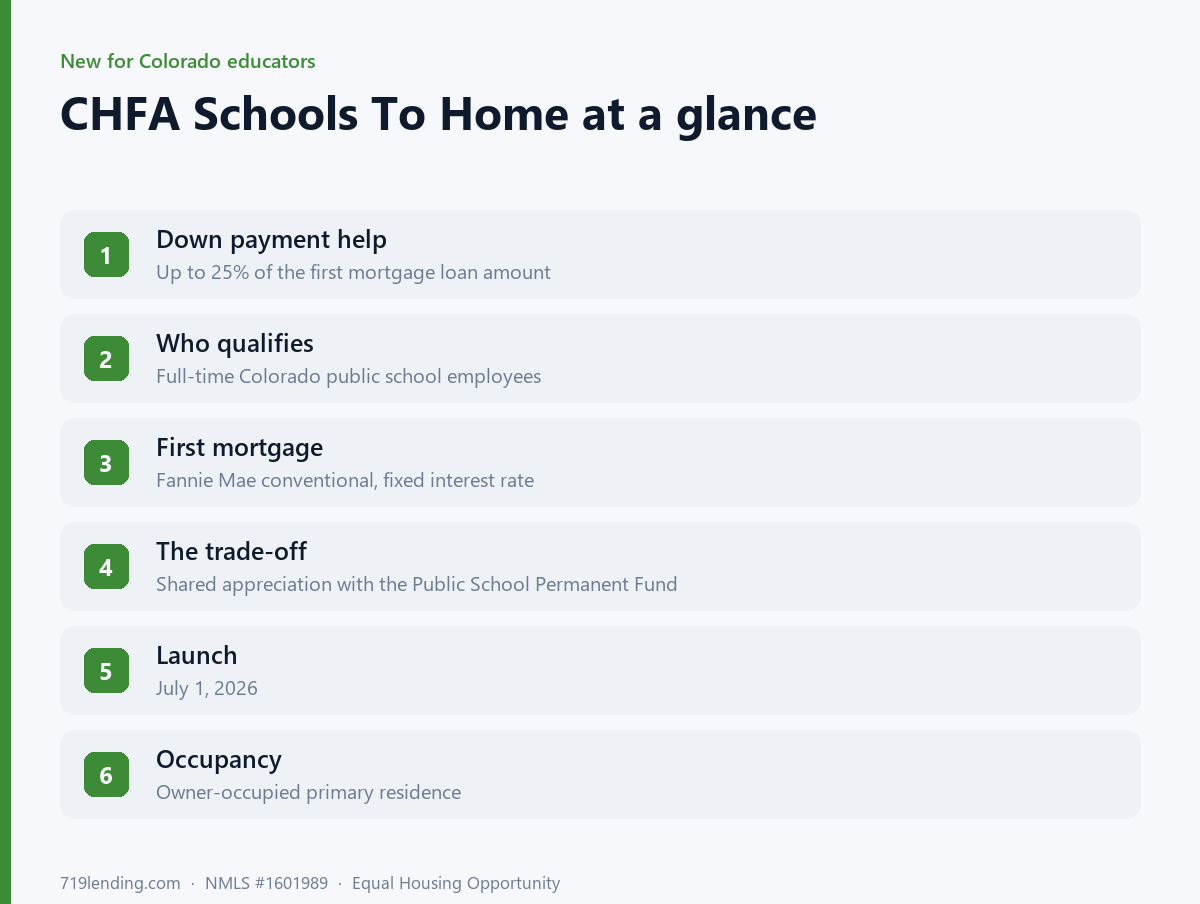

Starting in July 1, 2026, Colorado public school employees have a powerful new path to homeownership: the CHFA Schools To Home program offers up to 25% of your first mortgage loan amount in down payment assistance. It is a shared-appreciation program, meaning you repay the assistance plus a share of your home’s future appreciation when you sell, refinance, or pay off the loan.

If you teach, drive a bus, run the front office, keep the buildings clean, or serve lunch at a Colorado public school, this is genuine, community-minded news. The Colorado General Assembly designated the Colorado Housing and Finance Authority (CHFA) to build and manage this program, and it is funded by an investment from the Public School Permanent Fund (PSPF). The goal is simple and worthwhile: help the people who keep our schools running buy homes in the communities where they work.

Here in the Pikes Peak region, that could mean a paraprofessional in Colorado Springs School District 11, a bus driver in Falcon District 49, a front-office administrator in Academy District 20, or a custodian in Fountain-Fort Carson, Harrison, or Widefield finally getting over the down payment hurdle. Below is a straight, no-hype breakdown of how Schools To Home works, who qualifies, and how the shared-appreciation piece really operates, because being clear about the trade-offs is how you make a smart decision.

CHFA Schools To Home launches in July 2026 (general, confirm current with CHFA and your loan officer).

