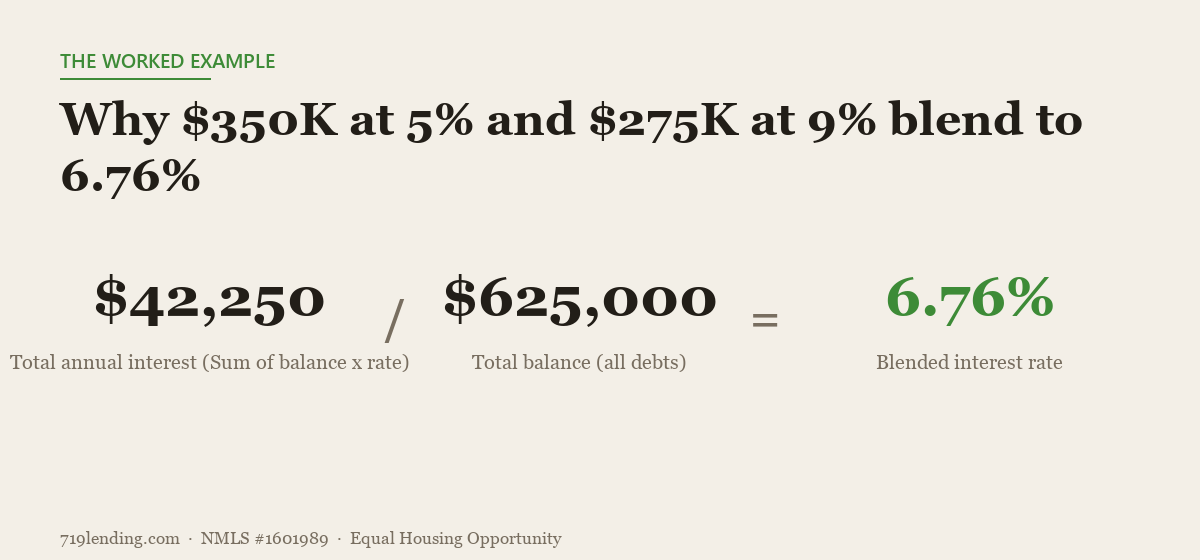

Plain-averaging your loan rates lies to you. A $350k loan at 5% plus a $275k loan at 9% isn't 7% — it's a weighted blend of 6.76%. Here's the one number that tells the truth, and why a lower rate can still cost you more.

Pay off your mortgage or invest? The honest payoff-vs-invest calculator that refuses to cheat

Last updated: June 30, 2026 — illustrative figures (7% expected return, 6.5% loan rate) are general examples for the calculator; confirm current rates and returns for your own situation.

Should you throw extra cash at your mortgage or invest it instead? On paper a 7% expected return beats a 6.5% loan, so investing looks like the winner. But the answer can flip once you weigh three things: a fixed mortgage rate is certain while market returns are only hoped for, your sale date caps how long compounding runs, and one bad year can erase a thin edge. The Early Payoff vs. Invest calculator runs both strategies with the same dollars, month by month.

Why does 7% sometimes lose to a 6.5% mortgage?

Because not all percentages are created equal. The 6.5% you save by paying down your mortgage is fixed and certain. The 7% you might earn in the market is an expectation, not a promise, and it arrives with volatility attached. When the gap between your expected return and your loan rate is thin, the certainty of the payoff side can outweigh the slightly higher (but risky) investment return, especially over shorter horizons.

This is the core insight most calculators bury. A certain return has real value that a hoped-for return does not. As the tool’s own risk callout puts it: a small dollar edge can vanish in one bad year, which is why many families simply split the difference and do some of each.

How does the calculator decide a winner?

You give it a mortgage and a fixed amount of extra cash per month. It then runs two strategies head to head, using the same dollars in each, simulated month by month:

- Strategy 1 (Pay down): every extra dollar goes toward principal, shrinking your balance and the interest you’ll ever pay.

- Strategy 2 (Invest): every extra dollar goes into an investment growing at your expected return, with the compounding frequency you select.

A key honesty feature: if the loan pays off early under Strategy 1, the calculator doesn’t let that freed-up monthly payment disappear. It invests the freed payment for the remaining months until your sale date, so no money vanishes from either side of the comparison. At your horizon, it reports the winner and the dollar margin between them, plus a dashed “contributions-only” baseline so you can see how much of each result is growth versus your own deposits.

What’s the “double-count” bug it refuses to repeat?

This is the differentiator. The legacy version of this tool cheated, almost certainly by accident. On the payoff side, it added “interest savings” on top of “additional equity,” which counts the same benefit twice. Every extra principal dollar already shows up as equity; the interest you avoid is a consequence of that, not a separate pile of money to stack on top.

