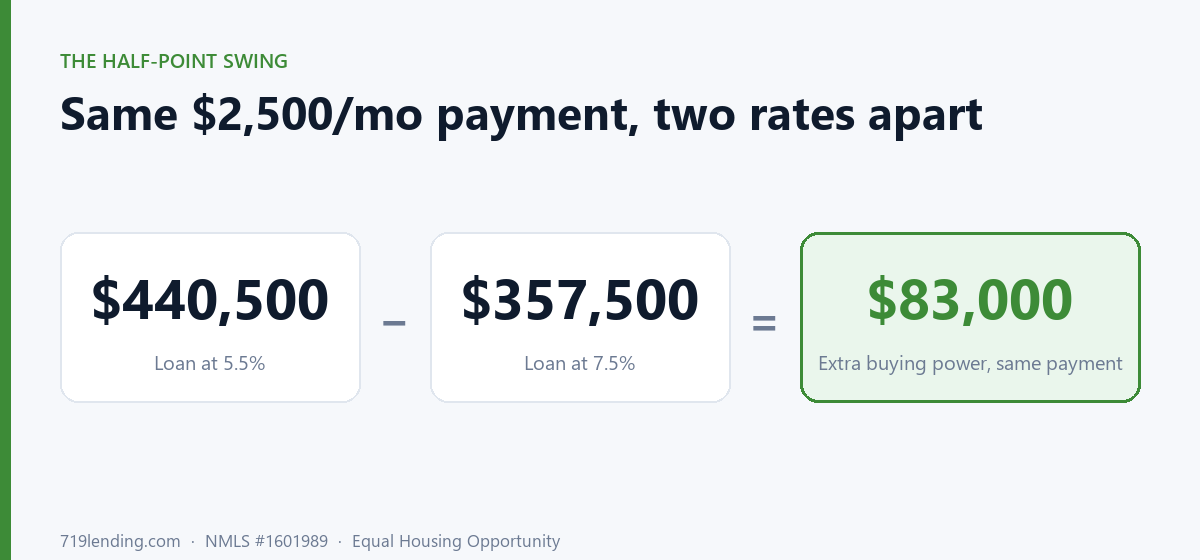

Your monthly payment is fixed in your head, but the house it buys moves every time rates do. The Buying Power calculator maps one payment across nine rates so you can see how much more loan a half-point drop hands you.

How to compare mortgage offers (the cheapest rate usually isn’t the winner)

Last updated: July 1, 2026 — program figures (FHA 1.75% upfront MIP, USDA 1% guarantee fee, VA funding-fee tiers, PMI 78% LTV cutoff, FHA MIP 132 months) are general and current as of this date; confirm current figures and your own quotes with a 719 Lending loan officer.

The cheapest rate isn’t automatically the winner, and the lowest payment is usually the most expensive loan you can pick. The right way to compare mortgage offers is by true cost over the exact number of years you’ll actually keep the loan: cash to close, plus every payment made, minus the equity you build. Whichever offer is cheapest at your horizon wins, not the one with the prettiest rate.

That single idea is what most rate shopping gets wrong. You see two offers, one with a lower rate, one with a lower payment, and there’s no clean way to tell which one leaves more money in your pocket. The Purchase Comparison calculator exists to settle that argument with math instead of gut feel.

Start with a Loan Estimate, then look at the four buckets

The fastest way to compare lenders honestly is to insist on a Loan Estimate (LE) from each one. One lender might hand you a spreadsheet, another an old “good faith estimate,” another a made-up fee worksheet — and you cannot compare a new form to an old form to a made-up form. The LE is the same standardized, three-page form for everyone, generated straight from the lender’s system, so you can finally compare apples to apples. (The CFPB explains the Loan Estimate.)

Once you have it, your Colorado closing costs fall into four buckets — and only one of them is actually a lender-to-lender comparison. The other three are either fixed no matter who you use, or fully in your control.

Bucket 1: What it simply costs to buy a house (~$4,500 in Colorado)

Credit reports, the appraisal, title fees, transfer taxes, and recording fees. These are pass-through costs — a lender generally cannot legally mark them up — so they are roughly the same no matter who you use, averaging around $4,500 for a typical Colorado home (more on a pricier one). If one lender’s credit report is $150 and another’s is $40, you will usually find the appraisal runs a little higher on the cheaper one. It washes out. Do not shop on these.

