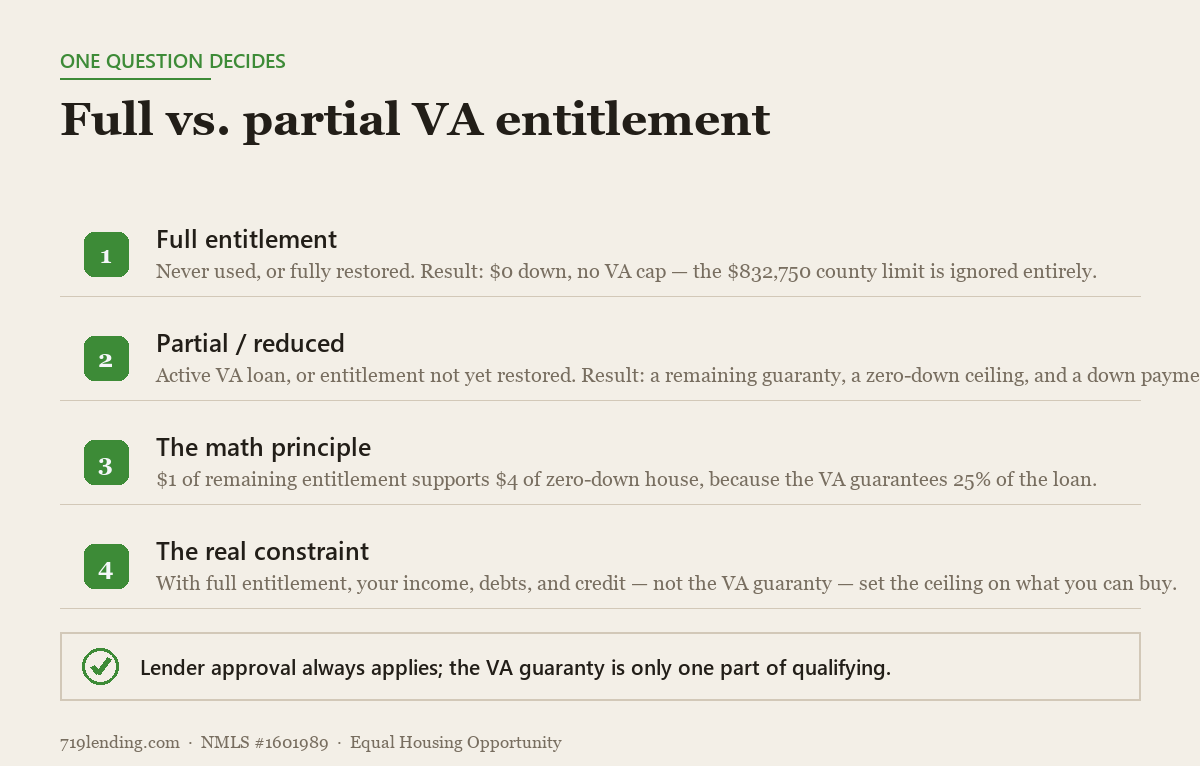

Since the 2020 Blue Water Navy Act, there is no VA loan cap with full entitlement — you do not owe 25% down above the county limit. One Yes/No question decides whether $832,750 even matters to you. Here's how the Maximum VA Loan calculator finds your real $0-down ceiling.

How VA loans count military income: BAH, BAS, and the pay that raises what you qualify for

Last updated: June 30, 2026 — pay figures (base pay, BAH, BAS) are illustrative examples; confirm current-year rates against the DoD pay tables, the official BAH lookup, and your most recent LES.

On a VA loan, your qualifying income is more than base pay. Lenders also count BAH (Basic Allowance for Housing) and BAS (Basic Allowance for Subsistence) — and because those allowances are tax-free, they can be “grossed up,” which raises your effective qualifying income above the face dollar amount. Special and incentive pays can count too if they’re stable and likely to continue.

If you’re a service member in Colorado Springs eyeing a VA loan, the single biggest misread we see is treating base pay as your whole income. It isn’t. The way the military pays you — a base salary plus a stack of allowances and special pays — is exactly the kind of structure VA underwriting was built to handle. Understanding which pieces count, and how the tax-free ones get a boost, can change whether you qualify for the house you actually want.

This is a plain-English breakdown of how your Leave and Earnings Statement (LES) translates into qualifying income. It’s reference material, not a calculator — but once you know what counts, our VA Income page walks you through it line by line and links straight to two free tools that do the heavy lifting: our Maximum VA Loan estimator and our VA Residual Income test. Start with the VA Income breakdown to map your pay.

What military pay actually counts toward a VA loan?

