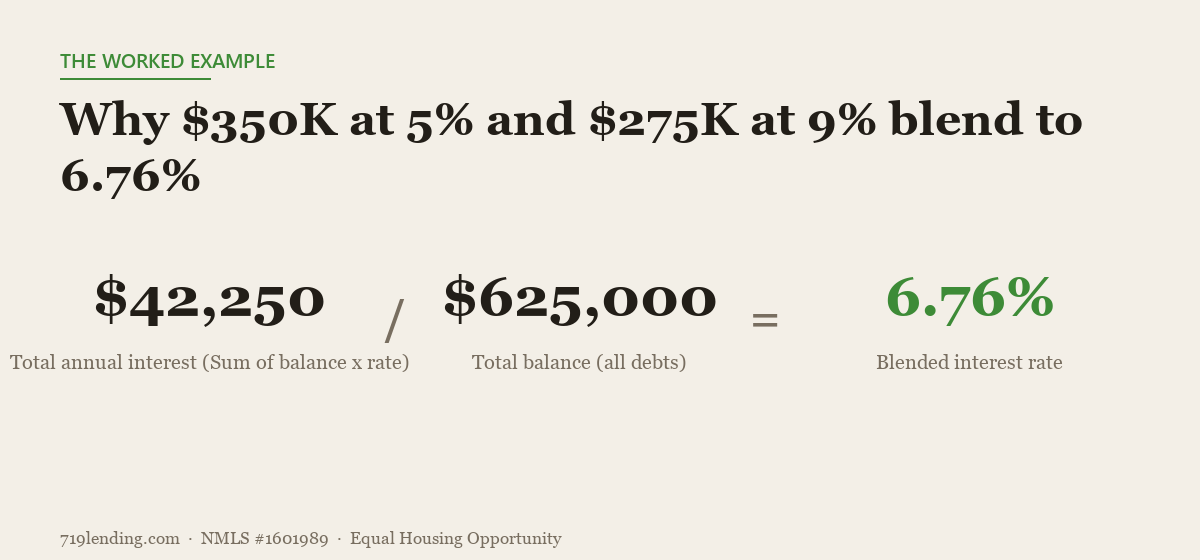

Plain-averaging your loan rates lies to you. A $350k loan at 5% plus a $275k loan at 9% isn't 7% — it's a weighted blend of 6.76%. Here's the one number that tells the truth, and why a lower rate can still cost you more.

Should I refinance? The true break-even (and the trap that can cost you $40,000)

Last updated: June 30, 2026 — FHA, VA funding fee, and PMI figures reflect current 2026 guidelines; confirm current rates and fees before deciding.

A lower monthly payment is not the same as a win. When you refinance, the only money you truly lose is interest, mortgage insurance, and closing costs — principal stays yours as equity. 719’s Refinance Comparison calculator ranks each option by that “money gone” figure and estimates the true month your refinance actually pays for itself — which is often years later than the payment drop suggests.

Why can a lower payment still lose you money?

Because a refinance resets the clock. If you’re seven years into a 30-year loan, a chunk of every payment now goes to principal — you’re past the front-loaded-interest hump. Refinancing into a fresh 30-year term drops your payment partly by re-amortizing the balance over 30 new years, which throws you back to year one where almost every dollar is interest again.

So the headline savings are real on a monthly basis, but stretched across a longer tail you can pay more total interest over the life of the loan. That’s the refinance trap: the payment goes down, the lifetime cost goes up, and a naive “cash break-even” (closing costs ÷ monthly savings) tells you you’re winning while you quietly bleed. On the wrong loan, that gap can run into the tens of thousands — the kind of $40,000 mistake the headline number hides. The calculator builds a full amortization schedule for your current loan and each refinance option, then compares the cumulative “money gone” curves month by month so you see the truth, not just the first month’s headline.

What is “money gone,” and why exclude principal?

“Money gone” is the cash you never get back: cumulative interest paid, mortgage insurance (PMI, FHA MIP, or VA funding fees), and closing costs. Principal is excluded on purpose — every principal dollar converts cash into equity you still own. Ranking options by money gone instead of by payment is the entire point. A refinance with a slightly higher payment but far less lifetime interest can be the better deal, and only a money-gone view surfaces that.

