For those who have selflessly served our nation, the dream of homeownership shouldn’t come with…

Reading an LES for VA Home Loan

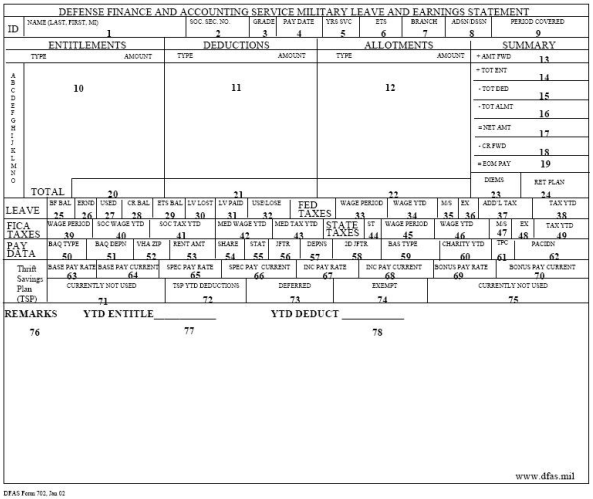

Introduction to Leave and Earnings Statement (LES)

The Leave and Earnings Statement (LES) is the cornerstone of financial management for service members. As the military equivalent of a civilian pay stub, your LES provides a detailed snapshot of your monthly pay, deductions, allowances, and leave balances. This document is essential not only for tracking your income and benefits, but also for verifying your eligibility when applying for loans, including VA home loans.

Service members can access their LES online through secure Department of Defense platforms, making it easy to view, print, and manage their financial information from anywhere. If you need help understanding your LES or have questions about specific entries, you can contact your financial institutions or the appropriate department for assistance. Managing your LES effectively ensures you have the evidence and information needed for important financial decisions, from loan applications to budgeting and beyond.

What Is an LES and Why Does It Matter for VA Loan Qualification?

A Leave and Earnings Statement (LES) is the military equivalent of a pay stub. It details a service member’s monthly pay, deductions, allowances, and leave information. The Entitlement section of the LES lists various types of pay and allowances the service member receives, including Base Pay, Basic Allowance for Housing (BAH), and Basic Allowance for Subsistence (BAS).

Your Leave and Earnings Statement is a monthly snapshot of your military compensation — base pay, allowances, deductions, allotments, and tax withholding. For VA loan purposes, it serves as your primary income verification document. The Entitlement section of the LES lists various types of pay and allowances the service member receives, which ultimately connect to your underlying VA entitlement codes and borrowing limits.

Per the VA Lender’s Handbook Chapter 4, the LES must be no more than 120 days old at closing (180 days for new construction), and must be either an original, an electronic version, or a copy certified as true by the lender. An expired LES is a hard stop — no exceptions. Lenders use the LES to confirm the borrower’s address and verify that income is steady and sufficient to meet monthly obligations.

Accessing Your LES Information Online: Step-by-Step for Service Members

Accessing your Leave and Earnings Statement (LES) online is a secure and efficient way for service members to manage their pay and benefits. To get started, ensure you have your valid ID and password ready. Using your preferred internet browser, go to the official Department of Defense (DoD) website and log in to your account. Once you’ve accessed your profile, navigate to the “My Pay” section—this is where you can view, print, and manage your LES information at your convenience.

If you encounter any issues during the login process or need help navigating the website, assistance is available. Service members can obtain assistance with accessing their account or obtaining a password if needed. You can contact the DoD customer service team by phone or mail for support. Remember, accessing your LES online allows you to stay up to date with your pay details and manage your financial information securely from anywhere.

Reviewing and Verifying LES Information Before Applying

Before you begin your VA loan application, it’s crucial to review and verify your LES to ensure all information is accurate and up to date, and that it aligns with core VA loan eligibility requirements and documentation. Start by checking your pay, allowances, and deductions—these details determine your qualifying income for the VA loan process. Confirm your service history, including your current rank, time in service, and any special pays or allowances that may impact your application.

To access your LES, log in online and select the “LES” option from the menu. Here, you can view your current and previous statements, print them for your records, and ensure all information matches your expectations. If you notice any discrepancies or need help interpreting your LES, contact your servicing pay office or seek assistance online. Taking these steps to verify your LES information helps prevent errors or delays when submitting your VA loan application. Additionally, take actions such as storing your LES securely, avoiding sharing sensitive details over unsecured channels, and monitoring your accounts to protect your personal information throughout the application process.

VA Loan Income from an LES: What Counts and What Doesn’t

Understanding which income components qualify is the foundation of the entire analysis, and fits within the bigger picture of how VA loans work from eligibility to closing. To find your total qualifying income for a VA home loan, add your Base Pay, Basic Allowance for Housing (BAH), and Basic Allowance for Subsistence (BAS) together. Temporary income items like bonuses or hazard pay may only be counted if they are verified to continue. Here’s what underwriters look at:

Base Pay — The Anchor of Your Qualification

Base pay is the most straightforward component. It’s treated as stable and reliable income — unless your Expiration of Term of Service (ETS) date is within 12 months of your projected closing date (more on that below).

