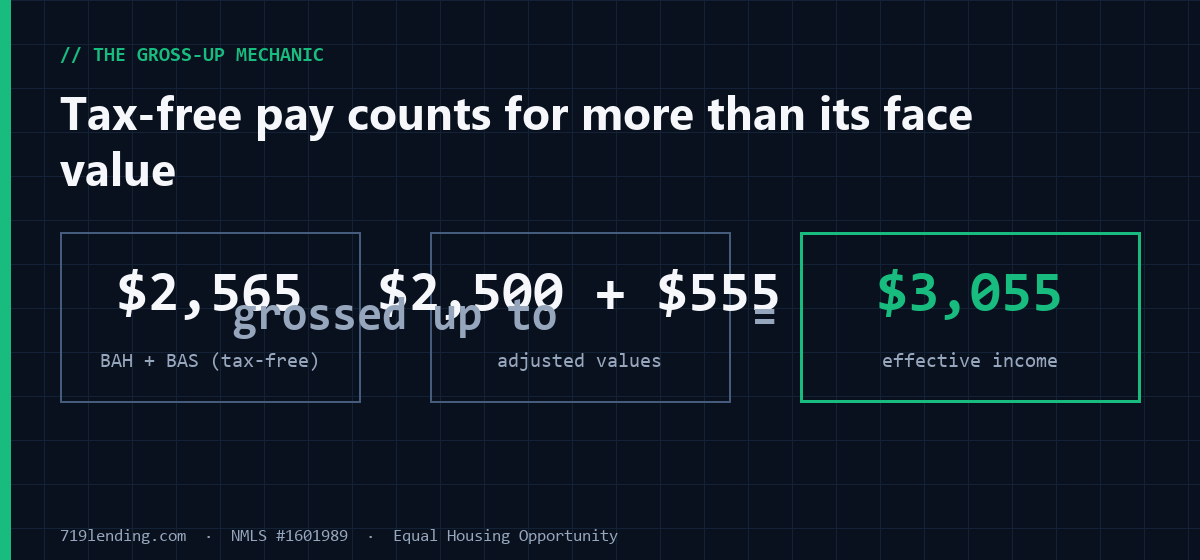

On a VA loan, your military income is more than base pay. BAH and BAS are tax-free allowances a lender can gross up — which quietly raises the income you qualify on. Here's which pay counts, and the charts to prove it.

The VA’s second qualifying test: how residual income decides your loan

Last updated: June 30, 2026 — residual income tables, the $80,000 loan-tier split, the 41% DTI threshold, and the 20% bump reflect the current VA Lenders Handbook. Figures are general; confirm current requirements for your situation.

Residual income is the VA’s second qualifying test, and it asks one blunt question: after your mortgage, every monthly debt, your paycheck taxes, and your utilities are paid, how many real dollars are left for groceries, gas, and life? The VA compares that leftover against a published minimum for your region, family size, and loan size. Miss it and the loan can stall even when your debt-to-income ratio looks fine.

Run your numbers in the VA Residual Income calculator to see exactly where you land on both tests.

What is VA residual income, and why does it exist?

Residual income is the cash you have left over each month after you subtract your full housing expense, all your monthly debts, your paycheck taxes, and your utilities from your gross monthly income. The VA cares about this number because debt-to-income (DTI) alone can be misleading. A 40% DTI on a high income leaves a comfortable cushion; the same 40% on a modest income can leave a family scraping. Residual income measures the cushion directly, in dollars, instead of trusting a percentage.

That’s why the VA built it into the VA Lenders Handbook as a separate, hard requirement. Our calculator runs both checks at once and returns a clear PASS or FAIL on each: the residual-income test and the DTI test, side by side.

How is residual income actually calculated?

The math is a subtraction problem. You start with gross monthly income and pull out four buckets:

| Subtracted from gross income | What it includes |

|---|---|

| Full monthly housing expense | Principal & interest, property taxes, homeowner’s insurance, HOA |

| All monthly debts | Car loans, credit cards, student loans, and more (add a row per debt) |

| Paycheck taxes | Federal, state, Social Security, and other withholding |

| Utilities | Estimated from square footage or entered manually |

Whatever survives that subtraction is your residual income. The calculator also shows a “where your paycheck goes” breakdown so you can see exactly which buckets are eating the most. One convenience built in: utilities auto-estimate at $0.14 per square foot from the home’s square footage, with a one-tap manual override if you already know your real numbers.

What’s the minimum residual income I need?

