Payment history is the single largest factor in your credit score, about 35 percent, and it is one of the first things a mortgage underwriter looks at. A late payment is generally only reported to the bureaus once you are a full 30 days past due, so a few days late is usually recoverable, but an accurate late that does post cannot be deleted just because you ask, and mortgage underwriting grades housing lates on an even harsher curve than the scoring model does. If you have a late in your recent history and a home purchase on the horizon, the moves that help are pre-application moves. This guide walks through what actually counts as late, why the damage is often worse for people with good credit, and the realistic recovery playbook. Figures are general, confirm current.

Last updated: June 30, 2026.

Why payment history matters more than anything else

FICO builds its score from five categories, and payment history is the heaviest at about 35 percent of the total, according to FICO’s own education materials. Lenders read your track record of paying past accounts as the strongest single predictor of whether you will pay the next one. Everything else on the report, how much you owe, how long you have had credit, is secondary to the simple question: do you pay on time?

For a mortgage, this factor carries extra weight because the underwriter does not just see your score, they read the actual payment grid on your report and react to what they see there, especially on housing debt. So two things are true at once: lates cost you score points, and lates can independently trigger problems in underwriting even when your score still looks fine.

What actually counts as a late payment

Being a day or a week late is not the same as a reported late. As a matter of standard creditor practice, most lenders do not report an account as past due to the credit bureaus until you are a full 30 days past the due date. You may owe a late fee the moment you miss the date, but the credit-report damage usually does not attach until that 30-day mark. That gap is a genuine runway: if you catch the payment up inside those 30 days, in most cases nothing hits your report. Policies vary by creditor, so do not treat it as a guarantee.

Once you cross the line, lates are graded by severity and get worse as they climb:

30 days past due is the first reportable tier and the most common.

60 days past due is a meaningful step down.

90 days or more is severe and is where a lot of the score damage concentrates.

A missed payment does not vanish quickly. Accurate negative information, including a late payment, can generally remain on your credit report for up to seven years, according to the Consumer Financial Protection Bureau. Its sting fades long before it falls off, but it stays visible.

The counterintuitive rule: a higher score loses more

Here is the part that surprises people. The higher your score, the more a single late tends to cost you. The reason is intuitive once you see it: someone with a strong, clean history and a high score has further to fall, because one new sign of risk is a bigger deviation from an otherwise spotless record. Someone whose score is already lower has, in a sense, already reflected past missteps, so one more late moves the number less. FICO’s published figures bear this out, with a single 30-day late capable of pulling far more points off a very good or excellent score than off a fair one.

The practical takeaway is not to feel worse about a good score, it is to protect it. If you are in the 700s or higher and planning to buy, a single 30-day late can pull a surprisingly large number of points, and it can knock you out of a pricing tier that matters for your rate and mortgage insurance.

FICO weighs recent activity more heavily than old activity, so the same 30-day late lands very differently depending on when it happened. General illustration, confirm current.

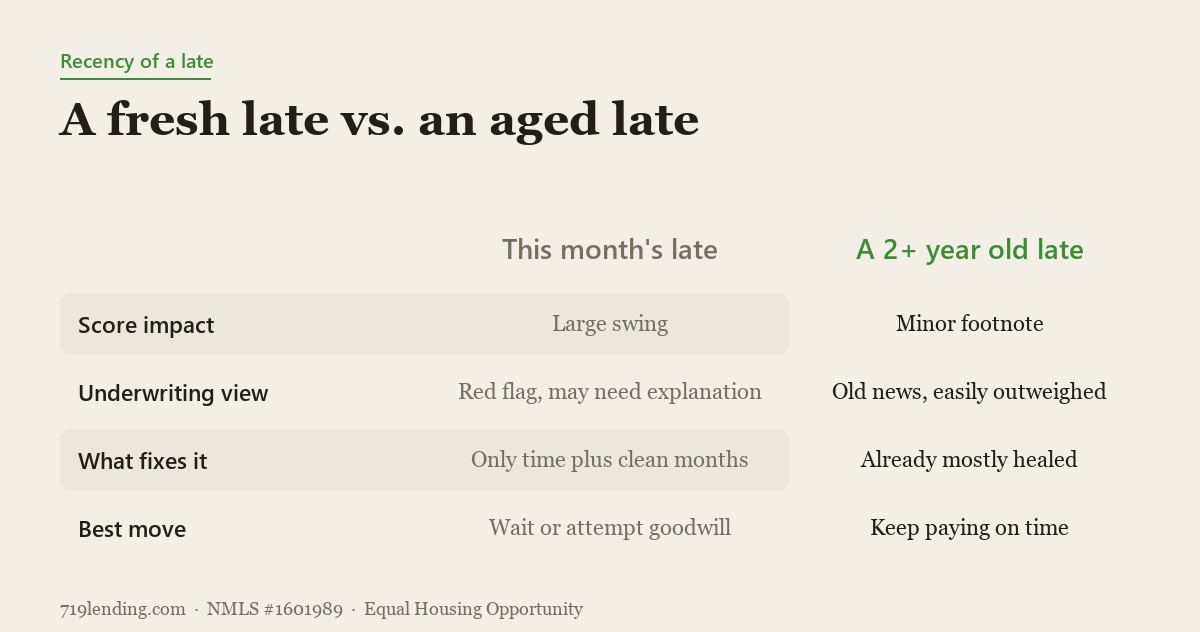

Recency is everything

Not all lates weigh the same over time. FICO is explicit that older credit problems count less toward your score than recent ones. A late from two or three years ago, with clean payments since, is a minor footnote. A late from this month is the big swing. The score is asking a forward-looking question, is this person a risk right now, and recent behavior answers it more loudly than old behavior.

