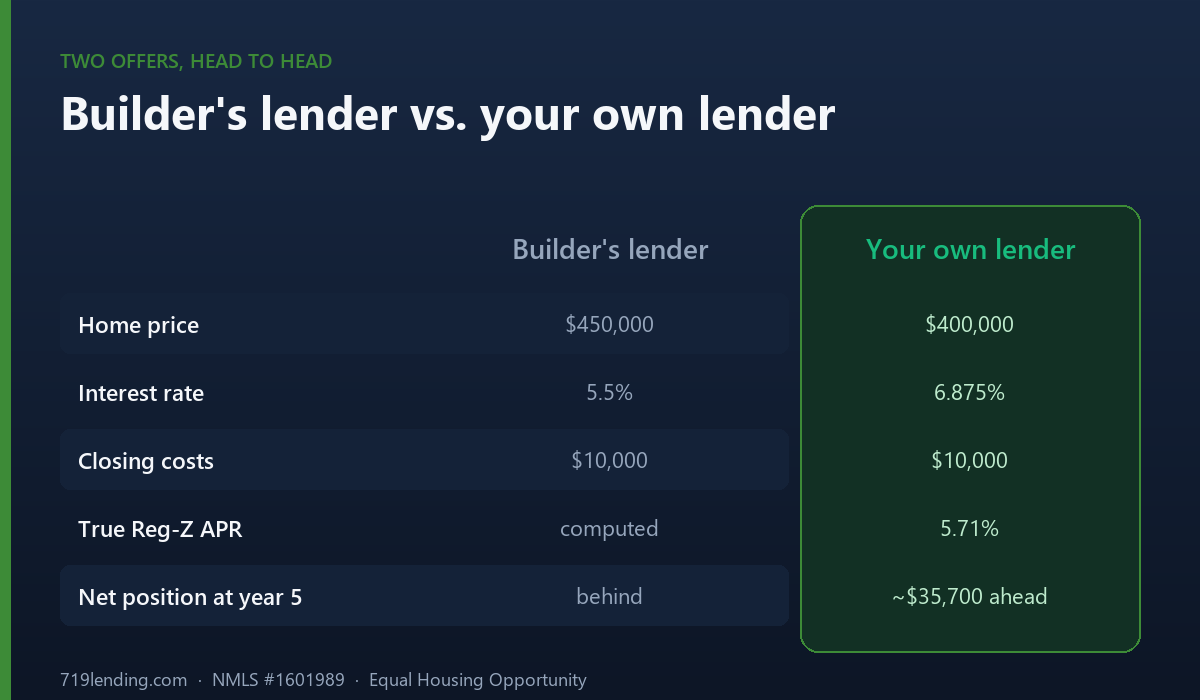

A builder's "preferred lender" dangles a rate the bank can't touch — then quietly funds it with a higher home price. Here's the math that names the winner in dollars, not rate.

The temporary buydown calculator that admits it: cost = savings, so the only question is who pays

Last updated: June 30, 2026 — figures (rates, payments, and buydown costs) are illustrative examples from the calculator’s defaults; confirm current numbers for your scenario.

A temporary buydown lowers your mortgage payment for the first year or two, and here’s the honest math most calculators hide: its total cost equals the sum of every dollar of payment relief it gives you. Cost = savings. So a buydown isn’t a discount — it’s prepaid relief, and the only question that matters is who pays. Our temporary buydown calculator shows that plainly and hands you the exact number to ask a seller to cover.

What is a temporary buydown — and why is “cost = savings” the whole story?

A temporary buydown is an escrowed pot of money that subsidizes your principal-and-interest payment for the first one to three years of a fixed-rate loan. Your note rate doesn’t change. Instead, the escrow covers the gap between your reduced payment and the full-rate payment, year by year, until the fund runs out and you settle into the real payment.

Because that escrow only ever pays out the relief you receive, the math closes perfectly: the total cost of the buydown is the sum of every tier’s annual relief. There’s no markup, no spread, no hidden margin built into the structure. That’s why the calculator treats the cost figure as doing double duty — it’s both “what this costs” and “what to write into a seller-concession ask.” Run your own loan in the temporary buydown calculator and you’ll see the cost line and the relief line are the same number.

How does a 2-1 buydown actually work?

The structure name tells you the rate reduction per year. A 2-1 buydown drops your effective rate by 2% in year one and 1% in year two, then snaps to the full note rate in year three. The calculator models four switchable structures: 1-0, 1-1, 2-1, and 3-2-1. A 2-1 breaks into three rows of decomposition; a 3-2-1 breaks into four.

