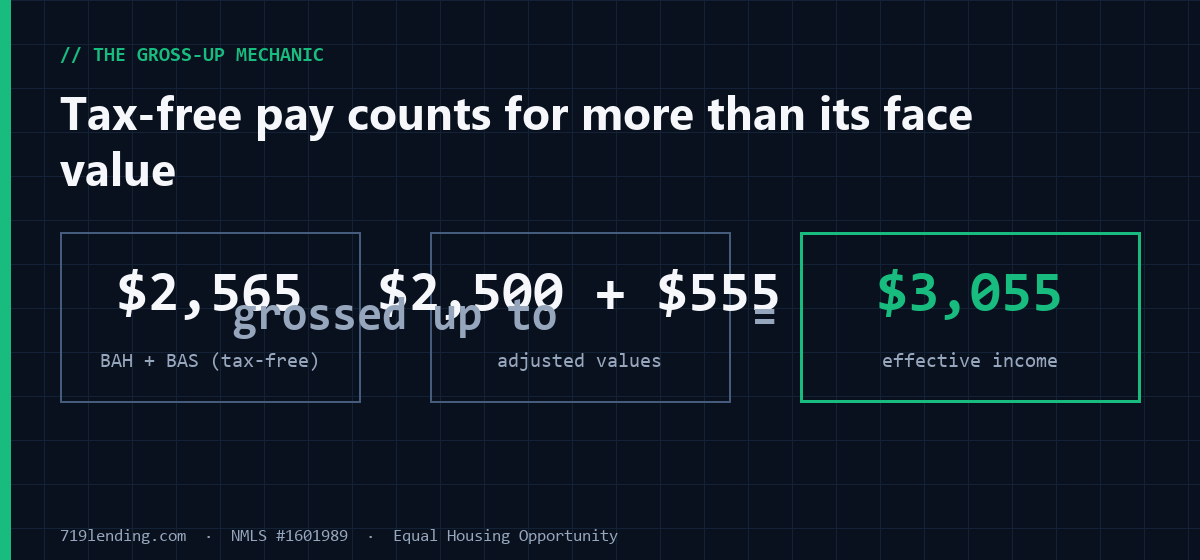

On a VA loan, your military income is more than base pay. BAH and BAS are tax-free allowances a lender can gross up — which quietly raises the income you qualify on. Here's which pay counts, and the charts to prove it.

The $832,750 myth: how one question reveals your real $0-down VA loan limit

Last updated: June 30, 2026 — reflects the 2026 baseline county loan limit ($832,750) and post-2020 Blue Water Navy Act entitlement rules. Figures are general and illustrative; confirm current limits and your verified entitlement.

Here’s the honest answer most veterans never get: if you have your full VA entitlement, there is no VA loan limit. None. You can buy at $600,000 or $1.2 million with $0 down, because since the 2020 Blue Water Navy Act the VA backs 25% of any loan size. The famous “$832,750 limit” only matters if part of your entitlement is already tied up in another VA loan. One Yes/No question decides everything.

Why is $832,750 the wrong number for most veterans?

Because for veterans with full entitlement, that figure is irrelevant. The $832,750 baseline (the 2026 county loan limit this calculator uses by default) describes how much guaranty the VA used to cap. Before 2020, exceeding it meant you had to cover the gap. The Blue Water Navy Vietnam Veterans Act of 2019 — effective January 1, 2020 — removed that ceiling for anyone with full entitlement.

So when a veteran with full entitlement asks “how much house can I buy with nothing down?”, the correct answer is no cap, $0 down at any price — subject only to what a lender will actually approve based on income and credit.

This is where a lot of older tools quietly fail. The legacy version of this calculator had a real bug: with full entitlement, it still charged 25% down on the portion of the price above the county limit. That’s flat wrong post-2020. Our Maximum VA Loan calculator fixes it — full entitlement returns “no VA cap, $0 down,” exactly as the law reads.

What is the one question that changes the whole answer?

