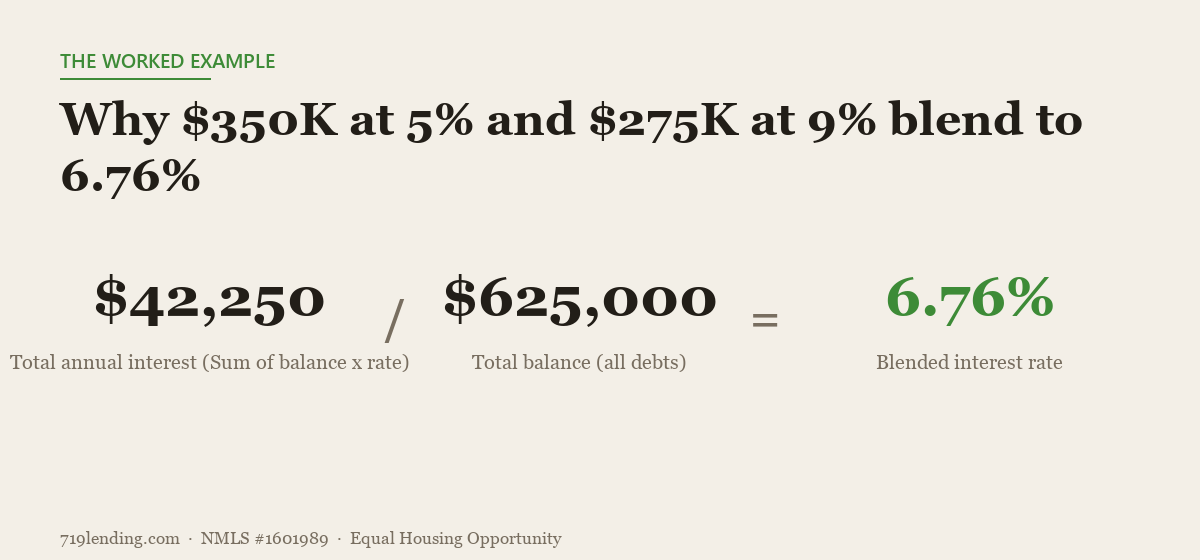

Plain-averaging your loan rates lies to you. A $350k loan at 5% plus a $275k loan at 9% isn't 7% — it's a weighted blend of 6.76%. Here's the one number that tells the truth, and why a lower rate can still cost you more.

Are bi-weekly mortgage payments worth it? The free trick that gets you ~97% of the savings

Last updated: June 30, 2026 — example based on a $350,000 loan at 6.5% over 30 years (~$2,212/month). Rates and figures are illustrative; confirm current terms for your own loan.

Bi-weekly mortgage payments can shave roughly five to six years and a large amount of interest off a typical 30-year loan — but the magic isn’t the every-other-week schedule. It’s that 26 half-payments equal 13 full payments a year, one more than monthly. You can capture about 97% of that benefit for free by adding 1/12 of your payment to principal each month, no program required.

That’s the honest version most lenders won’t lead with. Many sell a bi-weekly “enrollment” product, sometimes with a setup fee or a per-payment charge. Our bi-weekly payment calculator exists partly to talk you out of paying for one. It amortizes your loan three ways at the same rate — standard monthly, true bi-weekly, and a fee-free do-it-yourself approach — so you can see exactly where the savings come from and decide whether any program is worth a dime. Run your numbers here.

Where does the savings actually come from?

The 13th payment. That’s it. A monthly mortgage makes 12 payments a year. A true bi-weekly schedule charges half your monthly payment every two weeks — and because there are 52 weeks in a year, that’s 26 half-payments, which equals 13 full payments. That one extra payment goes almost entirely to principal, and knocking down principal early starves the loan of the interest it would have compounded for decades.

People assume paying “more often” is what helps — that hitting the balance every two weeks instead of once a month does something special. It barely does. The schedule shaves a tiny sliver. The 13th payment does the heavy lifting. Our calculator proves this by amortizing all three paths period-by-period and showing the bi-weekly and the DIY monthly-plus-1/12 finishing within a hair of each other.

How much could you actually save?

On a typical scenario, switching to the 13-payment rhythm pays the loan off several years early and saves a large chunk of interest. Here’s how the three paths compare conceptually. The dollar figures below are illustrative examples — they come from a $350,000 loan at 6.5% over 30 years, which produces a roughly $2,212 monthly payment. Your own numbers will differ:

| Path | What you pay | Payoff effect | Cost |

|---|---|---|---|

| Standard monthly | $2,212 on the 1st | Full 30-year term | $0 extra |

| True bi-weekly | $1,106 every other Friday | Debt-free ~5–6 years sooner | $0 — or a lender fee, if enrolled |

| Fee-free DIY | $2,212 + ~$184 to principal/mo | Captures ~97% of the bi-weekly benefit | $0 |

Read the bottom row carefully. Adding roughly $184 a month to principal — that’s the payment divided by 12 — gets you about 97% of everything the bi-weekly program delivers, with no enrollment, no fee, and full control. The calculator computes this DIY savings and prints it as a percentage of the bi-weekly benefit so you can see precisely how little you’d be paying a program for.

