On a construction loan, your money is not handed over all at once. It is placed in an escrow (or “draw”) account at closing and released in stages — called draws — as each phase of the build is finished and verified. A typical build sees a handful of draws (for example, foundation, framing, mechanicals, and a final draw), each one released only after an inspection confirms the work is done and, on government-backed loans, after you sign off in writing. You generally pay interest only on the money that has actually been disbursed, and a contingency reserve stands by to cover overruns.

If you are financing a build in El Paso County — whether that is a custom home on acreage out toward Black Forest or Falcon, or a production home in a newer Colorado Springs subdivision near Fort Carson — understanding how draws and inspections work is the difference between a build that flows and one that stalls. This guide walks through the mechanics generally, then the agency-specific touches for FHA, VA, USDA, and conventional (Fannie Mae and Freddie Mac) construction financing, verified against each agency’s own rulebook.

Why construction loan funds are released in draws instead of all at once

A finished-home mortgage funds in a single lump sum at the closing table, because the collateral — the house — already exists. A construction loan is different: at closing, the home is still a set of plans and a bare lot. The lender cannot hand a builder the full loan amount up front, because there is nothing built yet to secure it, and no incentive for the work to finish on schedule.

So the loan proceeds are placed into a controlled escrow account at closing. Some funds are disbursed immediately to cover the land purchase (or pay off the lot balance), and the remainder sits in escrow to be released during construction. Fannie Mae’s Selling Guide is explicit that in a single-closing construction-to-permanent loan, “the lender will be responsible for managing the disbursement of the loan proceeds to the builder, contractor, or other authorized suppliers.” The Department of Veterans Affairs calls this remaining balance a “Loan in Process (LIP) account, or a Draw account,” and states plainly that “these funds are paid out to the builder during construction.”

The practical upshot: you never control the construction money directly. The lender does, and it releases each tranche only as the builder earns it. This protects you, the lender, and — on government-backed loans — the taxpayer guaranteeing the loan. If you are still deciding whether a single loan or two separate loans fits your build, our explainer on the one-time-close vs. two-time-close construction loan structures compares the trade-offs.