CHFA Schools To Home at a glance

Schools To Home is built from three pieces that work together. Understanding all three is the key to understanding the program:

A fixed-interest-rate first mortgage. This is a Fannie Mae conventional loan, generally underwritten through Desktop Underwriter (DU). Per CHFA, restrictions and a higher interest rate apply on the 30-year fixed first mortgage — that higher rate is part of how the assistance is funded. Confirm the current underwriting requirements with CHFA and your loan officer (general — confirm current).

Down payment and/or closing-cost assistance of up to 25% of the first mortgage. This comes as a second mortgage loan — for example, on a $350,000 first mortgage, 25% would be about $87,500 in assistance. That is an unusually large amount of help compared with most down payment assistance.

Shared appreciation. In exchange for that larger assistance, you share a percentage of your home’s future appreciation with the Public School Permanent Fund. This is the trade-off that makes the up-to-25% figure possible, and we explain it plainly further down.

The assistance is designed for an owner-occupied primary residence, and it launches in July 1, 2026 (general — confirm current).

Who counts as a public school employee

This is the part people most often get wrong, so read it carefully: Schools To Home is not limited to classroom teachers. It is open to any individual classified as a full-time employee by an eligible Colorado public education employer. That includes, but is not limited to:

Teachers and instructional staff

Paraprofessionals and support staff

Administrators and front-office employees

Bus drivers and transportation staff

Cafeteria and nutrition-services workers

Custodial and maintenance staff

Eligible employers include a preK–12 Colorado public school, a school district, a charter school, an institute charter school, a board of cooperative educational services (BOCES), or an innovation zone. If more than one borrower is on the loan, only one of them needs to be the full-time public school employee (general — confirm current). You can verify whether a school or district qualifies through the Colorado Department of Education’s SchoolView tool, and your loan officer can help you confirm your employer is on the list.

How shared appreciation actually works

Here is the honest version, because you deserve the full picture. The down payment assistance in Schools To Home is essentially an investment by the Public School Permanent Fund in your home. It is not a grant and it is not free money.

In plain English, the second mortgage (your assistance) and the shared-appreciation payment are typically deferred — you generally do not make monthly payments on them while you live in the home. Instead, repayment comes due at the end of the loan term or at an earlier triggering event, such as paying off the first mortgage, selling the home, refinancing, or the home no longer being your primary residence. At that point you repay the assistance amount plus an agreed-upon share of the appreciation your home gained (general — confirm current).

Why is this a fair deal for many buyers? Because it swaps a large obstacle today (the down payment) for a shared upside later. You get into a home you might not otherwise afford, you build stability in your community, and the fund shares in the growth it helped make possible. The right way to evaluate it is to run the numbers with a loan officer on your specific price range and time horizon — that is exactly the kind of side-by-side comparison we do every day.

Schools To Home offers a far larger assistance amount in exchange for sharing future appreciation (general, confirm current).

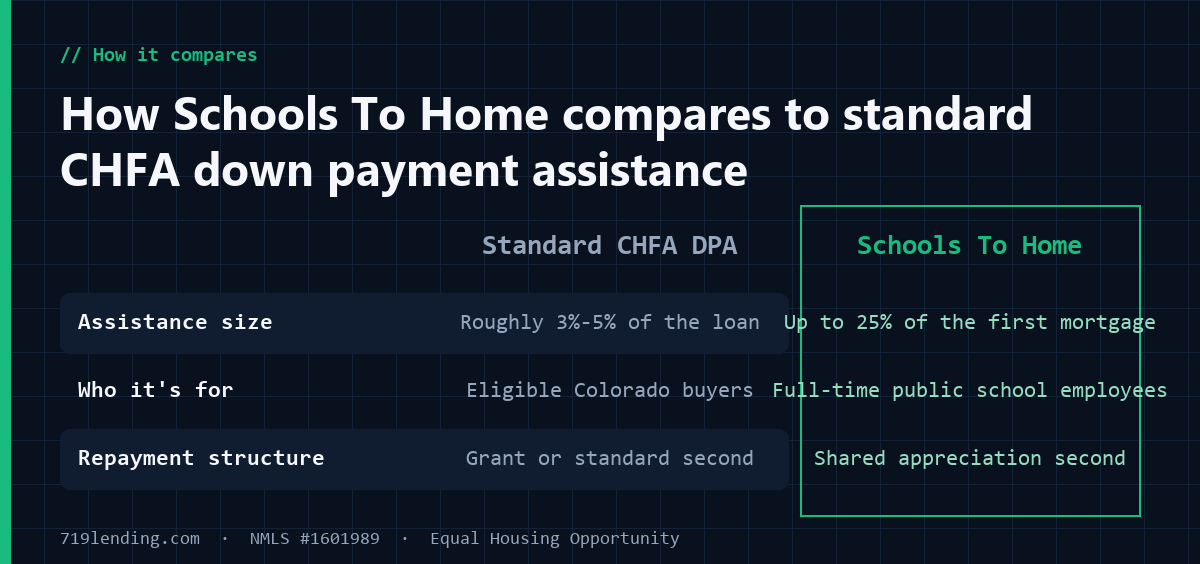

How Schools To Home compares to standard CHFA down payment assistance

CHFA already offers well-known down payment assistance, generally in the range of a few percent of the loan as a grant or second mortgage. Schools To Home is different in scale and structure. The table below frames it accurately (all figures general — confirm current with CHFA and your loan officer):

