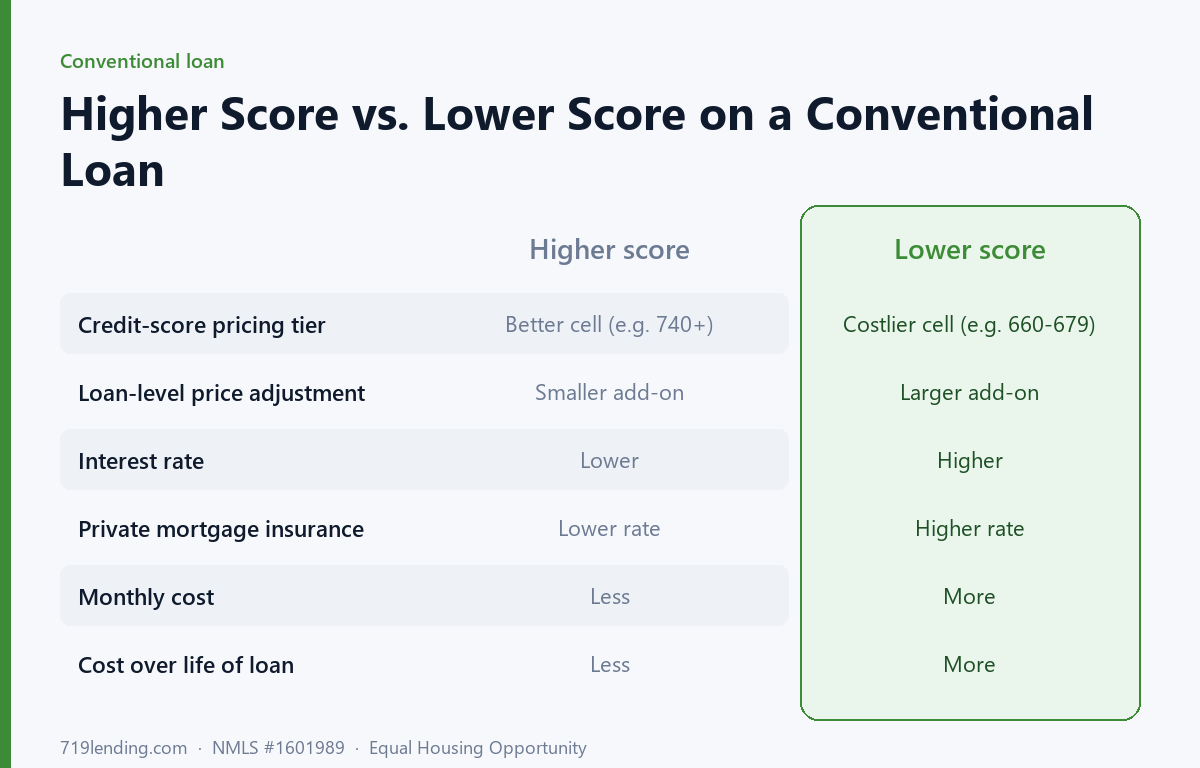

Conventional loans (the ones sold to Fannie Mae and Freddie Mac) carry loan-level price adjustments, or LLPAs. These are pricing add-ons stated as a percentage of your loan amount, and they are assessed off a published grid where your credit-score band meets your loan-to-value (LTV) band. Higher score and lower LTV land you in cheaper cells; a lower score or higher LTV lands you in costlier ones.

The score bands are stepped, roughly like this (general – confirm current):

780 and above

760 – 779

740 – 759

720 – 739

700 – 719

680 – 699

660 – 679

640 – 659

620 – 639

Below 620

After the pricing overhaul that federal regulators directed in 2023, the best-priced tier moved up to 780+. Two things matter here for a borrower. First, pricing is tiered, not perfectly smooth – so a handful of points that pushes you from one band into the next can change your cost, while points that stay inside a band may not. Second, because the grid crosses score against LTV, a bigger down payment can soften an LLPA, and a bit more score can too. The adjustment is not a rate you “see” – it gets baked into the rate or the closing costs your lender quotes.

The band jump: what crossing a tier can mean

Because the grid is stepped, the borrower who benefits most is the one sitting just below a boundary. Crossing from 718 to 720, or 738 to 740, can move you into a cheaper cell. The exact dollar effect depends on your loan size, LTV, program, and the day’s market – so treat the following as a general illustration, not a quote.

Consider a $400,000 conventional loan. Suppose a borrower crosses a pricing tier and their rate improves by even a quarter of a percent – say from the high-6s to the mid-6s (illustrative, general – confirm current). On a 30-year loan, a 0.25% lower rate on $400,000 is roughly $60 – $70 less per month, which is on the order of $20,000 – $25,000 less interest over the full 30 years. Add cheaper mortgage insurance on top (more below), and a single tier can quietly shift the total cost of the loan by a meaningful amount.

None of that is a promise of a specific rate or a specific point gain – scoring and pricing are individual. The point is directional and reliable: on conventional financing, moving up a credit-score tier tends to lower both your rate and your insurance cost at once.

General, illustrative – confirm current. On conventional loans, a higher credit-score tier tends to lower both the rate and PMI; on a $400,000 loan a 0.25% lower rate is roughly $60-$70 less per month and about $20,000-$25,000 less interest over 30 years. Source: Fannie Mae LLPA Matrix; MGIC risk-based pricing.

Your score also prices your PMI

If you put less than 20% down on a conventional loan, you pay private mortgage insurance (PMI). PMI is also risk-based. The mortgage insurers – MGIC, Radian, Enact, Essent, National MI and others – price with what MGIC calls a “risk-based pricing model,” driven largely by credit score and LTV. A higher score generally buys a lower PMI rate; a lower score costs more, sometimes several times more for the same loan.