Most stable, documentable components of your military compensation count. The core pieces a lender pulls from your LES are base pay, BAH, and BAS, plus special and incentive pays that are likely to continue. Here’s how each is generally treated:

| Pay component | What it is | Taxable? | Typically counts as qualifying income? |

|---|---|---|---|

| Base pay | Your core salary, set by rank and years of service | Yes | Yes |

| BAH (Basic Allowance for Housing) | Tax-free allowance for off-base housing, set by zip and rank | No | Yes — and can be grossed up |

| BAS (Basic Allowance for Subsistence) | Tax-free allowance for food | No | Yes — and can be grossed up |

| Special / incentive pays | Flight pay, hazard pay, sea pay, jump pay, etc. | Often taxable | Often, if stable and likely to continue |

The headline: BAH and BAS are not extras a lender ignores. They’re real, recurring income — and for many service members in the Colorado Springs market, BAH alone is one of the largest lines on the LES.

Why are tax-free allowances worth more than they look?

Because they can be “grossed up.” When income isn’t taxed, every dollar of it goes further than a taxable dollar — so VA underwriting guidelines let a lender adjust tax-free income upward to reflect its true buying power before measuring it against your debts. The result: your BAH and BAS count for more than their face value in the qualifying math.

Here’s the idea with example numbers (illustration only — your figures come from your own LES and lender, and results are estimates):

| Income type | Monthly amount (example) | Grossed-up value (example) |

|---|---|---|

| Base pay (taxable) | $3,200 | $3,200 (no adjustment) |

| BAH (tax-free) | $2,100 | ~$2,500 |

| BAS (tax-free) | $465 | ~$555 |

| Effective qualifying income | $5,765 | ~$6,255 |

That gross-up swing — here, roughly $490 a month of additional effective income — can meaningfully change how much loan you qualify for, because qualifying is driven by the ratio of income to debt. These numbers are examples to show the mechanic, not a quote. The exact gross-up percentage and which pays a lender applies it to depend on the program and your file.

How do I find my numbers on the pay charts?

Two places. Base pay comes from the annual military basic pay tables, indexed by your rank (pay grade) and years of service. BAH comes from a separate table indexed by your duty-station zip code, rank, and whether you have dependents — which is why a Colorado Springs BAH differs from the same rank’s BAH elsewhere. BAS is a flat monthly figure set each year, one rate for enlisted and one for officers.

To pull your own figures, start with the authoritative source: the DoD Military Compensation pay tables for base pay and BAS, and the official BAH rate lookup for your zip. Then cross-check against your most recent LES — the lender will, too. A quick way to read it:

- Base pay — find your pay grade (e.g., E-5, O-3) and your years of service in the basic pay table.

- BAH — look up your duty-station zip, your grade, and your dependent status.

- BAS — use the current-year flat rate for enlisted or officer.

- Special pays — list anything recurring on your LES; be ready to document continuation.

What about deployment, special pays, and continuing income?

The test is stability and likelihood of continuance. A pay that shows up every month and is expected to keep coming — flight pay you’ve drawn for years, sea pay tied to your assignment — is more likely to count than a one-time bonus. Combat or hazard pay tied to a specific deployment may be treated more cautiously because it can stop when the deployment ends. None of this is a yes/no you should guess at: it’s exactly what a VA-experienced lender reviews line by line on your LES.

The practical move is to document everything recurring and let the underwriter make the call against current VA guidelines — rather than assume a special pay won’t count and shortchange yourself.

How do I turn this into a real qualifying number?

Once you know which pay counts, the next two questions are “how much house does that support?” and “does my family clear the VA’s residual-income test?” That’s where our tools come in:

- Maximum VA Loan calculator — estimate the loan size your qualifying income can support.

- VA Residual Income calculator — run the VA’s second, lesser-known qualifying check: whether you have enough left over each month after the mortgage and debts.

Both pull from the same income picture you just built here, so it’s worth getting the income side right first. You’ll find these and every other 719 Lending tool on our Calculate hub.

Run your numbers: head to the VA Income page and use its income breakdown to map your LES to qualifying income, then jump into the Maximum VA Loan tool to see what it supports. When you’re ready to put real figures in front of someone, the VA Income page also connects you with a 719 Lending loan officer who works VA files every day. All calculator results are estimates, not a commitment to lend.

Frequently asked questions

Does BAH count as income for a VA loan?

Yes. BAH is treated as qualifying income, and because it’s tax-free it can be grossed up — meaning it counts for more than its face value in the qualifying math.

Can BAS be used to qualify too?

Yes. Like BAH, BAS is a tax-free allowance that typically counts and can be grossed up. It’s a flat monthly figure set each year for enlisted and officers.

What does “grossing up” tax-free income mean?

It’s an upward adjustment lenders apply to non-taxable income to reflect its higher buying power versus taxable income, before measuring it against your debts. The exact percentage depends on the program and your file.

Will my deployment or special pays count?

Often, if they’re stable and likely to continue. Recurring, documentable pays are more likely to count than one-time bonuses or pay tied to a deployment that may end. A VA-experienced underwriter reviews each line on your LES.

Where do I find my exact base pay and BAH?

Use the DoD military basic pay tables for base pay and BAS, and the official BAH rate lookup for your duty-station zip, then cross-check your most recent LES.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Related Posts