One underwriter best practice: divide your Year-to-Date (YTD) gross pay by the number of months worked. If the result doesn’t match your current monthly base pay, it may signal a recent promotion or mid-year pay adjustment. The lender will need to confirm the new rate before using it for qualification.

BAH — Basic Allowance for Housing

BAH is one of the most powerful income components for VA loan qualification, and it’s non-taxable, which means it can be grossed up (see the tax section below).

Key points lenders verify:

- BAH is location-specific. The rate must match your actual duty station — not a generic rate. Lenders should confirm that the BAH matches the new duty station ZIP code before loan approval.

- Dependency status matters. With-dependent and without-dependent rates are different. Your LES must reflect the correct status. An increase in BAH can occur if you relocate or your dependent status changes, which can impact your loan qualification.

- Pending PCS orders change everything. If you have reassignment orders, your lender must use the BAH rate for your future duty station, not your current one. This is the most common LES error in VA loan files.

Missing or incorrect BAH can significantly reduce qualifying income — don’t let your file go to underwriting with an unverified BAH figure.

BAS — Basic Allowance for Subsistence

BAS is also non-taxable and counts as qualifying income. If you receive an annual clothing allowance, it must be converted to monthly income (divide by 12) before it’s applied.

Special and Proficiency Pay (Flight, Hazard, Sea, Linguistic, etc.)

This is where many VA loan files run into trouble. Special pay is only included if it meets two criteria:

- You’ve received it continuously for at least 12 months

- It’s expected to continue based on your assigned duties

If the pay varies (for example, flight pay based on flight hours), the lender will average the most recent 12 months. If it’s new or inconsistent — it’s excluded. Period.

Combat Pay and Imminent Danger Pay

Combat pay may be counted only if it’s expected to continue into the foreseeable future. If the duration is uncertain, it can be used to offset short-term obligations (6–24 months) but cannot be used to qualify your full income. This distinction matters enormously when underwriters calculate your debt-to-income ratio.

The Tax Gross-Up: How Non-Taxable Military Income Gets a Boost

Because BAH, BAS, and certain special pays are non-taxable, the VA allows lenders to gross them up to reflect their equivalent taxable value. The standard method is a 125% gross-up, applied only to the Debt-to-Income (DTI) calculation.

Important nuance: The gross-up is applied to the loan analysis form only — it does not carry over to the residual income worksheet. Non-taxable allowances are used at face value for residual income.

Also worth knowing: a gross-up does not automatically justify a DTI above 41%. VA guidelines require additional scrutiny above that threshold, including meeting 120% of the residual income requirement and/or demonstrating strong compensating factors.

The ETS Date: The 12-Month Rule That Can Sink Your Loan

Every active duty VA borrower’s LES includes an Expiration of Term of Service (ETS) date, which directly ties into your broader VA loan eligibility and entitlement. If your ETS falls within 12 months of your closing date, your income is not considered stable — and the loan cannot proceed as-is.

To overcome this, your lender needs one of the following:

- Re-enlistment or extension documentation

- A valid civilian job offer or verified military retirement income

- A statement of intent to re-enlist plus a Commanding Officer’s statement confirming eligibility and no known reason the extension would be denied

Officer Exception: If your LES shows an ETS of “888888” or “000000,” continuity documentation is not required — unless there is evidence of resignation.

This is a deal-stopper if it catches you off guard. Check your ETS date before you ever apply.

Allotments: The Hidden Liabilities in Your LES

Every allotment line on your LES must be reviewed and categorized. Allotments are not just savings — they can represent debt obligations that must be counted in your DTI calculation.

| Allotment Type | Counts as Debt? |

|---|---|

| TSP / 401(k) Contribution | No — voluntary savings |

| TSP Loan Repayment | Yes — monthly obligation |

| Savings Deposit Program | No — voluntary |

| Family Support / Child Support | Yes — count as debt |

| SGLI (Life Insurance Premium) | No — insurance, not debt |

| Commercial Life Insurance | No — exclude |

| General Loan Repayment | Yes — investigate source |

| Checking/Savings Transfer | No — internal transfer |

| Court-Ordered Payment | Yes — count as debt |

| If an allotment’s purpose is unclear, your lender will request a letter of explanation, supporting bank statements, or documentation identifying the source. A file with multiple unexplained allotments is a red flag that will generate conditions and slow your closing. |

Residual Income: The VA’s Secret Weapon — and Your Benefit as Active Duty

The VA loan program doesn’t just look at DTI — it also requires borrowers to meet a residual income threshold based on family size and geographic region. Residual income is what’s left after all monthly obligations, housing costs, and taxes are paid.