This is also why recovery is mostly about time plus clean months stacked on top. You cannot erase an accurate late, but you can bury it under a long, unbroken run of on-time payments, and the score rewards that runway.

How mortgage underwriting grades a housing late

This is where the mortgage layer diverges hard from the generic credit advice you will find online. Automated underwriting engines and manual underwriters do not treat a housing or mortgage late the way the FICO number does. They apply a separate, stricter standard, and one recent housing late can create conditions, force a manual review, or sink a file regardless of the score.

Fannie Mae’s Selling Guide is blunt about it. It defines an excessive prior mortgage delinquency as any mortgage tradeline with one or more 60-, 90-, 120-, or 150-day delinquency reported within the 12 months prior to the credit report date, and it states that loans with excessive prior mortgage delinquencies are not eligible for delivery to Fannie Mae. In plain terms: a recent, serious mortgage late can make a conventional loan unsalable, no matter how good the rest of the file looks.

FHA and VA files that go to manual underwriting look hard at the most recent 12 months of housing and installment payments, with housing payment history weighing heavily. A clean 12-month rent or mortgage history can be the difference between an approval and a denial on a manual file, and a recent housing late is one of the fastest ways to lose that benefit of the doubt. These are program- and investor-dependent rules, so confirm current guidelines with your loan officer.

Why you cannot dispute an accurate late off your report

A recent, accurate late is the one thing credit repair cannot fix. The CFPB is clear that you generally cannot have accurate negative information removed from your credit report, and it warns consumers to walk away from any company that claims it can remove information that is current, accurate, and negative, calling it a likely credit repair scam. Disputing an accurate item just gets it verified, and mid-application a disputed tradeline can actually stall your mortgage file rather than help it.

The only legitimate removal is a genuine error. If a payment you made on time is reported late, or a late is reported on the wrong month, or the account is not yours at all, you can dispute that for free and it should come off.

The one long-shot: a goodwill deletion

There is a single non-error path, and it is a favor, not a right. A goodwill deletion is a request to the creditor, not the bureau, asking them to voluntarily remove an accurate late as a courtesy, usually on the strength of a long history of on-time payments and a one-time hardship. No law requires a creditor to grant it, and many will not. When it works, it tends to work for isolated lates on otherwise pristine accounts.

Because it is slow and uncertain, a goodwill deletion is a pre-application play, something to attempt weeks or months before you need a clean report, not a mid-escrow rescue. If it lands before your lender pulls credit, great; if it does not, you were not counting on it.

You cannot erase an accurate late, but these pre-application moves control what happens from here. General information, confirm current.