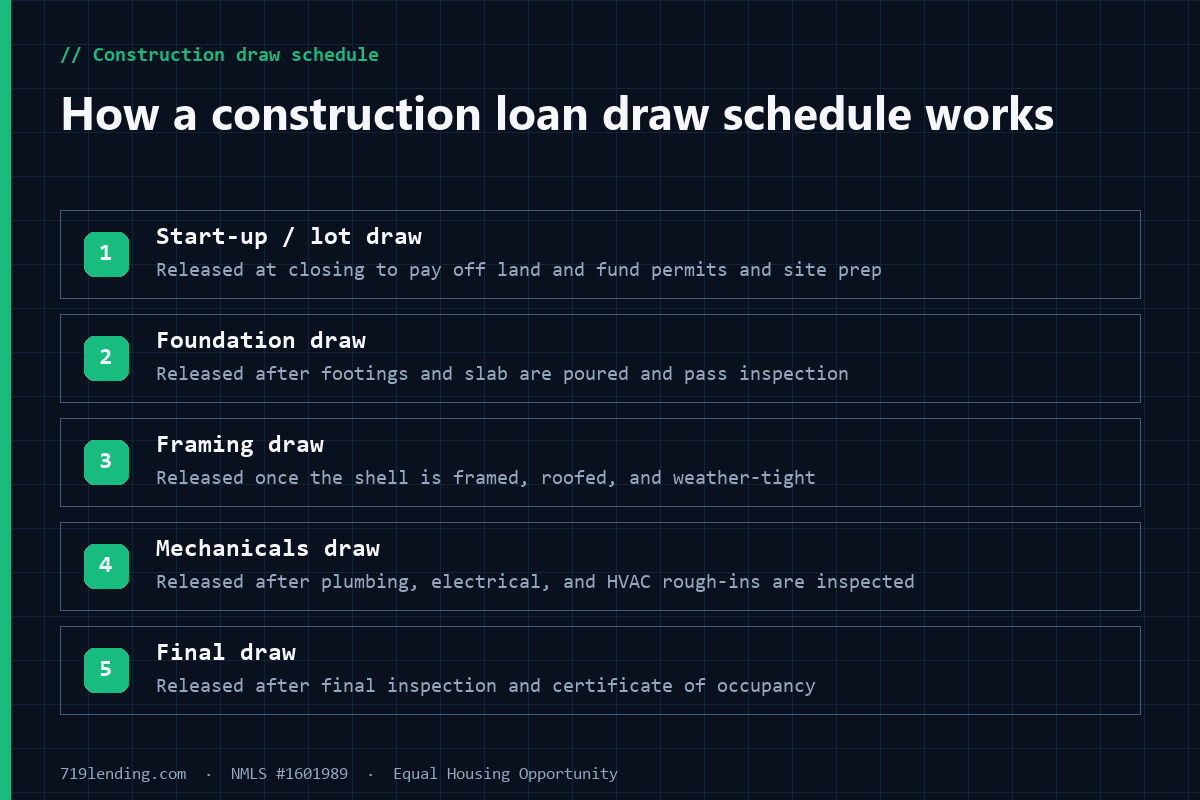

A typical draw schedule releases funds in stages as each inspected milestone is completed.

How a typical construction loan draw schedule works

Before construction begins, the lender and the general contractor agree on a draw schedule — a written plan that ties each release of money to a defined stage of completion. The number of draws varies by lender and by the complexity of the build, but a common structure releases funds at these milestones:

Start-up / lot draw. Released at or near closing to pay off the land and fund permits, site prep, and mobilization.

Foundation. Released once footings, foundation, and slab are poured and pass inspection.

Framing (dried-in). Released when the structure is framed, roofed, and the shell is weather-tight.

Mechanicals / rough-in. Released after plumbing, electrical, and HVAC rough-ins are installed and inspected.

Final draw. Released after the final inspection and, typically, the certificate of occupancy — when the home is 100 percent complete and move-in ready.

