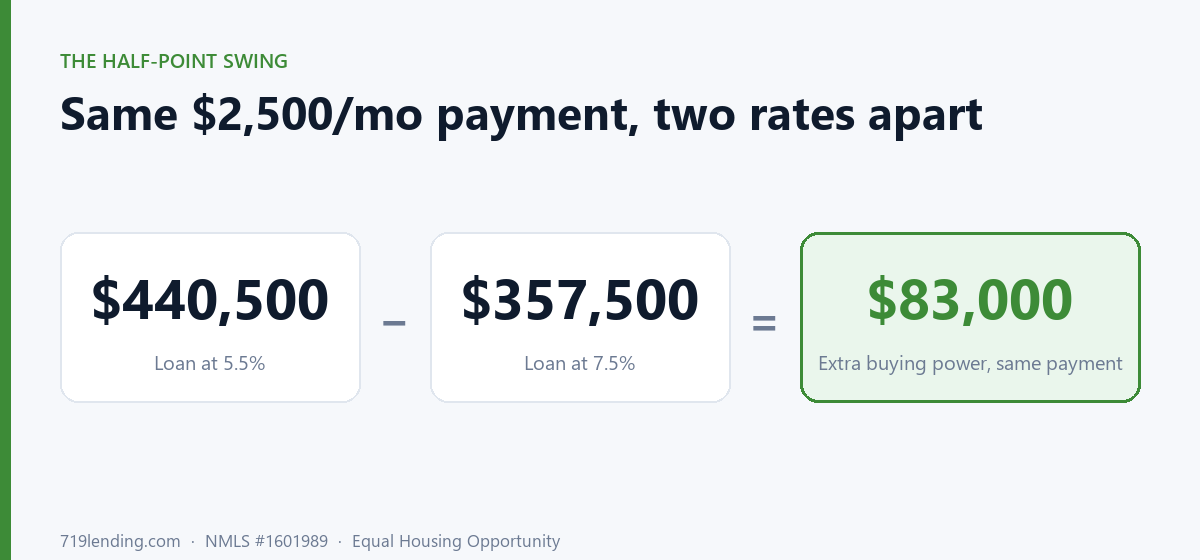

Your monthly payment is fixed in your head, but the house it buys moves every time rates do. The Buying Power calculator maps one payment across nine rates so you can see how much more loan a half-point drop hands you.

Rent vs. buy in Colorado Springs: the calculator that will tell you to keep renting

Last updated: June 30, 2026 — reflects the 2025 standard deduction and $10,000 SALT cap used in the optional tax-effects toggle; verify current figures and confirm specifics with a tax professional.

Rent or buy? The honest answer is a wealth race, not a payment comparison. Our rent vs. buy calculator starts both paths with the same cash, makes the renter invest every dollar they don’t spend on a down payment, counts taxes, insurance, and maintenance that grow as the home appreciates, then finds the exact month buying pulls ahead — or admits renting wins the full 30 years.

Why do most rent-vs-buy calculators secretly favor buying?

Because they cheat. The typical online tool compares a rent check to a mortgage payment and declares buying the winner the moment the payment looks competitive. That quietly ignores two things that decide the entire question.

First, the renter’s money. A buyer sinks a down payment plus closing costs into the home. A fair comparison gives the renter that same pile of cash to invest from day one. Second, the carrying costs. Property taxes, homeowners insurance, and maintenance aren’t fixed — they scale up as the home appreciates, and they never build equity. Skip those and ownership looks far cheaper than it is.

Our calculator closes both loopholes. It runs a month-by-month wealth race over 360 months between two paths that start with identical cash: rent and invest, or buy and build equity. That “fairness clause” is the whole point — the model can’t be tilted toward buying, because the renter always invests the surplus too.

How does the calculator actually decide a winner?

It tracks net worth on both sides every single month, then compares.

- Buyer net worth = home value − remaining loan balance − selling costs + any invested surplus. You only get credit for equity you could actually walk away with, because selling costs are subtracted.

- Renter net worth = a compounding investment account that started with the buyer’s down payment and closing costs.

- The surplus rule: whichever path is cheaper in a given month invests the difference. Early on, renting is usually cheaper, so the renter invests more. Later, as rent climbs and the mortgage stays fixed, owning often becomes the cheaper monthly path — and the buyer starts investing the surplus.

The tool then scans backward through all 360 months to find the true break-even: the first month the buyer’s net worth passes the renter’s and stays ahead. If that crossover never happens, it tells you so honestly — “renting stays ahead the full 30-year window” — instead of forcing a buy verdict.

What costs does it count that a quick comparison misses?