This is why the score payoff compounds. Cross a tier and you can improve the interest rate and the PMI factor together – two separate monthly line items both moving in your favor. It is one of the clearest cases in a mortgage where a better score is not cosmetic; it is cash flow.

FHA prices differently – MIP is not credit-tiered the same way

Not every loan uses credit-score pricing tiers the way conventional does. On an FHA loan, the mortgage insurance premium (MIP) is set by loan-to-value and loan term – not by your credit score. HUD lowered the annual MIP for most FHA loans to 0.55% in 2023, and that figure is the same whether your score is 620 or 760, because FHA MIP is structured by LTV and term rather than by a credit-score grid.

That does not mean score is irrelevant on FHA – it still affects the interest rate a lender offers and whether you qualify at all. But the insurance piece behaves differently than conventional PMI. For a borrower with a lower score, that structural difference is exactly why an FHA loan sometimes pencils out better than conventional – the conventional LLPA and PMI hits can outweigh FHA’s flat MIP. A good broker runs both and compares. Government agencies (FHA, VA, USDA, CHFA) do not endorse and are not affiliated with any particular lender or broker.

On a joint application, the lower score sets the price

When two borrowers apply together on a conventional loan, the lender does not average your scores. Per Fannie Mae’s Selling Guide, the lender determines each borrower’s representative score, then selects the lowest of them as the representative credit score for the loan – and that is the score used for pricing (assessing LLPAs). So a 760 paired with a 660 gets priced off the 660.

That usually is not an automatic denial – you often still qualify, just at the worse tier’s rate and LLPA. It sets up a real decision: apply together (add the second income for DTI, take the pricing hit) or apply solo (keep the stronger pricing, lose the second income). There is no one right answer – it depends on your numbers, and it is worth modeling both ways.

Why a small paydown or a rapid rescore can be worth real money

Here is where the pricing grid becomes a to-do list. Because conventional pricing is tiered, the highest-value credit move before you apply is often the one that nudges you across a boundary – not a heroic 100-point rebuild.

Credit utilization paydown. Utilization is one of the fastest-moving score factors. Paying revolving balances down before your statements report can lift the score – and if it crosses a tier, it changes your price, not just your appearance. See our guide on credit utilization before a mortgage.

Rapid rescore. Already under contract and a paydown or corrected error would cross a tier? A lender-ordered rapid rescore can update the bureaus in a few business days, capturing the improvement in time to reprice the loan. It is the in-transaction version of every “wait a few months” lever.

The mortgage math is what makes these worth doing. A 15-point bump that stays inside a band may not move your quote; the same 15 points that carries you from 719 to 720, or 739 to 740, can lower your rate and your PMI. That is why timing the paydown to the lender’s pull – and knowing exactly which boundary you are near – beats a generic “raise your score.”

The bottom line

Does credit score affect mortgage rate? On conventional loans, unmistakably – it prices your rate and your PMI through stepped credit-score tiers, and the lower score governs a joint file. FHA insures differently, which can flip the better deal for lower-score borrowers. The practical takeaway is simple: know your score and the nearest pricing boundary before you lock, because a small, well-timed move there is one of the few places in a mortgage where a little effort turns into lasting savings.

Frequently asked questions

Does my credit score really change my mortgage rate, or just whether I qualify? Both. Score is a major input into whether you qualify and, on conventional loans, into the price – through loan-level price adjustments that step by credit-score band and LTV. Higher score generally means a lower rate. Income is separate; it is not on your credit report and feeds DTI, not your score.

How many points do I need to gain to change my rate? There is no fixed number – it depends on where you sit relative to a pricing tier. Conventional pricing is banded (roughly 780+, 760-779, 740-759, 720-739, and so on), so the points that matter are the ones that cross a boundary. A few points inside a band may not move your quote; the same points across 700, 720, or 740 can. This is general – confirm current with a loan officer.

Does a higher score also lower my PMI? On conventional loans, generally yes. Private mortgage insurance is risk-based and priced largely by credit score and LTV, so a higher score usually earns a lower PMI rate. That is why moving up a tier can improve your interest rate and your insurance cost at the same time.

Does credit score affect FHA mortgage insurance? Not the way it affects conventional PMI. FHA’s annual mortgage insurance premium is set by loan-to-value and loan term, not by a credit-score grid – HUD cut it to 0.55% for most FHA loans in 2023. Your score still affects the FHA interest rate and whether you qualify, but the insurance premium itself is not credit-tiered.

We are applying together – whose score gets used? On a conventional loan the lender uses the lowest borrower’s representative score for pricing, per Fannie Mae’s Selling Guide. It usually is not an automatic denial – you often still qualify, just at that lower tier’s rate and adjustments. Whether to apply jointly or solo is a numbers decision worth modeling both ways.

I am about to buy – is it worth paying down a card or ordering a rapid rescore? It can be, if it crosses a pricing tier. A utilization paydown timed before your statements report, or a lender-ordered rapid rescore during the transaction, can capture points fast enough to reprice the loan. The value is in crossing a boundary near your current score, not in a large general increase.

Last updated: June 2026. 719 Lending Inc, NMLS #1601989. Equal Housing Opportunity. Figures and ranges above are general and illustrative – confirm current pricing, program rules, and eligibility with a licensed loan officer for your specific scenario. We do not promise any particular rate, approval, or credit-score outcome. Government agencies (FHA, VA, USDA, CHFA) do not endorse and are not affiliated with 719 Lending or any lender or broker.

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.