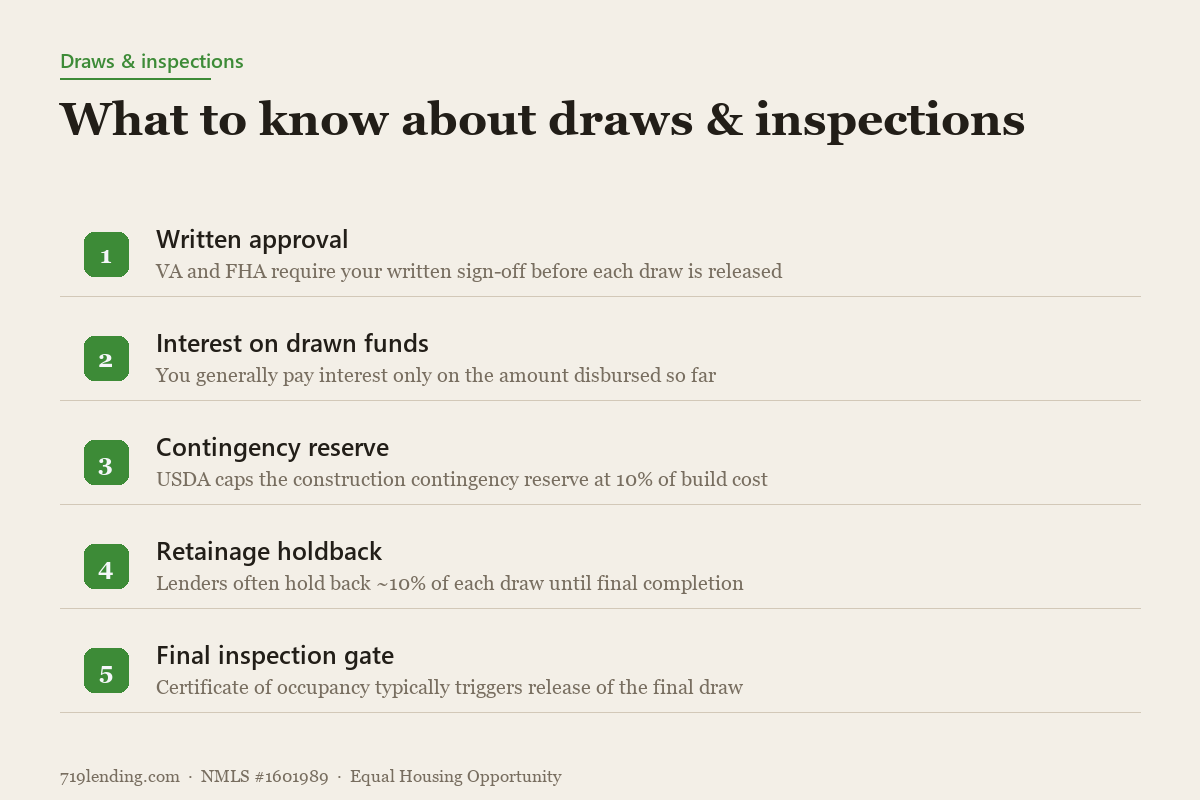

Each draw is triggered the same way: the builder requests funds for completed work, an inspection (or lender-ordered progress review) confirms the stage is genuinely done, and only then are the funds released. The VA is direct that on its loans “the lender must obtain written approval from the borrower before each disbursement, or draw payment is provided to the builder” — so the veteran signs off on each release. FHA follows the same principle: the mortgagee must obtain the borrower’s written authorization for each draw before disbursing funds to the contractor. Because the draw request, inspection, and sign-off all have to line up, a poorly sequenced schedule is one of the most common ways a build loses momentum.

What inspections verify at each draw

A draw inspection is not the same as a home inspection you would order when buying a resale house. It is a progress inspection: an independent inspector or the lender’s representative visits the site and confirms that the work claimed on the builder’s draw request has actually been completed to the plans. On many builds, local building-department inspections (foundation, framing, and final) do double duty. The VA, for instance, will accept a certificate of occupancy as evidence that the local authority performed the required foundation, framing, and final inspections and that construction was satisfactorily completed. Lenders often layer their own progress inspection on top before cutting a check.

One nuance worth knowing: the VA itself stopped performing compliance inspections on new construction back in February 2006, relying instead on local building inspections plus one- and ten-year construction warranties. That reliance on local inspectors is exactly why your builder must hold valid El Paso County or City of Colorado Springs permits and pass Pikes Peak Regional Building Department inspections — those are the checkpoints your draws hinge on. For a stage-by-stage look at how long each milestone takes, see our construction loan timeline.

Five things that govern how and when your construction money is released.

How interest works during construction

Here is a feature that surprises many first-time builders: during the construction phase, you generally pay interest only on the amount disbursed so far — not on the full loan amount. If your loan is approved for $450,000 but only $120,000 has been drawn to complete the foundation and framing, interest accrues on that $120,000, not the whole $450,000. As each draw is released, the outstanding balance climbs, and so does the interest payment. This is why early payments feel small and later ones grow.

Lenders handle those construction-period interest payments in one of two common ways:

Interest paid as you go. You (or, on some structures, the builder) pay the interest-only bill each month as draws accumulate.

Interest reserve. An amount is financed into the loan at closing to cover the projected construction-period interest, so you make no out-of-pocket interest payments during the build. The VA expressly lists an “interest reserve if not included in the contract to build” among the costs that can be built into a VA construction loan.

On a one-time-close construction-to-permanent loan, you typically begin making regular principal-and-interest payments only after construction is complete and the loan converts to its permanent terms. To see how these interest structures feed into your quoted rate, review how construction loan rates are set and locked.

Contingency reserves, retainage, and the final draw

No build goes exactly to plan. A rock ledge appears where the footings should go; a material price jumps; you decide to upgrade the kitchen. That is what a contingency reserve is for — a cushion built into the loan to absorb change orders and cost overruns without derailing financing.