So is the lender’s bi-weekly program a rip-off?

Not always — but you should know what you’re buying. The value a paid program adds is automation and discipline, not math. If a third-party service charges a setup fee plus a per-payment processing fee to “split” your payment, you’re paying for a calendar reminder. Before you enroll, confirm three things:

- Does the extra actually hit principal? Some programs hold your half-payments and only apply them monthly, which kills the early-paydown advantage entirely.

- Are there fees? Enrollment fees and per-payment charges eat into — or erase — the benefit you came for.

- Is there a prepayment penalty? Rare on modern mortgages, but always worth checking before you accelerate.

Our calculator flags this anti-fee guidance directly. The whole point is to show you that you can do the same thing yourself, for free, by setting up an automatic extra principal payment with your servicer.

How do I set up the free DIY version?

Take your normal monthly payment, divide it by 12, and add that amount to principal every month. On a $2,212 payment that’s about $184. Most servicers let you schedule a recurring extra principal payment online — label it clearly as “principal only” so it isn’t applied to next month’s payment or held in suspense.

The suggested extra is exactly what the bi-weekly payment calculator hands you: payment ÷ 12. It also draws a balance-race chart so you can watch the DIY line track the true bi-weekly line almost step for step. Want to see your own loan’s three-way race? Try the bi-weekly calculator and compare the paths side by side.

Does this work at any interest rate?

The lever weakens as your rate drops. The bi-weekly advantage exists because you’re avoiding future interest — so the more interest there is to avoid, the bigger the payoff. At a higher rate, an extra payment a year is powerful. As the rate approaches 0%, the savings collapse toward nothing, because there’s almost no interest left to dodge. The calculator lets you test your own rate (it accepts rates from 0% to 20%) so you can see exactly how much the bi-weekly trick is worth at your number rather than someone’s generic example.

This is also why the bi-weekly trick pairs naturally with other payoff decisions. If you’re weighing whether to throw cash at the mortgage at all, compare it against investing the same money, or check your true cost of debt across multiple loans. You can explore all of those on the 719 Lending Calculate hub.

The bottom line

The schedule isn’t the magic — the 13th payment is. A true bi-weekly plan and a free monthly-plus-1/12 plan land within roughly 3% of each other, so before you pay for a bi-weekly program, make sure you’re buying convenience and not just renting math you already own. Plug in your balance, rate, and term, see your estimated interest saved and your new payoff date, and grab the exact extra amount to send to principal. Run your numbers on the bi-weekly calculator now.

Calculator results are estimates for educational purposes and will vary with your actual loan terms.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Frequently asked questions

Do bi-weekly mortgage payments really save money? Yes, but not because of the every-other-week timing. Paying half your monthly amount every two weeks produces 26 half-payments a year, which equals 13 full payments instead of 12. That one extra payment goes to principal and can shave roughly five to six years and a large amount of interest off a typical 30-year loan. The schedule itself adds only a tiny sliver. Exact savings are estimates that depend on your loan.

Should I pay my lender's fee to enroll in a bi-weekly program? Usually no. You can replicate about 97% of the benefit for free by adding 1/12 of your monthly payment to principal each month. A paid program mainly buys automation. Before enrolling, confirm the extra actually hits principal each period, check for setup or per-payment fees, and verify there's no prepayment penalty.

How do I do the bi-weekly trick for free? Divide your monthly payment by 12 and add that amount to principal every month — on a $2,212 payment that's about $184. Schedule it with your servicer as a recurring principal-only payment so it isn't applied to next month's bill or held in suspense. The calculator gives you the exact suggested extra for your loan.

Does the bi-weekly strategy still help at a low interest rate? Less so. The savings come from avoiding future interest, so the lower your rate, the smaller the benefit. As the rate approaches 0%, the advantage collapses toward nothing because there's almost no interest left to avoid. The calculator lets you enter any rate from 0% to 20% so you can see the effect on your own loan.

Is the bi-weekly calculator's result a quote or guarantee? No. The calculator produces estimates based on the balance, rate, and term you enter, at a single fixed rate across all three paths. Your actual results depend on your real loan terms, servicer behavior, and how consistently you make extra payments. It is educational and is not a commitment to lend.

Related Posts