A VA one-time close construction loan lets eligible veterans build a home near Fort Carson with $0 down and a single closing that covers the land, the build, and the permanent mortgage. Here's how it works in El Paso County.

Construction Loan Down Payment: How Much You Need

Most construction loans require 10% to 25% down. Conventional construction-to-permanent loans typically want around 20%, FHA can go as low as 3.5%, and VA construction loans allow $0 down for eligible borrowers. If you already own the lot, your land equity can count toward — and sometimes fully cover — the down payment.

Building a home in El Paso County is a different animal than buying an existing one. The lender isn’t just underwriting you — it’s underwriting a house that doesn’t exist yet, plus the builder, the budget, and the timeline. That risk is why down payment math on construction loans looks different from a normal purchase. Below is how it actually works, what land equity does for you, and the typical ranges by program.

How much do you need down on a construction loan?

Plan on 10% to 25% of total project cost on a conventional construction loan, with 20% being the common target. “Total project cost” usually means the land plus the cost to build (the “cost to complete”), and the lender lends against the lower of total cost or the appraised future value of the finished home. The riskier the file — lower credit, tighter builder, custom one-off design — the closer to 25% a lender will push.

The key mental shift: on a purchase, your down payment is a percentage of the sale price. On a construction loan, it’s a percentage of everything it takes to build — land acquisition, materials, labor, permits, and the builder’s contingency. That number is often larger than buyers expect, which is exactly why land equity matters so much.

How does land equity count toward the down payment?

If you already own your lot — especially free and clear — that equity counts as part of (or all of) your required down payment. Lenders treat the land’s appraised value as cash you’ve already put into the deal. So if you own a $120,000 lot outright in Black Forest and you’re building a $480,000 home, your total project cost is roughly $600,000. A 20% down requirement is $120,000 — which your land equity already covers. In that scenario you may bring little or no additional cash to close.

A few things that decide how much your land actually counts for:

- Appraised value, not what you paid. If your lot has appreciated since you bought it, the higher current value generally works in your favor.

- How long you’ve owned it. Under FHA rules, land you’ve owned more than six months, or received as a gift, counts at full appraised value; land held six months or less counts at the lesser of your cost or its appraised value. Some lenders add longer seasoning overlays, so confirm with yours.

- Any loan against the land. If you still owe on a lot loan, only your equity (value minus the balance) counts — and that lot loan typically gets paid off and rolled into the construction loan.

This is the single biggest lever for buyers in places like Monument, Falcon, and Peyton, where families often buy acreage first and build later. The land you’ve been sitting on can be your down payment.

What are the down payment ranges by loan type?

Different programs treat construction very differently. Here’s how the common paths compare for a Colorado Springs build. The dollar example assumes a $600,000 total project cost. These are general ranges, not quotes.

| Loan type | Typical down payment | On a $600K project | Best fit |

|---|---|---|---|

| Conventional construction-to-permanent | ~20% (10-25% range) | ~$120,000 | Strong credit, has land or cash |

| FHA one-time-close construction | 3.5% | ~$21,000 | Lower down payment, flexible credit |

| VA construction loan | $0 down | $0 | Eligible veterans / active duty |

| USDA construction (rural areas) | $0 down | $0 | Eligible rural lots outside the city core |

| Jumbo / custom construction | 20-30%+ | $120,000-$180,000+ | High-cost custom builds |

Numbers above are typical ranges, not quotes — every lender sets its own overlays, and your actual requirement depends on credit, the builder, and the appraised future value. Confirm current terms before you budget.

Why is the down payment higher than a regular mortgage?

Because the collateral doesn’t exist yet. With a purchase, the bank can foreclose on a finished, sellable house tomorrow. With construction, the lender is fronting money against a half-framed structure that’s worth far less than the loan until it’s done. To offset that, lenders ask for more skin in the game up front. The down payment is the cushion that protects them if the build stalls, the builder walks, or costs blow past budget.

