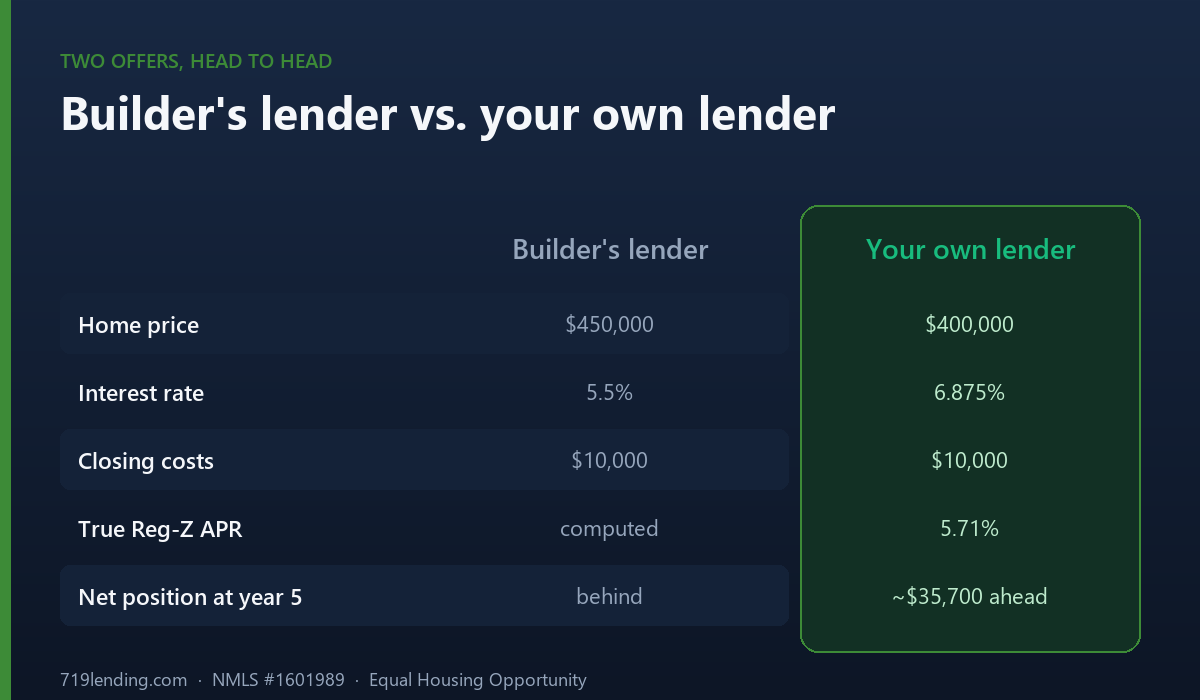

A builder's "preferred lender" dangles a rate the bank can't touch — then quietly funds it with a higher home price. Here's the math that names the winner in dollars, not rate.

How to split a seller concession so you don’t waste a dollar

Last updated: June 30, 2026 — example figures (a $350,000 loan at 6.25% over 30 years, $15,000 in concessions) are illustrative; confirm current rates and terms.

A seller concession is use-it-or-lose-it money. Whatever you don’t apply to real loan costs goes back to the seller — not your pocket. The Concession Optimizer brute-forces every dollar split across closing costs, a temporary buydown, and a permanent rate buydown to find the mix that wastes the least seller money first, then nets the most over how long you actually plan to stay.

Why does the way you split a concession matter so much?

Because the three ways to spend a seller credit are not interchangeable, and one of them can quietly evaporate. The optimizer scores a split on two honest realities most buyers never get told:

- Refundability. Closing-cost credits are the only dollar-for-dollar sure thing. A temporary buydown sits in an escrow account, so the unused portion is credited back to you if you sell or refinance early. A permanent buydown’s value simply evaporates the day you leave — you bought a lower rate for a loan you no longer have.

- Your planned stay. A permanent buydown only “works” if you keep the loan long enough for the monthly savings to repay its upfront cost. As an illustration, spend $7,500 to save $90 a month and you’d need roughly 83 months just to break even — sell at year three and you’d torch most of it.

That’s why a smart split is a math problem, not a gut call. Run yours in the Concession Optimizer and watch the recommendation change as you change your timeline.

How does the optimizer actually find the best split?

It does not guess and it doesn’t take shortcuts. The engine performs a brute-force search of every dollar split across the three buckets — exhaustive, not a greedy “biggest savings first” heuristic that can miss the true winner. For each candidate split it prices the closing-cost credit, the applicable temporary-buydown schedules, and up to three permanent-rate-buydown quotes, then ranks every outcome by two keys in order:

- Least seller money wasted — any dollar that can’t be put to work goes back to the seller, shown in red.