The toggle is simple: Do you have your full VA entitlement, or is some of it tied up? That single Yes/No swaps the entire result.

| Your entitlement status | What the calculator returns |

|---|---|

| Full entitlement (never used, or fully restored) | “$0 down, no VA cap” — county limit ignored entirely |

| Partial / reduced (active VA loan, or one not yet restored) | Remaining guaranty, a zero-down ceiling, and any required down payment on a higher-priced home |

If you’ve never used your benefit, or you sold the home and had your entitlement restored, you’re on the full-entitlement path — and the limit conversation is over. Run your numbers in the Maximum VA Loan calculator to see which path you land on.

How does the math work if some of my entitlement is used?

This is the path veterans with an active VA loan need. The VA guarantees 25% of a loan. When some entitlement is already committed, the calculator works out your remaining guaranty, then your zero-down ceiling, then any down payment as the 25%-coverage shortfall on a more expensive home.

The three steps:

- Remaining guaranty = 25% of the county limit − entitlement already used.

- Zero-down ceiling = remaining guaranty × 4. (Because the VA covers 25%, every $1 of remaining entitlement supports $4 of zero-down house.)

- Required down payment (only if you buy above that ceiling) = the gap needed to bring total coverage back to 25% on the higher price.

That last principle is worth repeating: $1 of entitlement = $4 of zero-down house. It’s the whole reason the partial-entitlement math lands where it does.

A worked example (illustrative)

Say a veteran has $104,000 of entitlement already used and wants to buy a $500,000 home. The calculator finds the remaining guaranty against the county limit, sizes the zero-down ceiling, and — because $500k sits above that ceiling — returns a required down payment of roughly $20,813. Same veteran, smaller price under the ceiling? $0 down required.

| Scenario (example) | Result |

|---|---|

| Full entitlement, any price | $0 down, no VA cap |

| Partial entitlement, price under ceiling | $0 down required |

| Partial entitlement, $500k with $104k used | ~$20,813 down (the guaranty shortfall) |

These are estimates to illustrate the mechanics — your actual figures depend on your county limit, exact entitlement used, and lender approval.

What does the “how your number is built” breakdown show?

On the partial-entitlement path, the calculator doesn’t just spit out a number — it shows its work. The breakdown table walks through your maximum guaranty, your remaining entitlement, the guaranty actually backing the new loan, and the max base loan amount. You see exactly where your zero-down ceiling comes from and why any down payment is required, instead of trusting a black box. That transparency is the point: honest math you can check line by line. See it on your own scenario in the Maximum VA Loan calculator.

Is there any upper limit at all?

The VA itself imposes no cap with full entitlement, but lenders do set their own overlays. This calculator applies a $4M lender-overlay cap on the max base loan as a practical ceiling. For the overwhelming majority of Colorado Springs and El Paso County veterans, that’s far above anything in play — the real constraint is your income, debts, and credit, not the VA guaranty. Want to pressure-test what you’d actually qualify for? Start at our Calculate hub and pair this with our other VA tools.

Frequently asked questions

Does full VA entitlement really mean no loan limit? Yes. Since the Blue Water Navy Act took effect January 1, 2020, the VA backs 25% of any loan size with full entitlement, so there is no VA cap and no required down payment based on the county limit. Lender approval still applies.

Then why do I keep seeing $832,750? That’s the 2026 baseline county loan limit, and it only governs your benefit when part of your entitlement is already used. With full entitlement, it doesn’t apply to you.

I have an active VA loan. Can I still buy with $0 down? Possibly — up to your zero-down ceiling, which is your remaining guaranty times four. Above that ceiling you’d cover the 25% shortfall as a down payment. The calculator computes both for your numbers.

Where does “$1 of entitlement = $4 of house” come from? The VA guarantees 25% of the loan. Twenty-five percent coverage means every dollar of remaining entitlement supports four dollars of zero-down purchase price.

Are the calculator results exact? No — they’re estimates to show you the mechanics and a realistic ceiling. Your final figures depend on your verified entitlement, county limit, and a full application.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

719 Lending is not affiliated with or endorsed by any government agency.

Related Posts