Bucket 2: What the bank charges for your rate — Box A (the real comparison)

This is the one that matters. Box A on the Loan Estimate is what the bank is charging you to deliver that specific rate and loan. Put two Loan Estimates side by side at the same rate and the same down payment: if Box A says $2,000 on one and $4,000 on the other, that $2,000 gap is the real difference — full stop. Everything else on the estimate can be manipulated right up until the end, so Box A is where you compare. Be crystal clear on that.

Here is what Box A actually looks like. On page 2 of a Loan Estimate, Box A is the top-left box, “A. Origination Charges.” It lists exactly what this lender charges to give you this rate and loan. Here is a real example:

| A. Origination Charges (Box A) | Amount |

|---|---|

| 0.25% of loan amount (points to buy down the rate) | $405 |

| Application fee | $300 |

| Underwriting fee | $1,097 |

| Total — Box A | $1,802 |

That $1,802 is the number that actually compares. Points buy down your rate, and the application and underwriting fees are the lender’s own charges. Line up two Loan Estimates at the same rate and the same down payment, compare each one’s Box A total, and you will see immediately which lender is charging more to deliver the identical loan — no matter what the rest of the estimate says.

Bucket 3: Your escrows — taxes and insurance (you control this)

Your escrow account funds property taxes and homeowner’s insurance, and the lender collects about two months of reserves for each at closing. This is not a lender comparison — it is yours to control. You choose the insurance (a high vs. low deductible, an older home that is expensive to insure vs. a newer one that is not), and the property tax depends on the home you buy. Different lenders will show similar numbers here.

Bucket 4: The day of the month you close (you control this)

This one surprises people. You prepay interest for the days you own the home during your closing month, and you generally skip the very next month’s payment. Close on the 1st and you prepay about 30 days of interest; close on the 30th and you prepay about one day. Here is why: mortgage interest is paid in arrears. Close on July 30, skip August, and your September payment covers all of August’s interest — but you still owned the home for that one day in July, so that single day’s interest is due at closing. Close on the 1st and you owe nearly the whole month up front. Depending on the loan, that timing can swing your cash-to-close by $1,000 to $3,000. It is real money — but it is the calendar, not a lender comparison.

Our take: when you compare lenders, do not get distracted by title, taxes, insurance, or days of interest — buckets 1, 3, and 4 are roughly the same everywhere or they are yours to control. Some lenders lowball those buckets so their page-1 “Estimated Closing Costs” total looks smaller; that is the manipulation. Line up two Loan Estimates at the same rate and down payment, compare Box A, and you will know exactly what each lender is really charging. Then run the finalists through the true-cost math below.

Why is comparing by rate or payment the wrong move?

Because rate and payment each tell you only one slice of the story. A lower rate often costs more up front in points and fees. A lower monthly payment can mean a longer term, more lifetime interest, or mortgage insurance that never goes away. Neither number, on its own, tells you what the loan actually costs you over the time you own the home.

The Purchase Comparison tool builds a full month-by-month amortization for each offer, then plots a “net cost” curve: cash to close, plus all payments made, minus the equity you’ve built so far. Two offers can look nearly identical on the rate sheet and diverge by thousands once you follow those curves out a few years. The cheapest curve at your horizon is the honest winner.

What is the break-even month, and why does it matter?

The break-even month is the exact point where a pricier-up-front, lower-rate loan finally overtakes a cheaper-up-front, higher-rate loan. It’s the moment the two net-cost curves cross.

This is where most “break-even” math is sloppy. The common shortcut divides the extra up-front cost by the monthly savings, which ignores the faster equity a lower rate builds. The Purchase Comparison calculator finds the real crossover by watching for the sign-flip in the actual cost curve (its findCrossover logic) and credits the equity you build along the way. If you’ll sell or refinance before that month, the cheaper-up-front loan wins. If you’ll stay past it, the buydown pays off.

That’s why a buydown of, say, $7,200 in points can be brilliant or a complete waste, and it hinges on one number: the break-even month versus how long you’ll actually own the home. (That $7,200 is just an illustration; your numbers set your own break-even.)

How do I actually compare two offers? (a worked example)

Put both offers in side by side. The default view compares two loans, and you can expand to three. Here’s an illustrative example of how two offers might stack up. These figures are examples only, not quotes.

| Input | Offer A (lower rate) | Offer B (lower cost) |

|---|---|---|

| Purchase price | $450,000 | $450,000 |

| Rate | Lower (bought down) | Higher |

| Discount points paid | $7,200 | $0 |

| Monthly payment | Lower | Higher |

| Cash to close | Higher | Lower |

| Break-even month | Where A’s net-cost curve drops below B’s | |

The verdict depends entirely on your horizon. Stay five years and sell before break-even? Offer B’s lower cash-to-close wins. Stay the full term? Offer A’s lower rate compounds into real savings. The calculator names the winner, the dollars saved, and the break-even month so you’re not guessing. Run your own numbers in the Purchase Comparison calculator and watch the verdict change as you slide the horizon.

