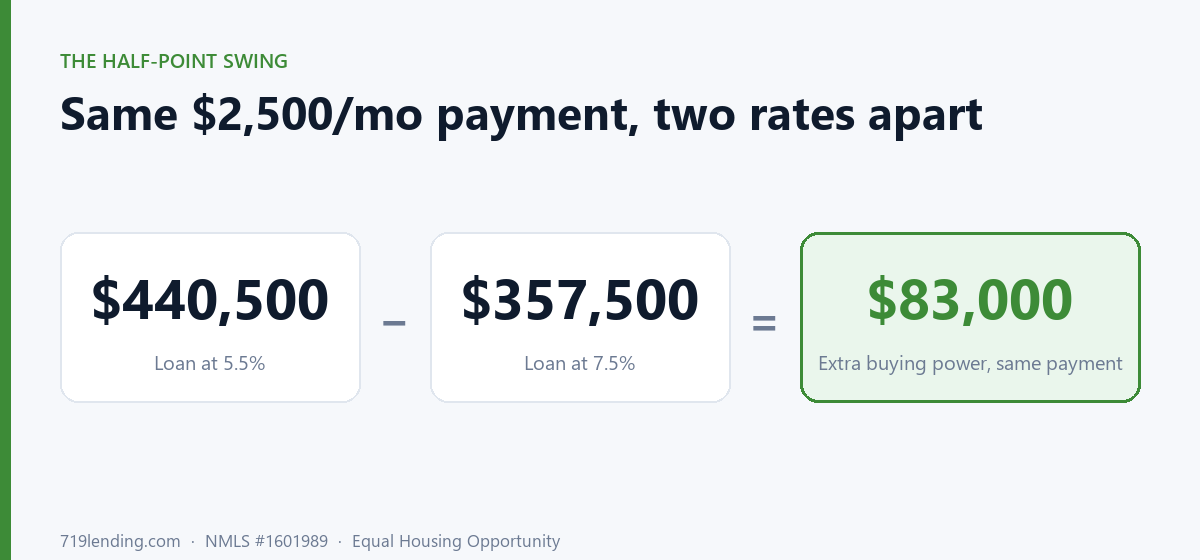

Your monthly payment is fixed in your head, but the house it buys moves every time rates do. The Buying Power calculator maps one payment across nine rates so you can see how much more loan a half-point drop hands you.

How much income do I need to qualify for a mortgage? Run the math in reverse

Last updated: June 30, 2026 — example figures (rates, DTI targets, and required-income outputs) are illustrative and general; confirm current pricing for your scenario.

Most mortgage calculators ask what you make and hand you a home price. The What Do I Need to Make calculator runs the underwriter’s math in reverse: tell it the loan you want, and it estimates the gross (pre-tax) income a lender needs to see, as a monthly and annual figure, live as you drag the sliders. It is an estimate, not a quote.

How does a lender decide how much income I need?

A lender doesn’t start with your dream house and find your income. It starts with your income and caps your payments at a percentage of it. That percentage is your debt-to-income ratio (DTI). Turn the equation around and the question becomes simple: if my total monthly obligations can only be X% of my gross income, how much gross income do I need to carry this specific loan?

That’s exactly what this tool does. You enter the loan you actually want, plus the carrying costs and debts that come with it, and it works backward to the income figure. No guessing at a home price, no reverse-engineering from a payment you saw on a listing.

What numbers does the calculator ask for?

You give it the loan you’re chasing and the costs that ride along with it. Four of these are “levers” the tool encourages you to adjust one at a time so you can watch the required income move.

| Input | Default | What it does |

|---|---|---|

| Loan amount | $450,000 | The mortgage you want, not the home price |

| Interest rate | 6.875% | Drives the principal & interest payment |

| Term | 30 years | Shorter terms demand much more income |

| DTI target | 47% | The share of gross income your debts can consume |

| Other monthly debt | — | Car loans, cards, student loans, etc. |

| Taxes / insurance / PMI / HOA | — | The non-P&I carrying costs, entered per month |

The math is straightforward in concept: build the full housing payment, add the other debts, then divide that total by your DTI target to get the gross income a lender requires. Run your numbers in the What Do I Need to Make calculator and watch the figure update as you move each slider.

What does the default scenario tell me?

Out of the box, the calculator models a $450,000 loan at 6.875% over 30 years with a 47% DTI target. As an illustrative example, that combination requires roughly $7,247 per month in gross income, or about $86,966 per year (these are example outputs, not a quote or a commitment to lend). The tool reads that back as “you’re in the game,” and at a 47% DTI it flags the file as stretched-but-approvable rather than comfortable.

That’s the honest part. A 47% DTI isn’t a disqualifier, but it’s not roomy either, which is why the tool nudges you toward a 36–43% comfort zone.