Feature

Standard CHFA DPA

Schools To Home

Assistance size

Roughly 3%–5% of the loan

Up to 25% of the first mortgage

Who it’s for

Eligible Colorado buyers

Full-time public school employees

Repayment structure

Grant or standard second mortgage

Shared appreciation second mortgage

The up-to-25% figure is the headline, and it is real — but the shared-appreciation exchange is the reason it can be that large. Neither approach is universally "better." A buyer focused on the smallest long-term cost might prefer a standard grant; a buyer who simply cannot clear the down payment today may find Schools To Home is what makes the purchase possible at all.

Requirements to know before you apply

Because Schools To Home rides on CHFA’s conventional first mortgage, several familiar CHFA-style requirements apply. Confirm each with CHFA and your loan officer, since this is a brand-new program and details can change:

Credit score: CHFA programs generally require a mid-credit score around 620 (general — confirm current).

Homebuyer education: Borrowers are expected to complete an "Understanding Your Financial Commitment" course and a CHFA-approved homebuyer education class before closing.

Occupancy: The home must be your owner-occupied primary residence.

Loan type: Fannie Mae conventional, generally underwritten through Desktop Underwriter (DU) — confirm the current underwriting path with CHFA and your loan officer.

Income and loan limits: CHFA programs carry county-based income limits, and total loan amounts are capped by loan-type limits. Confirm the current income and price limits for your county with CHFA (general — confirm current).

Because this is a first-week program, some operational details are still being finalized. Your loan officer will handle the current Schools To Home program forms and paperwork with you.

Do you have to be a first-time buyer?

Schools To Home is aimed at helping public school employees live where they work. The legislation that created the program references first-time homebuyers, so first-time status may factor into eligibility alongside the full-time public school employee requirement. Whether you are buying your very first home or returning to homeownership, the smartest move is to confirm your specific situation with CHFA and a loan officer rather than assuming you are in or out. That is a five-minute conversation that can save you a lot of guessing.

How 719 Lending helps you explore Schools To Home

719 Lending is a Colorado Springs mortgage broker serving El Paso County and the Fort Carson area. To be clear about our role: we do not originate or administer the CHFA Schools To Home program — CHFA does. What we do is help you navigate and explore CHFA and down payment assistance options, compare Schools To Home against other paths, and figure out what actually fits your budget, your timeline, and your goals.

For a public school employee, the questions that matter are practical: How much house does this put within reach? How does the shared-appreciation math look over the years you plan to stay? Is a standard CHFA down payment assistance program a better fit than Schools To Home for you? Those are exactly the comparisons we walk through together, with real numbers and no pressure.

If you teach, drive a bus, run the front office, or keep the lights on at a Colorado public school, homeownership just got more within reach. Call 719 Lending today to see whether Schools To Home could be a fit and to explore it alongside every other Colorado down payment assistance option on the table. It costs nothing to find out.

Frequently asked questions

Who counts as a public school employee for Schools To Home? Any individual classified as a full-time employee by a preK–12 Colorado public school, school district, charter school, institute charter school, BOCES, or innovation zone. That includes teachers, paraprofessionals, administrators, bus drivers, cafeteria staff, and custodial and maintenance workers — not just educators. If two borrowers are on the loan, only one needs to be the full-time public school employee (general — confirm current).

How much down payment assistance can I get? Up to 25% of your first mortgage loan amount, provided as a second mortgage. That is unusually large compared with standard down payment assistance, which is typically in the 3%–5% range (general — confirm current).

What is shared appreciation, and is this free money? No, it is not free money. The assistance is an investment by the Public School Permanent Fund. When you sell, refinance, pay off the first mortgage, or the home stops being your primary residence, you repay the assistance plus an agreed share of your home’s appreciation. Being clear-eyed about that trade-off is how you decide if it fits (general — confirm current).

Do I have to be a first-time buyer? The program’s enabling legislation references first-time homebuyers, alongside the full-time public school employee requirement. Confirm your specific eligibility with CHFA and your loan officer rather than assuming.

What credit score and education do I need? CHFA programs generally look for a mid-credit score around 620, and you are expected to complete an "Understanding Your Financial Commitment" course plus a CHFA-approved homebuyer education class before closing (general — confirm current).

How do I get started? Contact 719 Lending. We will help you confirm your employer’s eligibility, compare Schools To Home with other Colorado down payment assistance, and walk through the numbers for your situation. We help you explore and navigate CHFA options — CHFA administers the program itself.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, or endorsed by, CHFA or any government agency; program details are subject to change — confirm current terms with CHFA and your loan officer. All figures and terms above are general — confirm current. Last updated: July 1, 2026.