That’s also why construction lenders scrutinize the builder almost as hard as they scrutinize you — licensing, references, a fixed-price contract, and a realistic draw schedule all factor into how much they’ll require down.

One-time-close vs. two-time-close: does it change the down payment?

The structure matters more for cost and risk than for the down payment percentage itself. A construction-to-permanent (one-time-close) loan wraps the construction phase and the final mortgage into a single closing — you put your down payment in once and the loan converts to a permanent mortgage when the home is finished. A two-time-close uses a short-term construction loan, then you refinance into a permanent mortgage separately, paying two sets of closing costs.

For most El Paso County buyers, the one-time-close is cleaner: one closing, one set of fees, your terms locked once. FHA and VA construction programs are typically one-time-close by design. The down payment percentages above apply either way — what changes is how many times you pay closing costs.

A real Colorado Springs scenario

Say a Fort Carson family owns a $130,000 lot in Falcon free and clear and wants to build a $470,000 home — a $600,000 total project. With a VA construction loan, they may be able to do this at $0 down, with no monthly mortgage insurance, and the land equity simply strengthens the file. With a conventional loan, that same $130,000 of land equity more than covers a 20% ($120,000) requirement, so they’d bring little additional cash. Same land, very different cash-to-close depending on which program fits. That’s the conversation worth having before you pick a builder.

What each loan program requires

The down payment ranges above come straight from how each agency structures a construction-to-permanent loan, and the details differ by program.

- FHA one-time close. FHA’s Construction-to-Permanent program (HUD Handbook 4000.1) combines the interim construction loan and the permanent mortgage into a single closing before construction begins. You must use a licensed general contractor, and land owned more than six months, or received as a gift, counts at full appraised value toward your required investment. See our Colorado FHA loan overview for the basics.