Full-cost owner accounting is where the honest math lives. The model includes the line items buyers forget and the ones that grow over time.

| Cost or input | How the calculator treats it |

|---|---|

| Property taxes | Scales with the appreciating home value, not frozen at purchase |

| Homeowners insurance | Also scales with value over time |

| Maintenance | A percentage of the growing home value — the recurring drain renters never pay |

| PMI | Automatic, LTV-banded, and drops off at 80% LTV as you build equity |

| Selling costs | Subtracted from buyer wealth — equity you can’t actually pocket doesn’t count |

| Rent increases | Rent grows each year by the increase rate you set |

| Investment return | The renter’s (and surplus) cash compounds at your expected return |

| Appreciation | Accepts negative values — you can model a flat or falling market |

Because PMI drops at 80% LTV and taxes/insurance/maintenance ride the home’s value upward, the buyer’s monthly cost isn’t a flat line — and neither is the renter’s, since rent climbs every year. The race is genuinely dynamic. Try the rent vs. buy calculator and watch the wealth-over-time chart show both curves crossing (or not).

What is the “cost of waiting,” and why does it matter in Colorado?

Alongside the head-to-head, the tool runs a 3-way “cost of waiting” analysis: what happens if you buy now versus waiting 1, 2, or 3 years. If the home appreciates, waiting has a price — you buy later at a higher value and miss equity. The cards put a dollar figure on it (for example, “waiting 2 years costs $X” — an illustration only; your number depends on the inputs you enter).

But here’s the honest twist most calculators won’t show: if you set appreciation to a negative number, waiting can actually save you money. The tool reports that too. In a soft or uncertain market, “wait and see” isn’t always the wrong move, and a tool that only ever punishes waiting is selling you something.

What inputs do I need, and what do I get back?

You control the full picture: home price, down payment %, interest rate, loan term, annual appreciation (negative allowed), closing costs, HOA, tax/insurance/maintenance/selling percentages, monthly rent, annual rent increase, your expected investment return, and the horizon. There’s also an optional tax-effects toggle (off by default) that models the itemized mortgage-interest and SALT deduction above the 2025 standard deduction, the $10,000 SALT cap, and capital-gains on investment gains.

In return you get a clear verdict — “buying leaves you $X ahead after N years” or “renting leaves you $X ahead” — plus the crossover month, owner cost versus rent, month-1 PMI, the wealth-over-time chart, the cost-of-waiting cards, and a two-sided narrated explanation that talks through both outcomes rather than cheerleading for one.

These are estimates, not a quote. They depend entirely on the assumptions you feed in — especially appreciation and investment return, which nobody can promise. Change those two numbers and the winner can flip.

So when does the honest answer come out “keep renting”?

More often than the industry likes to admit. If you only plan to stay a few years, selling costs can swallow the equity you built. If your expected investment return is high relative to home appreciation, the renter’s invested cash can out-compound the buyer’s equity for a long time. And if appreciation is flat or negative, buying may never catch up inside the 30-year window — and the tool will say exactly that.

That’s the design philosophy: a calculator that’s not afraid to tell you to keep renting is one you can actually trust when it tells you to buy. Run your numbers with your real Colorado Springs rent, price, and timeline, then explore the rest of our mortgage calculators to pressure-test the decision from every angle.

Frequently asked questions

Is it cheaper to rent or buy a home?

It depends on how long you stay, your local appreciation rate, and what your cash could earn invested instead. Our calculator runs a month-by-month wealth race that starts both paths with the same cash, forces the renter to invest the difference, and counts every ownership cost — then names the exact month buying pulls ahead, or reports honestly that renting stays ahead the full 30 years. The result is an estimate based on the assumptions you enter, not a quote.

Why does the calculator make the renter invest money?

Fairness. A buyer puts a down payment plus closing costs into the home. To compare honestly, the renter gets that same cash to invest from day one, and whichever path is cheaper each month invests the surplus too. Without this “fairness clause,” a rent-vs-buy tool can be tilted to always favor buying.

Does the calculator count property taxes and maintenance?

Yes. It uses full-cost owner accounting — property taxes, insurance, and maintenance scale up as the home appreciates, PMI drops automatically at 80% LTV, and selling costs are subtracted from buyer wealth so you only get credit for equity you could actually pocket.

What is the “cost of waiting” feature?

It models buying now versus waiting 1, 2, or 3 years. If the home appreciates, waiting has a dollar cost shown on the cards. If you set appreciation to a negative number, the tool honestly reports that waiting can actually save you money in a falling market. These figures are estimates that depend on your inputs.

Will the calculator account for tax benefits of owning?

It can. There’s an optional tax-effects toggle (off by default) that models the itemized mortgage-interest and SALT deduction above the 2025 standard deduction, the $10,000 SALT cap, and capital-gains on investment gains. Results are estimates and not tax advice — confirm specifics with a tax professional.

Try the rent vs. buy calculator with your own numbers, or browse the full set of 719 Lending mortgage calculators.

Calculator results are estimates only and depend on the assumptions you enter.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Related Posts