As an active duty service member, you qualify for a 5% reduction in the required residual income threshold. This benefit applies based on your active duty status alone — it is a meaningful advantage that your lender should always apply.

One often-overlooked detail: for residual income calculations, lenders use the state listed on your LES for tax withholding — even if you’re purchasing a home in a different state, and VA’s residual income guidelines by region and family size can significantly influence qualification. The purchase state’s tax rate does not substitute.

Common LES Mistakes

Even the most diligent service members can make mistakes when reviewing or submitting their LES for a VA loan application. Some of the most common errors include missing or outdated information, unverified pay or allowances, and incorrect personal details such as address or dependency status. Failing to confirm these details can result in delays, additional requests for evidence, or even a denied application.

To avoid these pitfalls, always verify that your LES reflects your current pay, allowances, and deductions before submitting it with your loan application. Double-check your service history, dependency status, and any special pays or allotments. If you notice discrepancies or have questions, request assistance from your servicing pay office or contact your lender for clarification. Keeping your LES up to date and accurate is essential for a smooth loan process and helps ensure your application is complete and ready for review.

Red Flags That Underwriters Watch For on a Military LES

Even a clean-looking LES can contain issues that generate conditions, delay closing, or trigger a denial. Here’s what experienced VA underwriters flag immediately:

ETS within 12 months — Income isn’t stable without re-enlistment documentation or a civilian job offer in hand.

Missing or incorrect BAH — The most common LES error. Verify the rate, location, and dependency status before submission.

Pending PCS orders — BAH may shift dramatically. Future duty station rate must be used.

Multiple allotments — Each one needs to be identified. Hidden debts here can push DTI above threshold.

YTD doesn’t reconcile to monthly pay — Could indicate a recent promotion or mid-month enlistment. Confirm before using the higher rate.

New or fluctuating special pay — Excluded if not established for 12+ consecutive months.

Combat pay with unknown end date — Cannot be used for full income qualification; short-term offset only.

Overpayment being recouped — Appears as a deduction. Signals potential financial risk and requires explanation.

DTI over 41% — Triggers enhanced scrutiny. Residual income must hit 120% of the threshold, and compensating factors must be documented.

Negative leave balance — Not disqualifying, but a potential indicator of pending separation or financial distress. Worth a note in the file.

Security and Privacy Protections for Your LES Data

Protecting your LES data is a top priority for both the VA and the Department of Defense. Advanced security measures—including encryption, firewalls, and continuous monitoring—are in place to ensure your information remains confidential and secure. When accessing your LES online, always use a secure internet connection and a trusted device to reduce the risk of unauthorized access. Secure communication methods, such as text messages or email, may be used for password resets or security alerts to help prevent unauthorized access.

To further protect your LES and personal information, create strong, unique passwords and keep your software updated to the latest version. Be vigilant against phishing attempts or suspicious messages that may try to obtain your details. Regularly monitor your account activity for any unusual transactions or changes. If you notice anything out of the ordinary, contact the DoD or VA customer service immediately to safeguard your account and ensure your data remains protected.

DoD Consent Notice: What You Need to Know

When you access DoD computer systems, including the LES website, you are required to acknowledge and accept the DoD Consent Notice. This notice outlines the terms and conditions for using the system, including important security and monitoring protocols. By proceeding, you confirm your understanding and agreement to these requirements, which are in place to ensure the security and integrity of all users’ information.

The DoD may monitor your activity on the website for both security and administrative purposes. Your consent is necessary and required each time you log in. To learn more about the DoD Consent Notice and what it means for your use of the LES website, visit the official DoD website and review the full terms and conditions.

Why LES Analysis Matters More Than Most Borrowers Realize

Most VA-eligible borrowers assume their income is simple because they’re paid by the government. In practice, military income is more complex to document than almost any other borrower type — because it has more moving parts: non-taxable allowances, special pays with continuity requirements, ETS risk, allotment liabilities, PCS order impacts, and residual income overlays.

VA loans offer key benefits for veterans, including no down payment required, no private mortgage insurance (PMI), and typically lower interest rates compared to conventional loans. Veterans can reuse their VA loan benefits multiple times, access favorable loan terms with flexible credit requirements, and take advantage of refinancing options to lower monthly payments or access cash. VA loans are backed by the government, making it easier for veterans to qualify, and VA-approved lenders provide specialized assistance for military borrowers, especially in markets like Colorado Springs where 2025 VA home loan insights and updates can shape your strategy. The VA loan program also includes options and benefits specifically designed for veterans with disabilities, and there are additional VA entitlement strategies for military couples that can further expand your options.