Here’s the default scenario — a $300,000 loan at a 7.5% note rate on a 30-year term, structured as a 2-1 buydown. These figures are illustrative examples from the tool’s defaults, not a quote:

| Year | Effective rate | What you pay (P&I) | What the escrow covers |

|---|---|---|---|

| Year 1 | 5.5% (−2%) | ~$1,703/mo | ~$394/mo relief |

| Year 2 | 6.5% (−1%) | higher than year 1 | smaller relief |

| Year 3 onward | 7.5% (full) | ~$2,098/mo | $0 — fund exhausted |

On that default, year one runs roughly $394 a month less than the full $2,098 payment, and the whole thing costs about $7,149 — which is also the total relief delivered. The calculator draws a year-by-year staircase and an SVG bar chart with the buydown-covered portion shaded green so you can see exactly how much of each payment the escrow is footing.

How much does a temporary buydown cost?

Exactly as much as it saves you — that’s the honest-cost identity. The deeper the structure, the bigger the number. A 3-2-1 buydown delivers more relief over more years, so it costs more than a lighter 1-0. The calculator computes the full-rate P&I, the reduced P&I for each buydown year, the savings the escrow covers, and the total cost, all on a principal-and-interest basis (it does not model taxes or insurance).

It also guards the inputs so the math stays real: loan amounts run from $1,000 to $50 million and rates from 0.5% to 20%. If any buydown tier would push your effective rate to zero or below — for example, a 3-2-1 on a 2.5% note — the tool returns an error instead of printing a nonsense negative-rate payment.

Who should pay for the buydown — and when should you skip it?

This is where the “cost = savings” framing earns its keep. Because the cost is just prepaid relief, who funds it decides whether a buydown is smart or pointless.

- Seller or builder pays: This is the buydown’s best use. In a market where a seller is motivated, that ~$7,149 becomes a concession line in your offer — you’re getting two years of lower payments on someone else’s dime. The calculator is built to convert the total-cost number straight into that ask.

- You pay it yourself: Here the tool is blunt. If you fund your own buydown, you’re “mostly moving your own money around” — paying cash up front to get the same cash back as monthly relief. In that case, the calculator tells you to price permanent points instead, which lower your rate for the life of the loan rather than for two years.

That’s the verdict the calculator is designed to deliver: not “buy this,” but “make the seller pay for it, or buy permanent points.” See the full year-by-year breakdown and the who-pays verdict in the temporary buydown calculator, or browse every tool on the Calculate hub.

Why is this a negotiation tool, not just a math tool?

Because the single most important output — total cost — is also the number you hand to the other side of the deal. For buyers and agents in Colorado Springs and across El Paso County, a temporary buydown is a way to make a fixed list price feel more affordable in the early years without touching the sticker. Instead of asking a seller for a $7,000 price cut that barely moves the monthly payment, you ask them to fund a 2-1 buydown for the same money and the buyer feels it as ~$394 a month in year one. The calculator gives you the exact figure to write into the offer — that’s the “write this into the offer” framing baked into the tool.

Frequently asked questions

Does a temporary buydown lower my interest rate? No. Your note rate stays the same for the whole loan. A buydown uses an escrow fund to subsidize your payment for the first year or two, so your effective payment is lower temporarily even though the underlying rate never changes. After the fund runs out, you pay the full-rate payment.

Is a 2-1 buydown a discount? No — it’s prepaid payment relief. The total cost equals the sum of all the relief delivered, so nobody is giving you a discount; someone is pre-paying part of your payments. Whether that’s a good deal depends entirely on who funds it.

When should I buy permanent points instead? When you’d be paying for the buydown out of your own pocket. The calculator flags this case directly: funding your own temporary buydown is mostly moving your own money around, so permanent points — which lower your rate for the life of the loan — are usually the better use of cash.

What does the calculator actually compute? Given your loan amount, note rate, term (15 or 30 years), and structure (1-0, 1-1, 2-1, or 3-2-1), it returns the full-rate P&I, the reduced P&I per buydown year, the escrow-covered savings, the total cost, a year-by-year tier breakdown, and a bar chart. It’s principal-and-interest only and shows estimates, not a quote.

What’s the catch with the structure I pick? Deeper structures like 3-2-1 cost more because they deliver more relief over more years. And the tool won’t let a tier push your effective rate to zero or below — if it would, it returns an error instead of a bad number.

Ready to turn a payment into a negotiation? Run your numbers in the temporary buydown calculator and see your seller-concession ask in seconds.

Calculator results are estimates only.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Related Posts