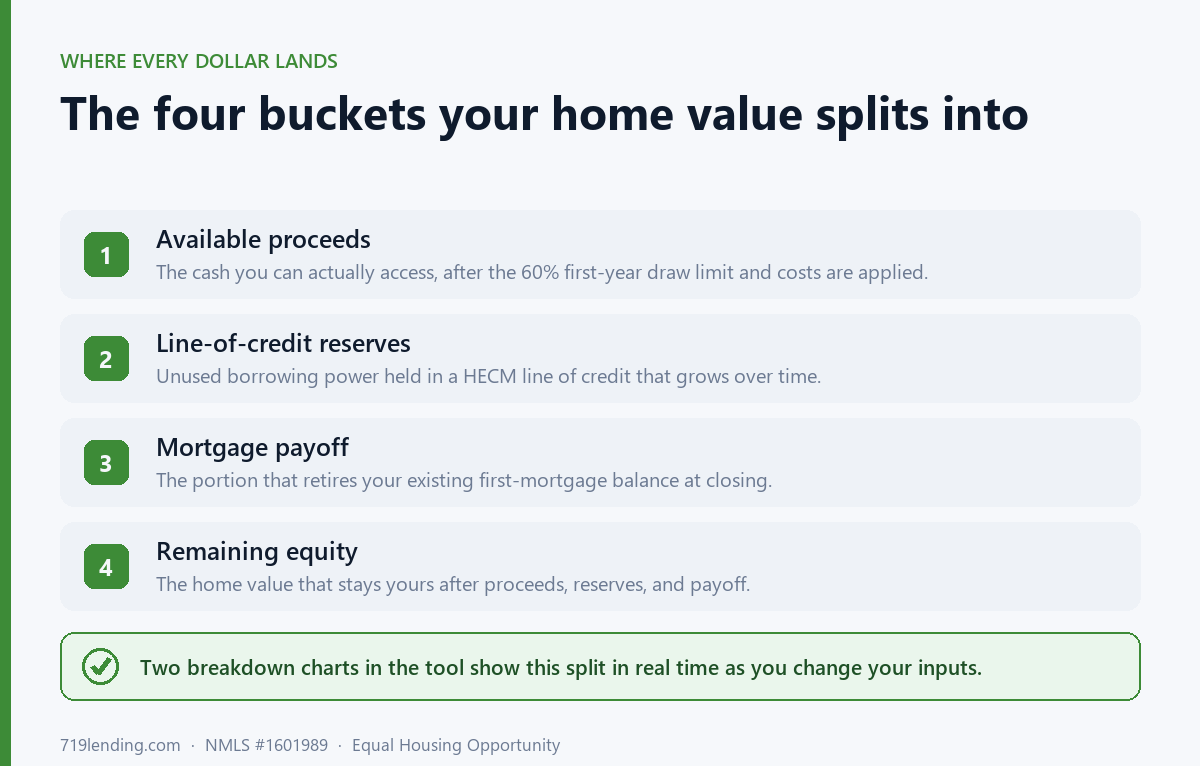

Most HECM estimators inflate your payout by ignoring the FHA value cap and charging an outdated premium. Our reverse mortgage calculator bakes in the honest math — 2.0% UFMIP, the $1,209,750 ceiling, the 60% first-year limit — and runs HECM against HomeSafe at the same time.

What is APOR? The federal rate that decides if your mortgage is an HPML

Last updated: June 30, 2026 — APOR thresholds and example figures are general and current as of this date; confirm the current published APOR and your lender’s determination before relying on them.

