A seller concession is use-it-or-lose-it money — and the wrong split hands dollars back to the seller. The Concession Optimizer brute-forces every split across closing costs, a temporary buydown, and a permanent rate buydown to find the mix that wastes the least and nets the most over your planned stay.

How much seller concession to ask for (and the % most calculators get wrong)

Last updated: June 30, 2026 — concession caps (FHA 6%, VA 4%, USDA 6%, and LTV-stepped conventional brackets) reflect current agency guidelines; general figures, confirm current with your loan file.

The honest answer: size your seller concession by adding up the real loan costs a credit can legally cover (closing costs, escrows, prepaid interest, points, a buydown), then check that total against your program’s cap as a percentage of purchase price — not loan amount. That one distinction is where most calculators go wrong, and it can make a perfectly legal 6% ask look like it “fails.”

Seller concessions are one of the most powerful — and most fumbled — levers in a purchase offer. Ask for too little and you leave money on the table. Ask for too much, or measure the cap the wrong way, and your offer gets bounced or your lender claws it back at the closing table. The Seller Concessions calculator exists to get this number exactly right. Here’s how the math actually works.

What is a seller concession, really?

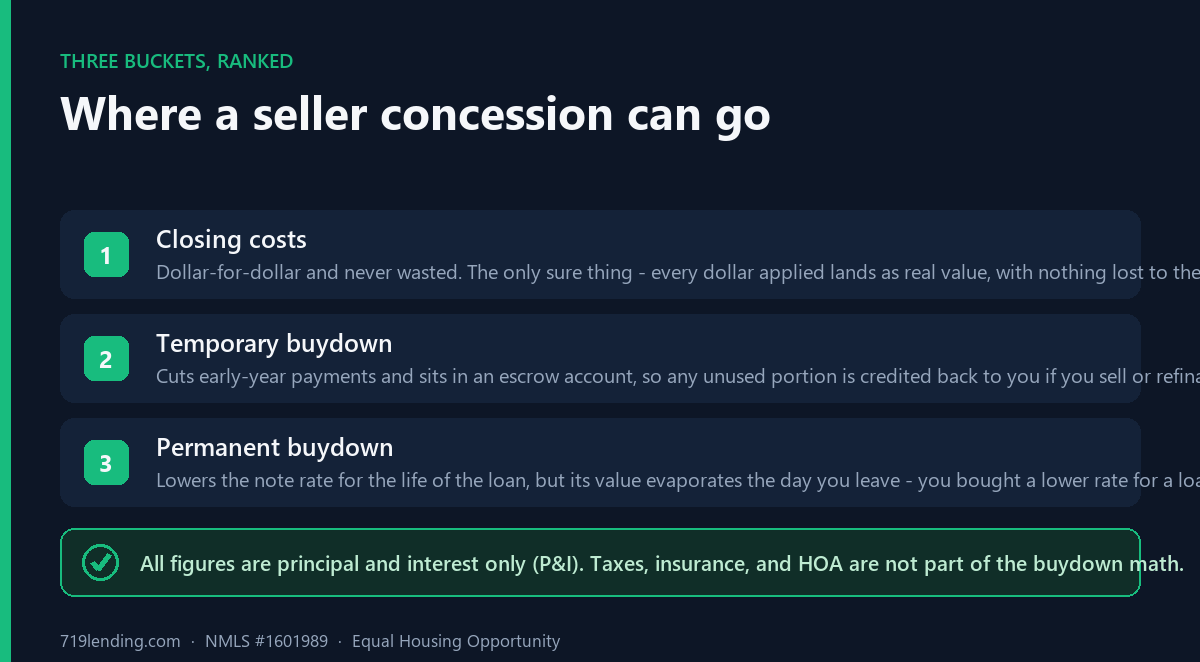

A seller concession (or seller credit) is money the seller agrees to put toward your closing-related costs instead of pocketing it as sale proceeds. It does not go to your down payment, and it can’t be cash back to you. It covers things like closing costs, escrow funding, prepaid interest, discount points, and a temporary buydown.

The tool sizes the credit by summing the real costs a seller credit is allowed to cover:

| Cost component | How it’s estimated |

|---|---|

| Flat closing costs | CO-average ~$4,750 |

| Estimated escrows | 0.8533% of purchase price |

| Prepaid interest | loan × (rate/100)/360 × days from closing to month-end |

| Discount points | Whatever you enter |

| Temporary buydown | Whatever you enter |

| DPA origination (optional) | 1% of purchase price |

Add those up and you have a defensible dollar figure to write into the offer — not a guess. Run your numbers in the Seller Concessions calculator and it itemizes every line for you.