The size of that cushion is where agency rules bite. USDA’s Rural Development handbook (HB-1-3555, Chapter 12) caps the construction contingency reserve at 10 percent of the cost of construction, and requires that any leftover contingency funds be applied as a principal curtailment once the home is finished — so an unused cushion pays down your loan rather than disappearing. The VA, by contrast, treats contingency funds as something “to be negotiated between the borrower and builder.” Conventional programs set their reserve requirements through the lender and investor guidelines. The common thread: figures here are general — confirm current terms with your lender, because they move.

Retainage is a related safeguard. Lenders (and many construction contracts) hold back a percentage of each draw — often around 10 percent — until the project is fully complete and signed off. That withheld money is the lender’s leverage to ensure the builder finishes punch-list items rather than walking away at 95 percent done.

The final draw is the last piece. It is released only after the final inspection confirms the home is complete and, in most cases, after the local authority issues a certificate of occupancy. The VA requires that all its minimum property requirements be met “prior to issuance of the Loan Guaranty Certificate, and the final inspection/certificate of occupancy,” and that a clear final compliance inspection be received before the guaranty is issued. In a one-time-close conventional loan, Fannie Mae will not even purchase the loan “until the construction is completed and the terms of the construction loan have converted to the permanent financing.” In other words, the final inspection is the gate that turns a construction loan into a permanent mortgage. For the full picture of what underwriters check before you ever break ground, see our construction loan requirements guide.

How draws and inspections differ by loan program

The core mechanics — escrow at closing, draws tied to inspected milestones, interest on disbursed funds, a final draw at completion — hold across programs. But the details differ, and the differences are set by each agency’s rulebook:

Program

Draw & inspection touch points

Reserve / interest notes

FHA

Proceeds escrowed at closing, disbursed as construction progresses; mortgagee must obtain borrower’s written authorization for each draw.

LIP / draw account; lender must get the veteran’s written approval before each draw; foundation, framing, and final inspections; final inspection at 100% complete.

Interest reserve and contingency reserve allowable; contingency negotiated between borrower and builder. Builder ID no longer required (rescinded March 31, 2025).