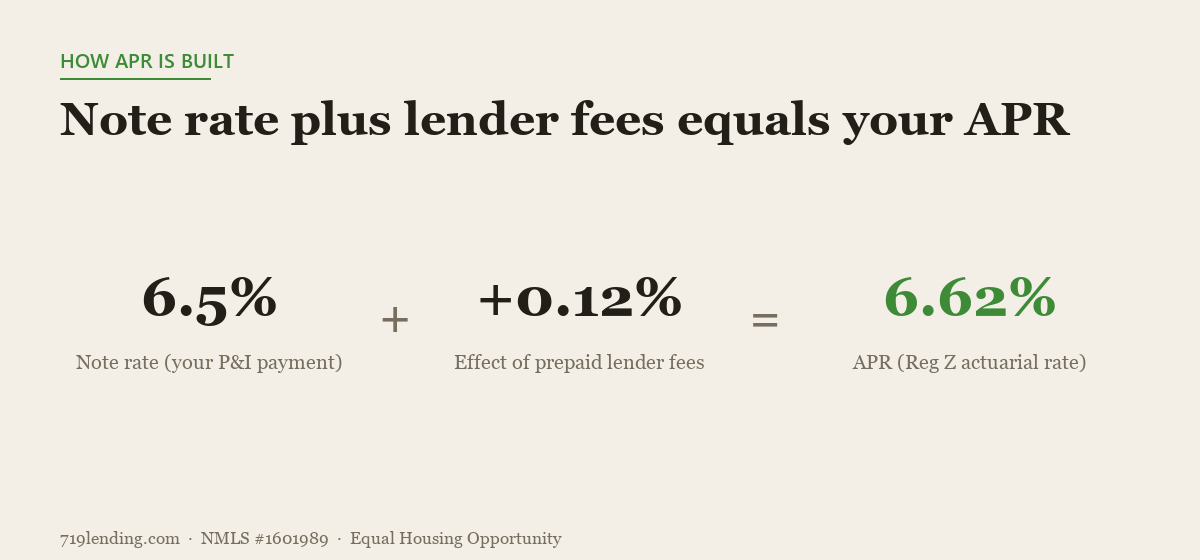

APOR (Average Prime Offer Rate) is a weekly benchmark rate the federal government publishes for prime mortgages. Lenders compare your loan’s APR to the APOR in effect on the week you locked your rate. That single gap — APR minus APOR — quietly decides whether your mortgage triggers escrow rules, a stricter appraisal, HOEPA high-cost protections, or loses its FHA safe harbor.

Most borrowers never hear the term until underwriting. But APOR is one of the most consequential numbers attached to your loan, and it’s sitting in a public federal dataset that almost nobody looks up. Our APOR Lookup tool pulls the real published figure for any lock date back to 2017 — not a hardcoded estimate — and runs the three separate regulatory checks your loan is being measured against. Its results are estimates for education, not a compliance determination.

What does APOR actually measure?

APOR represents the average annual percentage rate offered to highly qualified borrowers for a given loan type and term. The CFPB and FFIEC publish it as a weekly yield table, broken out by fixed vs. adjustable and by term (30, 20, 15, 10, 5 years). It’s essentially the “going market rate” for a clean, prime loan that week.

Your loan’s spread over APOR is what matters. A higher-priced loan isn’t inherently bad — but the size of the gap above APOR is what regulators use to decide how much extra protection a borrower gets. The further your APR sits above APOR, the more rules click on.

Our tool plots the full APOR history and marks the exact week you locked, so you can see where your rate landed on the trend line. Run your numbers to see your spread in seconds.

Why does the lock date — not the closing date — matter?

This is the single most common and costly mistake. The APOR that governs your loan is the one in effect on the week you locked your rate, not the week you closed. Those can be weeks apart, and APOR moves every week. Pick the wrong date and your spread — and every determination built on it — can be wrong.

The lookup snaps your lock date to the most recent published APOR week on or before that date, exactly the way the federal rule works. There’s a built-in tooltip reminding you to use the lock date, because mixing it up with closing is how loans get misclassified.

What are the three federal lines my loan is measured against?

This is where APOR gets misunderstood. APOR itself is identical across loan programs — only the threshold changes. The same published APOR can pass a conventional loan and flag an FHA one. Our tool runs all three determinations in parallel on your one loan:

| Determination | Rule | What it triggers | Threshold (spread over APOR) |

|---|---|---|---|

| HPML | Reg Z (higher-priced mortgage loan) | Mandatory escrow, stricter appraisal | 1.5 first-lien · 2.5 jumbo · 3.5 subordinate |

| High-cost (HOEPA) | HOEPA | Heightened high-cost protections | >6.5 first-lien · >8.5 subordinate |

| FHA QM safe harbor | Ability-to-Repay / QM | Safe harbor vs. rebuttable presumption | APOR + 1.15 + annual MIP |

So a loan can clear HPML but still sit in rebuttable-presumption territory on the FHA side, because the FHA calculation folds in your annual MIP (default 0.55%). That’s why the tool distinguishes all three rather than giving you one pass/fail. These are estimates for education — your lender’s compliance engine makes the final call — but they tell you exactly where you stand before you get there.