The tool compares your current loan against up to two refinance quotes — a true three-way race — and ranks them. It auto-applies the right fees so you don’t have to: FHA’s 1.75% upfront MIP plus annual MIP, VA funding fees (0.5% on an IRRRL, 2.15% on a first cash-out use, 3.3% on subsequent use), and conventional PMI that drops off at your chosen LTV (78% by default). Rolled-in closing costs, cash-out, and debt consolidation are modeled too. These outputs are estimates for comparison, not loan terms.

Cash break-even vs. true break-even: what’s the difference?

The calculator shows both side by side, and the gap between them is where the trap lives.

| Break-even type | What it measures | Why it can mislead |

|---|---|---|

| Cash break-even | Closing costs ÷ monthly payment savings | Ignores that you reset the amortization clock and may pay more lifetime interest |

| True (equity) break-even | The month the refinance’s total “money gone” curve crosses below keeping your current loan | It’s honest — and sometimes the answer is “Never” |

When the two curves never cross — meaning the refinance never actually costs you less than staying put — the tool returns “Never” instead of inventing a rosy number. That honesty is the differentiator. If a refinance can’t pay for itself within your time horizon, you deserve to know before you sign. Run your numbers in the Refinance Comparison calculator and watch where (or whether) the curves cross.

The same-payment trick: turn a lower rate into an earlier payoff

Here’s the move most refinance calculators won’t show you. Instead of pocketing the monthly savings, keep paying your old (higher) payment on the new lower-rate loan. The extra goes straight to principal, and the tool models exactly what that does: your new payoff date, how many months sooner you’re mortgage-free, and the interest you save.

This flips the trap on its head. The same lower rate that could have cost you lifetime interest now becomes a payoff date years sooner — the calculator can show an outcome like “mortgage-free 6 years 2 months sooner” (an example output, not a quote). You used the better rate as a weapon to attack the loan instead of a reason to slow it down.

What does the calculator actually give me?

For your current loan and each refinance option, you get:

- New payment and monthly savings — the headline, kept in context.

- Money gone at your horizon — total interest + MI + fees, the real cost ranking.

- Cash break-even AND true break-even — side by side, including an honest “Never.”

- Financed fee and MI end month — when FHA MIP or PMI actually falls off.

- Same-payment payoff — payoff date, months sooner, interest saved.

- Invested-savings future value — if you’d rather pocket and invest the savings, an honest projected value at your assumed return and appreciation rate.

- A branded PDF you can save or bring to your loan officer.

A few honest touches under the hood: a $250 “dead-band” calls a near-tie a wash instead of pretending one option wins by pocket change, and debt consolidation lets you roll in specific debts per-line so you see the full picture of a cash-out or consolidation refinance.

Which inputs matter most?

The result swings hardest on three things: how many months are left on your current loan (the closer you are to payoff, the more a reset hurts), your time horizon (how long you’ll keep the loan or the home), and the rate and term of each new option. You’ll enter your current loan’s value, payoff, rate, months left, and any MI; then per refinance, the type (conventional, FHA, VA IRRRL, or VA cash-out), rate, term, closing costs, roll-in, cash-out, and PMI settings; plus any debts to consolidate and your investment/appreciation assumptions.

Want to see your own three-way comparison? Try the Refinance Comparison calculator, or browse every 719 tool on the Calculate hub. As a Colorado Springs mortgage broker, 719 Lending shops your scenario across lenders — the honest math just helps you decide whether refinancing is worth doing at all.

Frequently asked questions

If my payment drops, am I automatically saving money? No. A lower payment can come from stretching the balance over a fresh 30-year term, which can raise your total lifetime interest even as the monthly number falls. The calculator’s “money gone” ranking and true break-even show whether you’re actually ahead.

What does a “Never” break-even mean? It means the refinance’s cumulative cost curve never drops below keeping your current loan within the timeframe — so it never truly pays for itself. The tool reports this honestly instead of fabricating a break-even month.

How can refinancing help me pay off sooner? Use the same-payment scenario: refinance to a lower rate but keep paying your old, higher payment. The extra goes to principal, and the calculator shows your new payoff date, months saved, and interest avoided.

Does the calculator handle FHA, VA, and PMI fees? Yes. It auto-applies FHA upfront and annual MIP, VA funding fees by use type, and conventional PMI that drops off at your set LTV (78% default), and shows the financed fee and the month MI ends.

Are the results a loan offer? No. All outputs are estimates for comparison only. Your actual rate, fees, and terms depend on a full application and approval.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Related Posts