- Biggest net gain over your planned stay — among the splits that waste the least, the one that puts the most back in your pocket wins.

All figures are principal and interest only (P&I) — taxes, insurance, and HOA are not part of the buydown math here.

How does your planned stay change which buydown wins?

It decides whether a permanent buydown even belongs in the running. A permanent buydown has to earn its place against how long you’ll keep the loan, and the optimizer won’t let one look good on paper if your timeline kills it:

- Short stay: permanent buydowns are excluded — there isn’t enough time to recoup their upfront cost, so the optimizer leans on refundable temporary relief plus dollar-for-dollar closing-cost coverage.

- Long stay: a permanent buydown’s lifetime savings get the years they need to stack up past break-even, so permanent quotes are favored.

Each permanent quote also gets an honest per-quote break-even — cost divided by monthly savings — with a clear “works” or “won’t pay off” verdict for your stay. Temporary schedules are guarded too: if a structure would push the effective rate to zero or below in any year, it’s flagged rather than printing fantasy numbers.

What does a result look like?

You get one optimal allocation plus three pure strategies to compare against — a four-way race (max closing, max temp, max permanent). Here’s an illustrative split (these are example figures, not a quote):

| Bucket | Example allocation | What it does |

|---|---|---|

| Closing costs | $5,000 | Dollar-for-dollar, never wasted |

| Permanent buydown | $7,500 | Lowers the note rate for life of loan |

| Temporary buydown | $2,500 | Cuts early-year payments; unused escrow refundable |

| Total credit | $15,000 | Zero wasted, ranked by net gain |

The defaults — a $350,000 loan at 6.25% over 30 years, $15,000 in concessions, $5,000 of closing costs, and a five-year stay — are there so you can see it work, then swap in your own numbers. Alongside the optimized mix you’ll see three comparison cards, a bar chart, the full temporary-buydown menu (1/0, 1/1, 2/1, and 3/2/1 schedules), and per-permanent-quote savings, break-even, and verdict.

Why does the winning split change when I change my timeline?

Because the recommendation flips from temporary to permanent as your stay gets longer — and that’s the whole point. A short stay excludes permanent buydowns entirely and favors refundable temporary relief plus closing-cost coverage. A long stay lets a permanent buydown’s lifetime savings stack up past its break-even, so the optimizer pivots toward it. Change one input — “years to stay” — and the entire allocation can rearrange. That single lever is the difference between a credit that pays off and one that partly vanishes. Browse the full calculator hub if you want to pair this with the standalone Temporary Buydown or other structuring tools.

The bottom line

A seller credit is one of the few negotiating wins where the dollars are already yours to direct — but only if you direct them well. Closing credits are the sure thing, temporary escrow is refundable if you leave early, and permanent value disappears the moment you sell. Let the math decide instead of splitting it by feel. Run your numbers in the Concession Optimizer and find the split that doesn’t waste a dollar.

Calculator results are estimates for educational purposes and depend on the inputs you provide.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Frequently asked questions

What is a seller concession? A seller concession (or seller credit) is money the seller agrees to put toward the buyer's real loan costs — closing costs, a temporary buydown, or a permanent rate buydown. It's use-it-or-lose-it: any portion that can't be applied to legitimate costs goes back to the seller rather than to you, which is why how you split it matters.

Is a permanent buydown always the best use of a seller credit? No. A permanent buydown only pays off if you keep the loan long enough for the monthly savings to recoup its upfront cost, and its value evaporates the day you sell or refinance. The Concession Optimizer treats your planned stay as a gate: a short stay excludes permanent buydowns entirely, while a longer stay lets them compete because their lifetime savings have time to clear break-even.

How does the Concession Optimizer find the best split? It runs a brute-force search of every dollar split across closing costs, a temporary buydown, and a permanent buydown — exhaustive rather than a greedy shortcut. It ranks outcomes by two keys: least seller money wasted first, then biggest net gain over your planned stay. All figures are principal and interest only, and results are estimates based on your inputs.

Which part of a seller credit is actually safe if I sell early? Closing-cost credits are the only dollar-for-dollar sure thing. A temporary buydown sits in escrow, so the unused portion is credited back to you on an early sale or refinance. A permanent buydown's value simply evaporates when you leave, since you bought a lower rate for a loan you no longer hold.

Are the calculator's results a loan offer? No. The Concession Optimizer's results are estimates for educational purposes based on the inputs you enter, and they reflect principal and interest only. They are not a commitment to lend, and not all applicants will qualify.

Related Posts