What does the calculator do that I’d get wrong by hand?

A lot. The honest-math details are where comparing offers by hand falls apart:

- Mortgage insurance lifecycle by program. Conventional PMI drops off at 78% LTV. FHA MIP runs 132 months at 90% LTV or below, otherwise for the life of the loan. USDA’s annual fee is calculated on the average balance. VA has none. The tool tells you the calendar month each one ends, so a low FHA rate that carries MIP for life can quietly lose to conventional PMI that drops at 78%.

- Auto-financed government fees. FHA’s 1.75% upfront MIP, USDA’s 1% guarantee fee, and the full VA funding-fee tiers get added to the loan automatically, so the comparison reflects what you actually finance.

- Smart escrow estimate. It auto-estimates Colorado property tax (about 0.55%) and insurance (about 0.35%) so payments are realistic, and stops overwriting your numbers once you’ve entered your own.

- Reg-Z actuarial APR. It computes a true APR by bisection, the same actuarial method the disclosure rules use, instead of a rough approximation.

- Tie-awareness. If two offers land within $250, it calls it a tie instead of pretending one “wins” by a rounding error.

- Pay-it-off-early simulator. Add an extra monthly payment and see how many months sooner the loan retires, and how that shifts the comparison.

Why is the lowest payment often the most expensive loan?

Because a low payment can be hiding a longer term, a higher lifetime interest bill, or mortgage insurance that never falls off. The calculator separates categories deliberately: the lowest-payment loan and the cheapest-overall loan are frequently not the same loan. It shows you both so you can decide which one matters for your situation, monthly cash flow or total cost.

It also includes a “best deal by how long you stay” year-range table, so you can see at a glance which offer wins if you keep the home 3 years, 7 years, or the full 30. The winner can genuinely flip by timeline, and seeing that flip is the whole point.

The honest takeaway

Comparing mortgage offers isn’t about hunting for the cheapest rate or the lowest payment. It’s about true cost over the years you’ll actually own the home, with the break-even month doing the heavy lifting. A buydown can be a great deal if you’ll stay past its break-even month and a waste if you’ll move before then. The only way to know your number is to put the offers side by side and follow the cost curves.

That’s exactly what the tool is built for. Try the Purchase Comparison calculator with your real offers, then explore the rest of the lineup on the 719 Lending Calculate hub. Have competing Loan Estimates in hand? Bring them to a 719 Lending loan officer in Colorado Springs and we’ll walk the break-even with you.

Calculator results are estimates for educational purposes and depend on the inputs you provide; your actual rate, fees, and terms will be set by a full application and underwriting.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Frequently asked questions

Should I always pick the mortgage with the cheapest rate? No. A lower rate usually costs more up front in points and fees, so it only wins if you keep the loan past the break-even month, the point where its lower payments and faster equity finally overtake a cheaper-up-front offer. If you'll sell or refinance before then, the offer with lower cash-to-close often costs you less overall. The Purchase Comparison calculator finds that break-even month for you, and its results are estimates based on the numbers you enter.

What is the break-even month on a mortgage comparison? It's the exact month a pricier-up-front, lower-rate loan overtakes a cheaper-up-front, higher-rate loan, the point where their net-cost curves cross. The calculator finds it from the actual cost-curve sign-flip and credits the equity you build, rather than the rough cost-divided-by-savings shortcut that ignores equity.

Why does the calculator say the lowest payment is the most expensive loan? A low monthly payment can hide a longer term, more lifetime interest, or mortgage insurance that never drops off, like FHA MIP that can last the life of the loan. The tool separates lowest payment from cheapest overall cost, because they're often different loans, and shows both so you can choose between monthly cash flow and total cost.

Can I compare more than two loan offers at once? Yes. The Purchase Comparison calculator defaults to two loans side by side and expands to three. Each can use a different loan type (conventional, FHA, USDA, or VA variants), down payment, points, and closing costs, and the tool ranks them by true cost at the horizon you choose.

Are the calculator's results an actual loan offer? No. The results are estimates for educational purposes based on the numbers you enter, including an auto-estimate of Colorado taxes and insurance you can override. Your real rate, fees, mortgage insurance, and terms are determined by a full application and underwriting. It is not a commitment to lend, and not all applicants will qualify.

Related Posts