Why do most seller-concession calculators get the cap wrong?

Because they divide by the wrong number. Agency concession caps are expressed as a percentage of the purchase price — technically the lesser of price or appraised value, which is what agencies actually enforce. A lot of legacy tools (including the one this calculator replaced) wrongly divided the concession by the loan amount. That inflates the percentage and over-disqualifies programs that would have been perfectly fine.

Here’s the trap in numbers. Take a $500,000 purchase with a $450,000 loan and a $30,000 concession — a legal 6% of price:

| Basis | Math | Result | Verdict |

|---|---|---|---|

| % of purchase price (correct) | $30,000 / $500,000 | 6.00% | Fits a 6% cap |

| % of loan amount (legacy bug) | $30,000 / $450,000 | 6.67% | Looks like it fails |

(Illustrative example.) Same dollars, two answers. The price-based basis passes; the loan-based basis makes a legal ask look 0.67 points over the line. That difference can cost a buyer thousands by talking them out of a credit they were entitled to. The calculator measures against purchase price and still shows the % of loan figure alongside it, purely for continuity so you can see both.

What are the seller concession limits by loan program?

The cap depends on your program and, for conventional loans, your loan-to-value. The calculator checks your ask against seven agency caps at once and shows a fits/over bar for each:

| Program | Concession cap (% of price) |

|---|---|

| Conventional — 4 LTV brackets | Stepped by LTV bracket |

| FHA | 6% |

| VA | 4% |

| USDA | 6% |

This is why your loan amount still matters: it sets your LTV, which decides which of the four conventional brackets you fall into. The tool reads your LTV bracket automatically and tells you not just whether your ask fits overall, but whether it fits your bracket while still respecting the strictest program.

How do I know if my ask fits?

Enter your purchase price, loan amount, rate, and closing day, then add any discount points, temporary buydown, or DPA toggle. The calculator returns:

- Your total concession ask in dollars

- That ask as a % of price and a % of loan

- Your LTV bracket

- A count of how many of the 7 programs it fits, with a bar per program

- An itemized breakdown of every cost line

- Up to ten guardrail warnings flagging issues before they become offer problems

The closing-day selector matters more than people expect. Prepaid interest is calculated as loan × (rate/100)/360 × the number of days from your closing date to the end of the month. Close early in the month and you prepay nearly a full month of interest; close near month-end and you prepay almost nothing. Moving your closing date can meaningfully change the credit you need.

What outcomes should I expect?

Depending on your inputs, the tool will tell you one of several things:

- The exact dollar concession to write into the offer

- It fits all seven programs — you’re clear no matter the loan

- It fits your LTV bracket but blows the strictest program (useful if you might switch programs)

- It’s over for your bracket — trim the ask or restructure

- You have unused room to add discount points or a buydown and still stay under the cap

- The same dollars fit differently depending on whether you measure against price or loan

That “unused room” outcome is the one savvy buyers chase. If your essential costs come in under the cap, the leftover headroom can buy down your rate — turning a seller credit into a lower monthly payment instead of leaving negotiating room on the table.

Ready to size yours? Try the Seller Concessions calculator and write a number you can defend. It lives alongside our other negotiation and structure tools on the Calculate hub, or talk to a mortgage broker who structures these offers every week. Results are estimates — your actual figures depend on your full file, program, and final rate lock.

Frequently asked questions

Is the seller concession cap based on the loan amount or the purchase price?

The purchase price — technically the lesser of purchase price or appraised value, which is what agencies enforce. Dividing by the loan amount (a common legacy bug) inflates the percentage and can make a legal ask look like it exceeds the cap.

What can a seller concession actually pay for?

Loan-related costs: closing costs, escrow funding, prepaid interest, discount points, and a temporary buydown (plus optional DPA origination). It cannot go toward your down payment or come back to you as cash.

How much can the seller contribute on an FHA, VA, or USDA loan?

The calculator checks seven agency caps as a percentage of price: FHA 6%, VA 4%, USDA 6%, and four conventional brackets that step by LTV. Your loan amount sets your LTV, which decides your conventional bracket.

Why does my closing date change the number?

Prepaid interest is calculated from your closing day to the end of the month: loan × (rate/100)/360 × days remaining. Closing earlier in the month means more prepaid interest, so the credit you need goes up.

Can I use a seller concession to lower my interest rate?

Yes — if your essential costs come in under your cap, the unused room can fund discount points or a temporary buydown. The calculator flags that leftover room so you can put it to work instead of leaving it on the table.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Related Posts