An LES that’s read correctly can unlock significantly more qualifying income through gross-up treatment and BAH inclusion. An LES that’s misread — or not reviewed carefully before submission — can generate a stack of underwriting conditions, delay your closing, or result in a lower loan amount than you qualify for.

Working with Financial Institutions

Collaborating with financial institutions is a key part of the VA loan process for service members. Whether you’re working with a local bank, credit union, or a specialized mortgage broker like 719 Lending, providing a clear and accurate LES is crucial for determining your eligibility and payment options. Financial institutions rely on your LES to verify your income, manage your debts, and process your application efficiently.

To streamline your experience, use online tools to submit your LES and other required documents securely. If you have questions or need updates on your application, don’t hesitate to contact your lender’s support team for assistance. Many institutions offer both online and in-person support, so you can choose the option that best fits your needs. Staying proactive and responsive helps ensure your loan moves forward without unnecessary delays.

Loan Options

As a service member, you have access to a range of VA loan options designed to fit your unique needs. Whether you’re looking to purchase a new home, refinance an existing mortgage, or explore programs for veterans with disabilities, your LES plays a central role in determining your eligibility and payment terms. VA loans offer benefits like no down payment, competitive interest rates, and flexible qualification standards, making them an attractive choice for many military families.

In addition to VA loans, you may also consider other options such as FHA, Jumbo, or low down payment programs, depending on your financial profile and goals. Each loan type has specific requirements, so it’s important to review your LES and supporting documents carefully before selecting the best option. If you’re unsure which loan is right for you, consult with a VA loan specialist who can help you navigate the application process and maximize your benefits.

Customer Service and Support: Getting Help with Your LES or VA Loan Application

If you need help with your LES or have questions about your VA loan application, there are multiple support options available, including reaching out directly through our 719 Lending contact page. Customer service and support are available Monday through Friday during regular business hours. You can contact the DoD or VA customer service teams by phone, mail, or through their official websites for prompt assistance. For service members, additional support is available through financial counseling and educational resources to help you manage your pay and benefits effectively.

When submitting a request for assistance, be sure to provide all required information, including your name, ID, and contact details, to ensure a quick and accurate response. You can also reach out to your servicing pay office or connect with a VA loan specialist for personalized guidance. Whether you’re managing your LES, submitting an application, or simply have questions, these resources are designed to help you every step of the way.

Working with a VA Loan Specialist Who Gets It Right the First Time

At 719 Lending, we’ve been working with active duty borrowers in Colorado Springs and across the country for over two decades, including many stationed in and around Old Colorado City and central Colorado Springs. We understand the military income analysis inside out — from ETS documentation to allotment review to PCS order management.

If you’re active duty and ready to use your VA benefit, start with a conversation before you start an application, especially if you’re considering options like assuming an existing VA home loan instead of starting from scratch. The right preparation — including a proper LES review — means fewer conditions, faster closings, and more house for your money.

📞 Contact 719 Lending | Colorado Springs, CO 🌐 719lending.com 🏠 Colorado’s 100% Pure VA Mortgage Broker

This article is based on VA Lender’s Handbook, Chapter 4 guidance and applies to active duty borrowers only. Guard and Reserve income analysis follows separate VA guidelines. For current program requirements and individual qualification review, consult a licensed VA loan specialist.

Related Topics: VA loan qualification | military income verification | LES analysis | BAH for mortgage | VA residual income | active duty home buying | Colorado Springs VA loans | ETS date mortgage | military allotments DTI | VA loan Colorado

© 2025 719 Lending Inc. | NMLS# [Your NMLS] | Equal Housing Lender

Conclusion

Understanding and managing your LES is essential for a successful VA loan application and overall financial well-being as a service member. By regularly accessing your LES online, verifying your information, and seeking assistance when needed, you can avoid common mistakes and ensure your application is complete and accurate. Working with knowledgeable professionals and staying proactive throughout the process will help you secure the best loan options and achieve your homeownership goals.

If you have questions or need support, don’t hesitate to contact your financial institution, servicing pay office, or a VA loan specialist. Staying informed and prepared puts you in the best position to manage your finances, complete your application, and take advantage of the benefits you’ve earned through your service.

By 719 Lending | Colorado Springs, CO | Colorado’s VA Loan Specialists

If you’re active duty military and applying for a VA home loan, your Leave and Earnings Statement (LES) is the single most important income document in your file. This guide is for active duty service members who want to maximize their VA home loan benefits by understanding how lenders interpret their LES. Understanding your LES is crucial because it directly impacts your ability to qualify for a VA loan, affects your borrowing power, and helps prevent delays or denials during the mortgage process. Unlike a standard W-2 borrower who submits pay stubs and tax returns, your LES replaces the traditional Verification of Employment — but only if it’s read correctly. This guide breaks down exactly how underwriters analyze every line of your LES, what income counts, what doesn’t, and the red flags that can slow down or kill your closing.

Related Posts