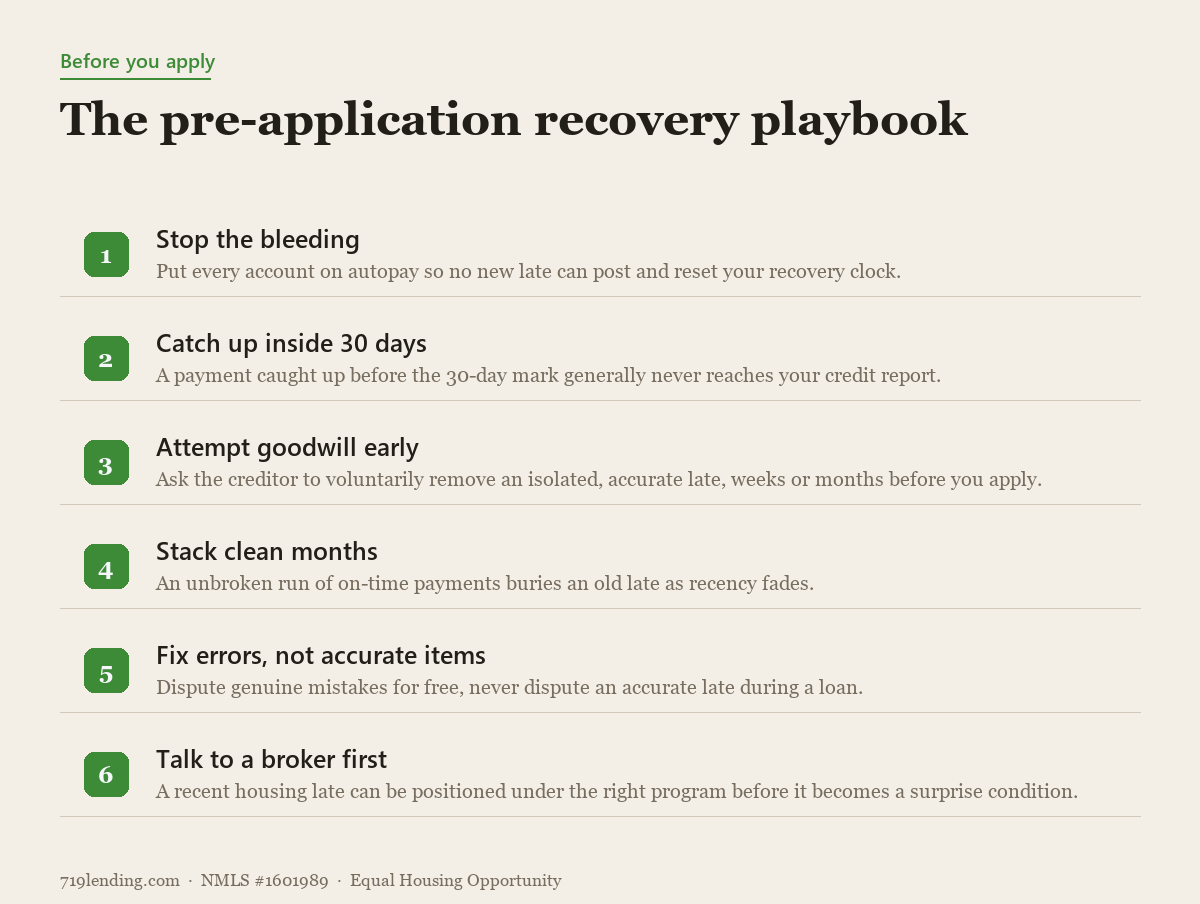

The recovery playbook before you apply

You cannot rush the calendar, but you can control what happens from here. The realistic sequence:

Stop the bleeding. Put every account on autopay for at least the minimum so no new late can post. One more late resets your recovery clock.

Catch up anything inside the 30-day window immediately before it becomes reportable.

Attempt goodwill deletions early on isolated, out-of-character lates, well ahead of any application.

Let clean months accumulate. Recency fades, and a stretch of on-time payments is what rebuilds the score.

Fix real errors, do not dispute accurate items, especially not while a loan is in process.

Talk to a mortgage broker before you apply, so a recent housing late can be positioned, explained, or waited out under the right program instead of surfacing as a surprise condition.

Frequently asked questions

Will one late payment stop me from getting a mortgage? Not automatically. A single non-housing late usually costs score points but rarely blocks a loan on its own. A recent housing or mortgage late is the bigger risk, because underwriting grades those on a stricter curve and, on conventional loans, a serious recent mortgage late can make the loan ineligible for sale to Fannie Mae. Talk to a loan officer about program options.

How many points will a late payment drop my score? There is no fixed number, it depends on your profile. Counterintuitively, the higher and cleaner your score, the more a single late tends to cost, because it is a bigger break from an otherwise spotless record. A recent, severe late costs more than an old, minor one.

Can I get an accurate late payment removed from my credit report? Not by disputing it. The CFPB states that accurate negative information generally cannot be forced off your report and warns against companies that promise to delete current, accurate, negative items. Accurate lates generally fall off on their own after about seven years. The only voluntary path is a goodwill deletion, which the creditor is free to refuse.

What is a goodwill deletion and does it work? It is a request asking the original creditor, not the bureau, to remove an accurate late as a one-time courtesy, usually based on a strong payment history. It is entirely voluntary, there is no guarantee, and it works best on isolated lates. Because it is slow and uncertain, attempt it before you apply, not during escrow.

How long does a late payment stay on my credit report? Generally up to seven years, according to the CFPB. Its impact on your score shrinks well before then, because FICO weighs recent activity more heavily than old activity.

Does a mortgage late hurt more than a credit-card late? For underwriting, yes. The scoring model treats a late as a late, but mortgage underwriters read housing payment history closely and hold it to a tighter standard. A recent housing late can trigger a manual review, conditions, or ineligibility on some programs even when your score still looks acceptable.

This article is general education, not credit, financial, or lending advice, and every figure is general, confirm current. Programs, guidelines, and credit-reporting rules change and vary by lender and investor. 719 Lending Inc, NMLS #1601989, is an Equal Housing Opportunity broker and is not affiliated with, or acting on behalf of, any government agency, including FHA, VA, USDA, or CHFA. Contact us to review your specific situation.

How to dispute credit report errors under the FCRA before a mortgage: the ~30-day timeline, how to document it, and why an active dispute remark can stall automated underwriting. 719 Lending, NMLS #1601989.

Thinking about disputing hard inquiries before your mortgage? For inquiries you actually authorized, it usually backfires - and can freeze your loan file. Here is the safe, correct approach.

Does shopping for a mortgage hurt your credit? Barely. Rate-shopping models bundle your mortgage inquiries into one. Here is how to shop many lenders safely.