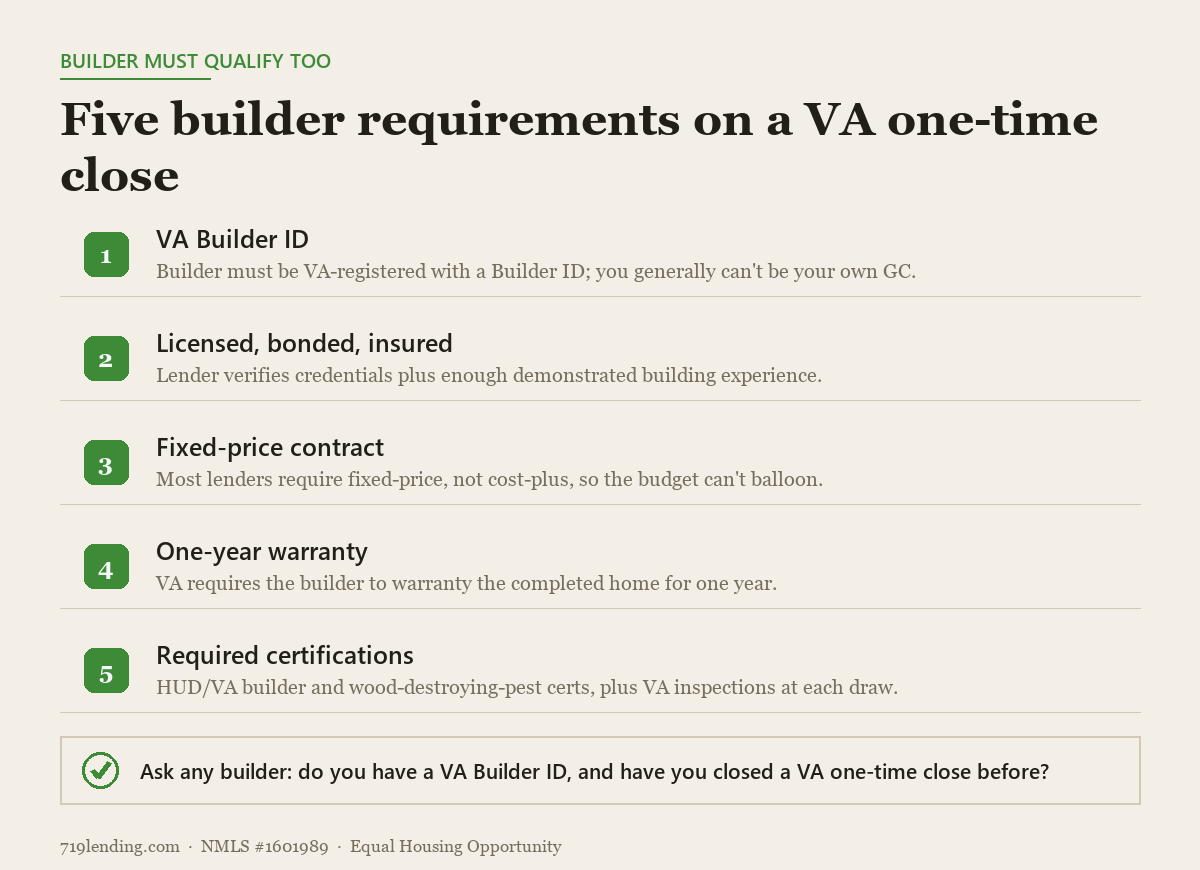

- VA construction. Eligible veterans can build with a VA loan at $0 down and no monthly mortgage insurance, as a one-time or two-time close. The builder must obtain a VA Builder ID before the appraisal’s Notice of Value is issued, and a final VA inspection is required at completion (VA.gov).

- USDA single-close. In eligible rural areas, USDA’s single-close construction loan finances the build with no down payment, but owner-builders are not allowed; you must use an approved, licensed, insured builder with a signed fixed-price contract (USDA Rural Development).

- Conventional (Fannie Mae). Fannie Mae sizes a single-closing construction-to-permanent loan against the lesser of total cost or the “as-completed” appraised value, with the construction period capped at 12 months (18 with extensions), per the Fannie Mae Selling Guide. Compare programs with our Colorado construction loan guide.

Frequently asked questions

Can I use land I already own as my down payment?

Yes. Lenders count your land’s equity (appraised value minus any balance owed) toward the down payment, and if you own the lot free and clear it can cover the requirement entirely. Many lenders use full appraised value if you’ve owned it 12+ months; otherwise they may use your purchase price. Overlays vary by lender.

Is the down payment based on the land price or the build cost?

On total project cost — land plus the cost to build. The lender lends against the lower of total cost or the appraised future value of the finished home, then applies the down payment percentage to that figure.

Do FHA and VA construction loans really have low or no down payment?

Yes, when you qualify. FHA one-time-close construction loans can go as low as 3.5% down, and VA construction loans allow $0 down with no monthly mortgage insurance for eligible veterans and active-duty service members. Both are typically one-time-close structures. Not all applicants will qualify.

Why do construction lenders want more down than a purchase lender?

Because they’re lending against a home that isn’t built yet. The extra down payment is a cushion against the build stalling or going over budget. Lenders also evaluate your builder, contract, and draw schedule as part of setting the requirement.

Does a one-time-close loan reduce my down payment?

No — the structure doesn’t change the down payment percentage, but it changes your costs. A one-time-close wraps construction and permanent financing into a single closing, so you pay closing costs once instead of twice. The down payment ranges by loan type still apply.

Talk to a local broker before you budget your build

The right loan can swing your cash-to-close by tens of thousands of dollars, especially if you already own land in El Paso County. As an independent Colorado Springs mortgage broker, 719 Lending can compare construction programs across multiple lenders and walk you through how your land equity counts. Want to see your options? Reach out for a no-pressure conversation about your build, or explore our other guides on current mortgage rates and first-time buyer programs.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency. Last updated: July 2026.

Related Posts