There’s no single number. The VA minimum depends on three things: your region, your family size, and your loan tier. Region is set automatically from your state and splits the country into Northeast, Midwest, South, and West. Family size scales the requirement, and families beyond seven keep extending (roughly +$75 to +$80 per additional member). Loan tier splits at $80,000: loans under $80,000 use a lower table, and loans of $80,000 or more use a higher one.

The calculator pulls the official figure for your exact situation, so you don’t have to guess which row of which table applies. As an illustration of how specific these numbers get: the correct Northeast figure for a family of six on the higher table is $996 (not the $966 some older tools printed — more on that below).

How does DTI change the residual requirement?

This is the part most people miss. If your debt-to-income ratio lands at 41% or higher, the VA raises your required residual income by 20% (multiply it by 1.2). The logic is straightforward: a borrower carrying heavier debt needs a bigger cushion to be safe. The calculator detects this automatically and shows the math, so you can watch your required residual jump the moment DTI reaches the threshold.

That creates a few common outcomes worth understanding:

- DTI under 41%: you’re held to the standard regional minimum.

- DTI at or above 41%: the 20% bump applies, but a strong residual cushion can still carry you to a PASS.

- Split decision: you can PASS the residual test but FAIL on DTI, or vice versa. The tool reports each independently so you know which one is the problem.

What does a real example look like?

Here’s an illustrative scenario showing the shape of the output (your numbers will differ):

| Line item | Example amount |

|---|---|

| Gross monthly income | $7,500 |

| Less: housing (PITI + HOA) | −$2,400 |

| Less: monthly debts | −$650 |

| Less: paycheck taxes | −$1,500 |

| Less: utilities | −$280 |

| Residual income | $2,670 |

| Required residual (region/family/tier) | $1,003 |

| Result | PASS — $1,667 cushion |

These figures are an example for illustration only, not a quote, and your real result will depend on your own inputs. The point is the format: you get your residual income, the required minimum for your exact situation, the dollar cushion or shortfall, and a PASS/FAIL on both the residual and DTI tests. Try the VA Residual Income calculator with your own numbers to see your real cushion.

What two bugs does this calculator fix?

The blog angle here is honesty. Many residual-income tools online are copies of an original that carried real math errors, and our build documents the fixes right in an “honest math” warning:

- The loan-tier bug: the original silently used the under-$80,000 table for every loan, including loans well over $80,000. That understates the required residual for most real VA purchases. Our calculator routes you to the correct table based on your actual loan amount.

- The wrong regional number: the old version used 966 for a Northeast family of six when the correct VA Lenders Handbook figure is 996. We use the right number.

There’s also a region-assignment fix: Washington, DC is correctly placed in the South region, matching the VA’s own classification, where a legacy version put it elsewhere. Small details, but they’re exactly the kind of thing that flips a borderline PASS into a FAIL or hides a problem until underwriting.

Where does this fit with your other VA numbers?

Residual income is one piece. If you’re sizing up a VA purchase, pair it with the Maximum VA Loan calculator to find your $0-down ceiling, and read the VA Income guide to understand how base pay, BAH, and BAS count toward qualifying. You can find all of 719’s mortgage tools on the Calculate hub.

Knowing your residual income before you write an offer means fewer surprises in underwriting. Run your numbers now and see whether your family has enough left over each month after the mortgage.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. Calculator results are estimates. 719 Lending is not affiliated with or endorsed by any government agency.

Frequently asked questions

What is VA residual income? Residual income is the money left over each month after you subtract your full housing expense, all monthly debts, paycheck taxes, and utilities from your gross monthly income. The VA compares this leftover against a published minimum for your region, family size, and loan size as a second qualifying test alongside debt-to-income.

How much residual income does the VA require? There's no single number. The minimum depends on your region (Northeast, Midwest, South, or West, set from your state), your family size, and your loan tier (under $80,000 versus $80,000 or more). Larger families need more, and families beyond seven add roughly $75 to $80 per extra member. The calculator pulls the exact official figure for your situation.

Does my DTI affect the residual income requirement? Yes. If your debt-to-income ratio is 41% or higher, the VA raises your required residual income by 20% (it multiplies the minimum by 1.2). The calculator detects this automatically and shows the math, so you can see the requirement increase once DTI reaches the threshold.

Can I pass DTI but fail the residual income test? Yes, and the reverse is true too. The two tests are independent. You can have an acceptable debt-to-income ratio yet fall short on residual income, or pass residual income while failing DTI. The calculator returns a separate PASS or FAIL on each so you know which one needs attention.

How are utilities calculated in the residual income test? The calculator auto-estimates utilities at $0.14 per square foot based on the home's square footage. If you already know your real utility costs, you can override the estimate manually with one tap. These figures are estimates, not a final underwriting determination.

Related Posts