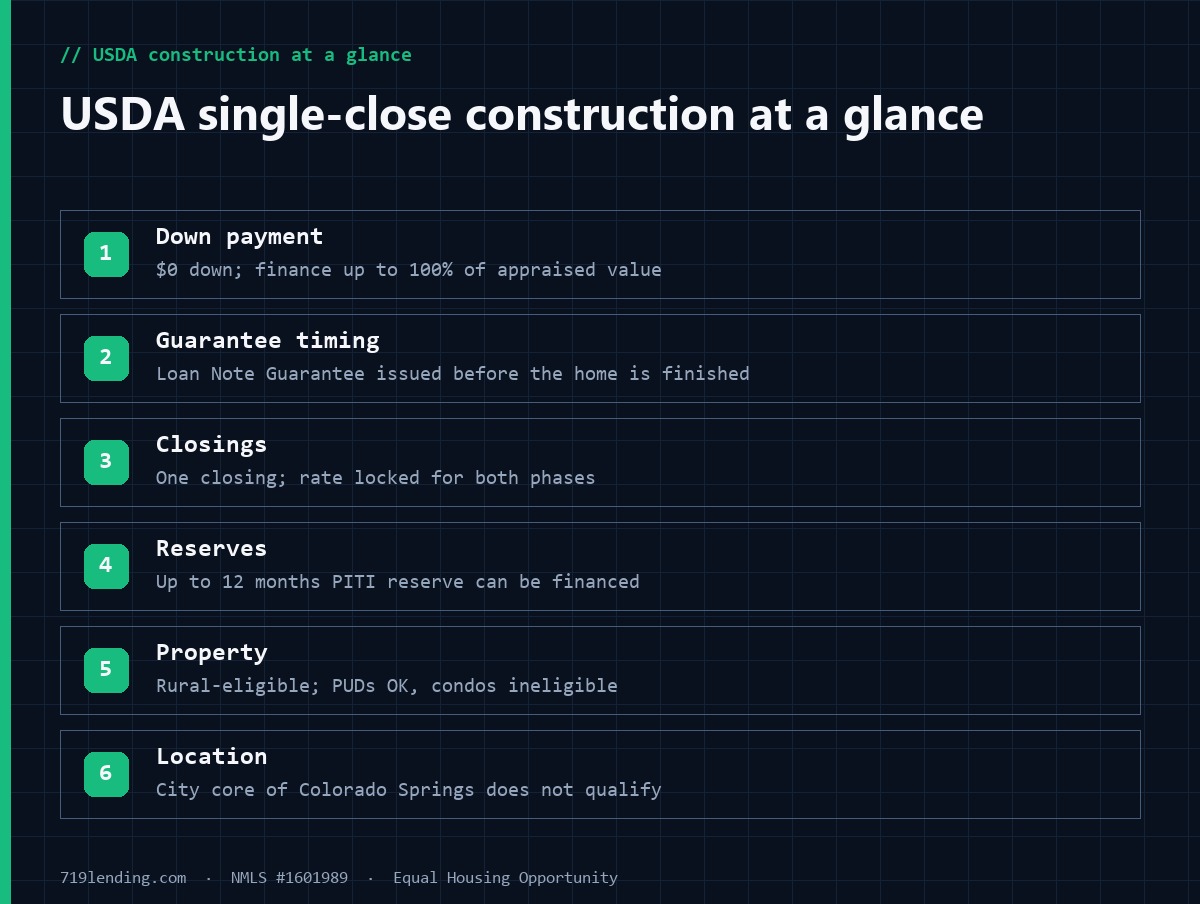

USDA

Single-close combination construction-to-permanent; draws with inspections; principal curtailment of unused funds at completion.

Construction contingency reserve capped at 10% of construction cost (HB-1-3555, Ch. 12).

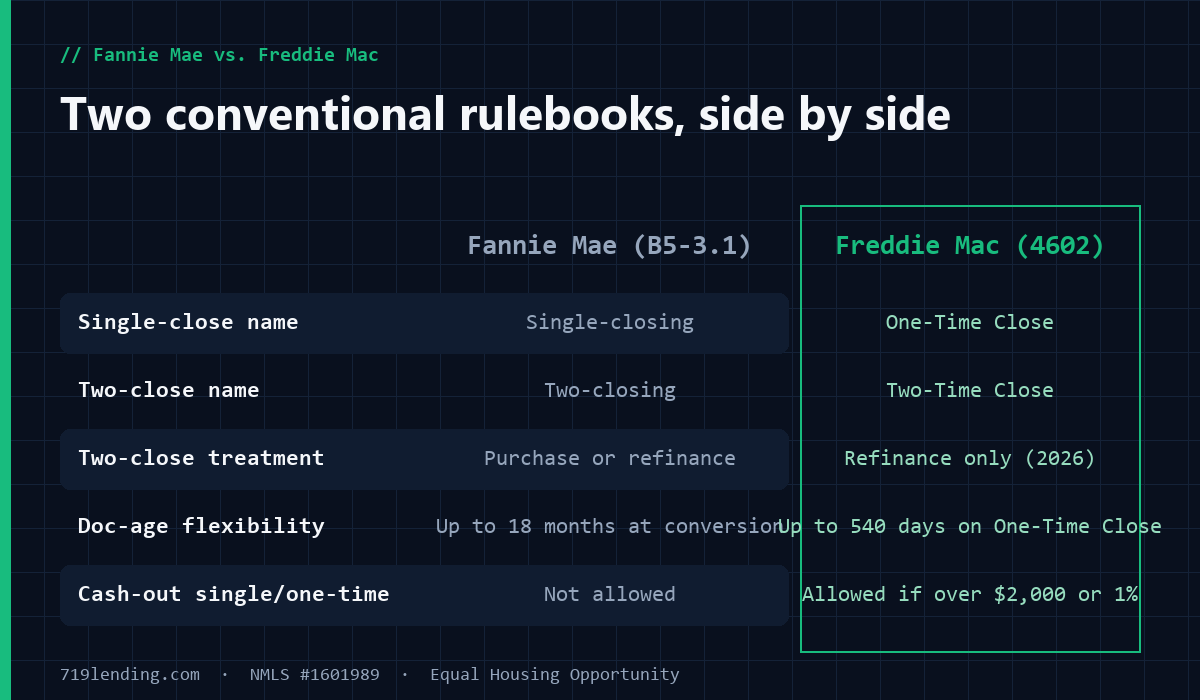

Conventional

Lender manages disbursement to builder/contractor; loan converts to permanent on completion; not purchasable by Fannie until construction is complete.