The rebuild scores the payoff strategy honestly: your contributions plus the interest you never have to pay, with no double-counting (and that’s verified by a test). It also fixes a dead compounding selector in the old tool, so when you choose monthly, quarterly, or annual compounding, it actually changes the result. Honest math is the whole point: if a comparison tool inflates one side, it can talk you into the wrong decision.

Which inputs actually move the answer?

The tool frames your time horizon as the single biggest factor, and for good reason: compounding needs time to work, and your sale date is the hard stop. Here’s what you’ll enter and what each input controls.

| Input | What it controls |

|---|---|

| Loan amount, rate, term | Your baseline mortgage and how much interest is on the table |

| Extra cash per month | The identical dollars deployed in both strategies |

| Expected return % | The hoped-for growth rate on the invest side |

| Compounding | How often investment gains compound (it actually works now) |

| Horizon | When you sell or stop, the “single biggest factor” |

| First payment date | Anchors the month-by-month schedule |

On the output side you get the winner and dollar margin, the payoff benefit (equity built, interest avoided, and any post-payoff investing), the portfolio value and ROI on the invest side, months to payoff, a race chart of the two strategies, and a branded PDF you can save or share. Want to see your own numbers? Run them in the Early Payoff vs. Invest calculator.

What outcomes might I see?

The verdict isn’t fixed, and that’s the honest part. Depending on the gap between your return and your rate, and your horizon, the calculator can land on several different answers. These are illustrative examples of the outcome types, not predictions for your situation:

| Scenario (example) | Typical verdict |

|---|---|

| 7% expected return vs 6.5% loan, 10-year horizon | “Investing wins by $X” — but a thin edge |

| Lower return or higher loan rate | “Paying down wins by $X” |

| Loan clears before your sale date | Freed payment invested for the remaining months |

| Return and rate nearly identical | “Too close to call” — split the difference |

Notice how the winner flips with the rate/return gap and the horizon. That’s exactly why a single rule of thumb (“always invest the difference” or “always kill the mortgage”) fails. You need your numbers, not a slogan.

How should I read a “thin edge” result?

Carefully. If the calculator says investing wins by a small margin, remember what that margin is made of: a certain saving on one side versus a hoped-for return on the other. The mortgage rate is fixed; the market return is not. A single down year can erase a slim advantage and then some.

The tool’s investment-return tooltip is deliberately honest about this: the S&P 500 has historically returned roughly 10% before inflation, with 7% often used as a conservative, after-inflation planning figure, and none of it is guaranteed the way your fixed mortgage rate is. So a thin “investing wins” verdict carries real downside, while a thin “paying down wins” verdict is closer to a sure thing. Many families respond by doing both: putting some extra toward principal and some into the market, capturing certainty and upside at once.

This decision often shows up alongside a refinance. If you’re weighing it, the 719 Lending calculator hub has the full lineup, and a quick conversation with a Colorado Springs broker can help you frame the right horizon before you run the numbers.

The bottom line

Paying down your mortgage versus investing isn’t a math contest you can settle with a single percentage. It’s a question of certainty versus upside, decided by your loan rate, your expected return, and how long you’ll actually hold the home. Skip the rules of thumb and the double-counting shortcuts. Try the Early Payoff vs. Invest calculator, enter your real numbers, and let the honest, double-count-free math show you which strategy builds more wealth by your sale date. Results are estimates, not promises, so use them as a starting point for a real conversation.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Frequently asked questions

Is it better to pay off my mortgage early or invest the money? It depends on the gap between your expected investment return and your fixed mortgage rate, and on how long you'll hold the home. A higher return favors investing, but a certain rate and a shorter horizon favor paying down. The Early Payoff vs. Invest calculator runs both strategies with the same dollars month by month and reports which built more wealth by your sale date. Results are estimates.

Why does a 7% return sometimes lose to a 6.5% mortgage? Because the 6.5% saving from paying down your mortgage is fixed and certain, while a 7% market return is only expected and comes with volatility. When the edge is thin, the certainty of the payoff side can outweigh the slightly higher but risky investment return, especially over shorter horizons where one bad year can erase the difference.

What was the double-counting bug in the old calculator? The legacy tool added 'interest savings' on top of 'additional equity' on the payoff side, counting the same benefit twice. The rebuilt Early Payoff vs. Invest calculator scores payoff honestly as your contributions plus the interest you never pay, with no double-counting, and that is verified by a test.

What happens if my loan pays off before I sell? The calculator doesn't let the freed-up monthly payment vanish. On the pay-down strategy, once the loan is gone it invests that freed payment at your expected return for the remaining months until your horizon, so both strategies use the same dollars over the same period for a fair comparison.

Which input matters most in the payoff-vs-invest decision? Your time horizon. The calculator frames it as the single biggest factor because compounding needs time to work and your sale date is the hard stop. The winner can flip based on your horizon and the gap between your expected return and your loan rate, which is why a single rule of thumb fails. Results are estimates.

Related Posts