What is the “honest-math” callout actually warning me about?

Here’s where this calculator earns its keep. Most tools quietly report a DTI percentage and move on. This one translates that back-end DTI into plain language with an amber callout: at a high DTI, it tells you something like “X cents of every gross dollar are spoken for before groceries.” That reframes an abstract ratio into what it means for your actual life. A 47% DTI means 47 cents of every pre-tax dollar is already committed to debt before you buy a gallon of milk.

The calculator also shows a front-vs-back DTI badge so you can see both the housing-only ratio and the all-debt ratio, and it auto-rewrites a “what this means for you” summary as your inputs change. It’s built to talk you toward a sustainable number, not just the maximum a lender might tolerate.

Which levers actually lower the income I need?

The most useful feature is that you can change one variable and immediately see how much income it frees up. Starting from the default $7,247/mo requirement, here’s roughly how each lever moves the number. These are example outputs for illustration, not quotes.

| Change you make | Required gross income (example) |

|---|---|

| Baseline ($450k, 6.875%, 30yr, 47% DTI) | ~$7,247/mo |

| Lower the rate by 1% | ~$6,621/mo |

| Add $50,000 to your down payment | ~$6,548/mo |

| Clear $150/mo of existing debt | ~$6,928/mo |

A couple of patterns fall out of this. Rate and down payment are the heavy hitters. Paying down a small monthly debt helps, but less than people expect. And there’s a clean rule of thumb baked into the engine: every extra $100/mo in carrying cost (higher taxes, insurance, HOA, or PMI) adds roughly $213/mo to the income you need. A shorter term, meanwhile, demands much more income, because you’re compressing the same loan into fewer payments.

Will a shorter loan term really change my required income that much?

Yes, and dramatically. A 15-year term carries the same balance over half the payments, so each monthly payment is far larger, which pushes the required income up steeply. That’s the trade-off behind every “pay it off faster” pitch. The calculator lets you toggle the term and see the income demand jump in real time, so you can decide whether the faster payoff is worth the bigger paycheck a lender will require. One note: if you enter a 0% rate, the math falls back to a straight-line payment, and the tool blocks invalid setups like a DTI of zero or a term of zero rather than returning a broken result.

What do I walk away with?

The calculator returns your required gross income as both a monthly and annual figure, your principal & interest payment, your total housing payment, your front and back DTI, and a six-part donut chart breaking down where every dollar of that payment goes. You can also generate a branded PDF (NMLS #1601989) to take to your agent or keep for your records.

Every figure here is an estimate to help you plan, not a commitment to lend or a pre-approval. The real number depends on your full file, the program, and current pricing. But knowing the ballpark income before you fall in love with a listing is the difference between shopping with confidence and shopping blind.

Try the What Do I Need to Make calculator to see the income behind the house you want, then explore the rest of the tools on our Calculate hub. If you’d rather start from your income and work toward a price, the What Can I Afford calculator runs the math the other direction.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify.

Frequently asked questions

How much income do I need to qualify for a $450,000 mortgage? As an illustrative example, the calculator's default scenario (a $450,000 loan at 6.875% over 30 years with a 47% DTI target) requires roughly $7,247 per month, or about $86,966 per year, in gross pre-tax income. These are example outputs, not a quote. Your actual number depends on your rate, term, DTI target, other debts, and carrying costs. Run your own figures in the What Do I Need to Make calculator for an estimate.

What DTI ratio does the calculator use? It defaults to a 47% back-end DTI target, which it flags as stretched-but-approvable rather than comfortable. The tool nudges you toward a 36–43% comfort zone and shows both your front (housing-only) and back (all-debt) ratios so you can see how much of every gross dollar is already committed.

What's the fastest way to lower the income I need to qualify? Rate and down payment move the number the most. In the example outputs, dropping the rate by 1% lowers the required income to about $6,621/mo, and adding $50,000 to the down payment lowers it to about $6,548/mo. Clearing a small monthly debt helps less, around $6,928/mo for $150/mo cleared. Every extra $100/mo in carrying costs adds roughly $213/mo to the income you need. These are estimates, not quotes.

Why does a shorter loan term require so much more income? A 15-year loan compresses the same balance into half the payments, so each monthly payment is much larger and the income a lender requires rises steeply. The calculator lets you toggle the term and watch the required income jump, so you can weigh a faster payoff against the bigger paycheck it demands.

Is the required income figure a pre-approval? No. Every result is an estimate to help you plan, not a commitment to lend, a quote, or a pre-approval. Your real qualifying income depends on your complete file, the loan program, and current pricing. Use it to shop with a realistic target, then talk to a loan officer for an actual pre-approval.

Related Posts