Two-time-close permanent financing is classified as a refinance under Freddie Mac Guide 4602.3 for applications dated on or after February 4, 2026.

Our take: the single most overlooked document in a construction loan is the draw schedule. Borrowers scrutinize the interest rate and the loan amount, then skim past the schedule that governs whether their builder gets paid on time. Do the opposite. A draw schedule with too few milestones can leave your builder fronting tens of thousands of dollars in labor and materials for weeks, which strains subcontractors and stalls the site. A schedule with unrealistic completion triggers invites disputes at inspection time.

Before you sign, walk the schedule with your builder and confirm three things: that each draw releases enough cash to cover the work in that phase, that the inspection trigger for each draw is something the builder can objectively demonstrate, and that the retainage holdback is one everyone can live with. Delays between draws do not just inconvenience you — they slow the builder, and a slowed builder can miss the window before your rate lock or interest reserve runs thin. This is exactly the kind of thing a broker earns their keep on. If you want a second set of eyes, a mortgage broker in Colorado Springs can compare draw structures across lenders before you commit.

Frequently asked questions

How many draws does a typical construction loan have? It varies by lender and build complexity, but a common structure uses a handful of draws tied to milestones — for example a start-up/lot draw, foundation, framing, mechanicals, and a final draw at completion. Your lender and builder set the exact number and triggers in the draw schedule before construction starts.

Do I have to approve each draw before the builder gets paid? On government-backed loans, yes. The VA requires the lender to obtain the borrower’s written approval before each disbursement to the builder, and FHA requires the mortgagee to obtain the borrower’s written authorization for each draw. Even on conventional loans, the lender controls disbursement and typically ties each release to verified, inspected progress.

Do I pay interest on the full loan amount during construction? Generally no. You typically pay interest only on the amount disbursed so far, so payments start small and grow as draws accumulate. Some loans finance an interest reserve into the loan to cover construction-period interest, so you make no out-of-pocket interest payments during the build. Terms are general — confirm current with your lender.

What is a contingency reserve and how big is it? A contingency reserve is a cushion built into the loan to cover change orders and cost overruns. USDA caps its construction contingency reserve at 10 percent of the cost of construction and applies any unused funds as a principal curtailment at completion. The VA leaves contingency funds to be negotiated between borrower and builder. Confirm your program’s specific reserve rules with your lender.

What triggers the final draw? The final draw is released after the final inspection confirms the home is complete, typically once the local authority issues a certificate of occupancy. On VA loans, a clear final compliance inspection must be received before the guaranty issues; on conventional one-time-close loans, the loan converts to permanent financing at completion and cannot be sold to Fannie Mae until construction is finished.

Who inspects the work before each draw is released? Usually an independent inspector or the lender’s representative confirms the stage is complete, and local building-department inspections (foundation, framing, final) often satisfy part of the requirement. The VA stopped performing its own new-construction compliance inspections in 2006 and now relies on local inspections plus construction warranties, which is why valid local permits and passing inspections matter to your draw releases.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with or endorsed by the FHA, VA, USDA, or any government agency. Loan figures and program terms in this article are general — confirm current details with your lender. Last updated: July 2026.

How conventional construction-to-permanent loans work under Fannie Mae (Selling Guide B5-3.1) and Freddie Mac (Guide 4602), with 2026 rule changes, for Colorado Springs builders.

USDA single-close construction loans let you build a rural Colorado home with $0 down and one closing. See the guarantee timing, builder rules, reserves, and El Paso County eligibility.

How VA construction loans let eligible Colorado Springs veterans build a home with $0 down and no monthly mortgage insurance. One-time close vs two-time close, draws, funding fee, and the 2025 builder-ID change explained.