How does the lookup actually work?

Unlike calculators that bake in a guessed rate, this tool fetches the real federal data live. It reads the FFIEC YieldTable files server-side, edge-caches them for 12 hours, and returns the genuine published number for your week. A few details worth knowing:

- Date-as-of snapping: your lock date resolves to the most recent published week on or before it.

- Nearest-term snapping: if your exact term isn’t published, it snaps to the nearest one and flags it honestly so you know it’s an approximation.

- Graceful fallback: if the federal feed is ever down, it points you to the official FFIEC Rate Spread Calculator rather than guessing.

You enter your rate-lock date, loan type (fixed/adjustable), term, and — optionally — your APR, program (conventional/FHA/VA/USDA), lien position, jumbo flag, and annual MIP. It returns the published APOR, the exact week-of date applied, your spread, and the three determinations.

What does a result look like?

Here’s an illustrative example of how the tool reports a single loan (these numbers are examples, not a quote, and the output is an estimate):

| Output | Example result |

|---|---|

| Published APOR (week-of) | 6.30% (week of your locked date) |

| Your loan APR | 8.00% |

| Rate spread (APR − APOR) | +1.70 pts |

| HPML (first-lien, 1.5) | HPML — over 1.5 |

| High-cost (HOEPA) | Not high-cost |

| FHA safe harbor | Rebuttable presumption |

In that example a +1.70 spread clears HOEPA easily but exceeds the 1.5 HPML line, so escrow and appraisal rules apply — and on the FHA side it falls into rebuttable presumption rather than safe harbor.

Who should run this?

Anyone locking a rate that feels above market, anyone on an FHA loan wondering about safe harbor, and any borrower who wants to understand why their lender suddenly required an escrow account or a second appraisal. It’s also useful after the fact — you can look up a past loan‘s lock week back to 2017 and see exactly how it was classified.

It’s a single-scenario lookup, not a payment calculator, but it answers a question most tools ignore. Try the APOR Lookup calculator with your real lock date, or browse the rest of our mortgage calculators hub to run the full picture.

Want a human to walk through what your spread means for your specific file? That’s exactly the kind of thing a local Colorado Springs broker should be able to explain in plain language.

Frequently asked questions

What is APOR in a mortgage?

APOR (Average Prime Offer Rate) is a weekly benchmark rate the CFPB and FFIEC publish for prime mortgages by type and term. Lenders compare your loan’s APR to the APOR in effect the week you locked. The gap between them determines which federal protections — escrow, appraisal, HOEPA, FHA safe harbor — apply to your loan.

Do I use my lock date or closing date for APOR?

Your lock date. The governing APOR is the one published for the week you locked your rate, not the week you closed — and those can be weeks apart while APOR changes weekly. Using the closing date is the most common mistake and can misclassify your loan. The lookup tool snaps your lock date to the correct published week automatically.

What makes a loan an HPML?

A loan is a higher-priced mortgage loan (HPML) under Reg Z when its APR exceeds APOR by 1.5 points on a first lien, 2.5 on a jumbo, or 3.5 on a subordinate lien. Crossing that line triggers mandatory escrow and a stricter appraisal requirement. The APOR Lookup tool runs this check and shows your exact spread as an estimate.

Why can the same APOR pass a conventional loan but flag an FHA one?

Because APOR is identical across programs — only the threshold moves. HPML uses a 1.5-point line, HOEPA uses 6.5+, and FHA QM safe harbor uses APOR plus 1.15 plus your annual MIP. A loan can clear the conventional HPML test yet fall into FHA rebuttable presumption because the FHA calculation folds in mortgage insurance. The tool runs all three determinations in parallel.

Is the APOR figure in the tool real or an estimate?

The APOR figure itself is the real published federal number — the tool fetches FFIEC YieldTable files live, server-side, and edge-caches them for 12 hours rather than using a hardcoded value. If the federal feed is ever down, it points you to the official FFIEC Rate Spread Calculator. The classifications it builds on top (HPML, HOEPA, FHA safe harbor) are estimates for education; your lender makes the final compliance determination.

Ready to see where your loan lands? Run your numbers in the APOR Lookup calculator.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Related Posts