VA Loan Entitlement Options for Military Couples Are you and your spouse both serving—or have…

How VA Loans Work

How VA Loans Work: A Comprehensive Guide

How VA Loans Work

Summary of How VA Loans Work*: VA loans, issued by private lenders and guaranteed by the Department of Veterans Affairs (VA), offer eligible veterans and active-duty service members the opportunity to finance a home without a down payment or mortgage insurance. In this comprehensive guide, we will explore the intricacies of VA loans and provide valuable insights to help you navigate the process, including the benefits of a competitive interest rate.

1. Introduction to VA Loans

How VA Loans Work: A VA home loan is a mortgage option designed specifically for veterans, active-duty service members, and eligible family members. These VA mortgage loans are issued by private lenders and guaranteed by the Department of Veterans Affairs (VA), offering borrowers several unique benefits. VA loans provide an opportunity to finance a home without a down payment or mortgage insurance, making homeownership more accessible for those who have served our country.

1.1 What is a VA Loan?

A VA loan is a mortgage guaranteed by the Department of Veterans Affairs (VA) that offers exclusive benefits to eligible servicemembers, Veterans, and their eligible surviving spouses. The VA loan program is designed to help these individuals achieve homeownership with favorable terms, such as no down payment requirements and lower interest rates. To be eligible for a VA loan, borrowers must meet the VA’s service requirements and obtain a Certificate of Eligibility (COE).

2. Eligibility for VA Loans

To qualify for a VA loan, you must meet certain eligibility requirements, which are part of the VA loan benefits. These include serving a minimum period of active duty, being a veteran, National Guard member, Reserve member, or a surviving spouse of a service member. The duration of service and discharge status will determine your eligibility. Obtaining a Certificate of Eligibility (COE) from the VA is necessary to prove that you qualify for a VA loan. VA loans can also help homeowners utilize their home equity to access cash for various financial needs, such as paying off debt or funding home improvements.

The VA Loan Process: Step-by-Step Guide to Competitive Interest Rates

Your VA loan can offer several advantages over conventional mortgages, including no down payment requirement, no mortgage insurance, competitive va loan interest rates, and lower va home loan closing costs. These benefits make VA loans an attractive option for veterans and active-duty service members who want to become homeowners.

4. VA Loan Process: Step-by-Step Guide

Understanding how a VA loan works is essential for a smooth homebuying experience. The VA loan process consists of several steps, including prequalification, preapproval, finding the perfect home, VA appraisal and underwriting, and closing the loan. Familiarizing yourself with how does the VA loan work can help you navigate the process more effectively.

4.1 Prequalification

The first step in the VA loan process is to find a VA lender and get prequalified. Prequalification provides an estimate of how much house you can afford based on your income, credit, and other financial factors. It sets the foundation for the next crucial step: VA loan preapproval, which is a key part of learning how to apply for a VA home loan.

4.2 Preapproval

Loan preapproval puts you in a strong position as a buyer. Lenders will verify your income, financial information, and credit history to determine your purchasing power. Once preapproved, you will receive a preapproval letter, which demonstrates to real estate agents and sellers that you are a serious buyer.

4.3 Finding the Perfect Home

With preapproval in hand, you can confidently search for a home that meets your needs. It’s important to work with a VA loan-savvy real estate agent who can guide you through the process and ensure the properties you consider are eligible for VA loans.

4.4 VA Appraisal and Underwriting

Once you find a home and have an accepted offer, your lender will order a VA home appraisal of the property. This VA appraisal is not a home inspection but a requirement to ensure the property meets fair market value and the VA’s minimum property requirements. Concurrently, underwriters will evaluate your financial documents, including the va home appraisal, to determine if the loan can be approved.

4.5 Closing the Loan

The final step is the loan closing. You will sign legal documents and paperwork, and the keys to your new home will be handed over. It’s essential to review all the details carefully and ensure everything is in order before completing the closing process.

Please note that this page contains links leading to external websites. The Department of Veterans Affairs does not endorse or take responsibility for the content found on those sites. This is an external link disclaimer.

4.6 Contact a Lender to Get Started

Once you have determined your eligibility for a VA loan, it’s time to contact a lender to get started on your application. A VA-approved lender can guide you through the process and help you understand the requirements and benefits of a VA loan. Be sure to compare offers from multiple lenders to find the best interest rate and terms for your situation. Additionally, be prepared to provide proof of employment, income, and other financial information to support your loan application.

5. VA Loan Facts You Should Know

While the VA loan process may seem familiar, there are several lesser-known facts about VA loans that borrowers should be aware of. These facts can help you make the most of your VA loan benefit. Let’s explore some of these important facts, including what is a VA loan and the benefits of the VA home loan.

- Cash-Out Refinance Loans: A cash out refinance loan allows homeowners to access their home equity and use the funds for various needs, such as debt consolidation, education funding, or home improvements. This option is also beneficial for eligible veterans when used in conjunction with VA loans.

- Streamline Refinance Loans: The streamline refinance loan, also known as the VA Interest Rate Reduction Refinance Loan (IRRRL), allows veterans to lower their interest rate and potentially reduce their monthly mortgage payments by refinancing their existing VA home loan.

5.1 Reusability of VA Loans

One of the significant advantages of the VA home loan program is its reusability. You can use your full VA entitlement multiple times as long as you pay off the loan each time. Even if you have lost a VA loan to foreclosure or currently have one, you may still be able to obtain another VA loan.

5.2 Property Eligibility for VA Loans

VA loans are primarily designed for properties in ‘move-in ready’ condition. They are typically suitable for single-family homes, condos, modular housing, and some multi-unit properties. However, they may not be suitable for certain types of properties such as working farms or fixer-uppers.

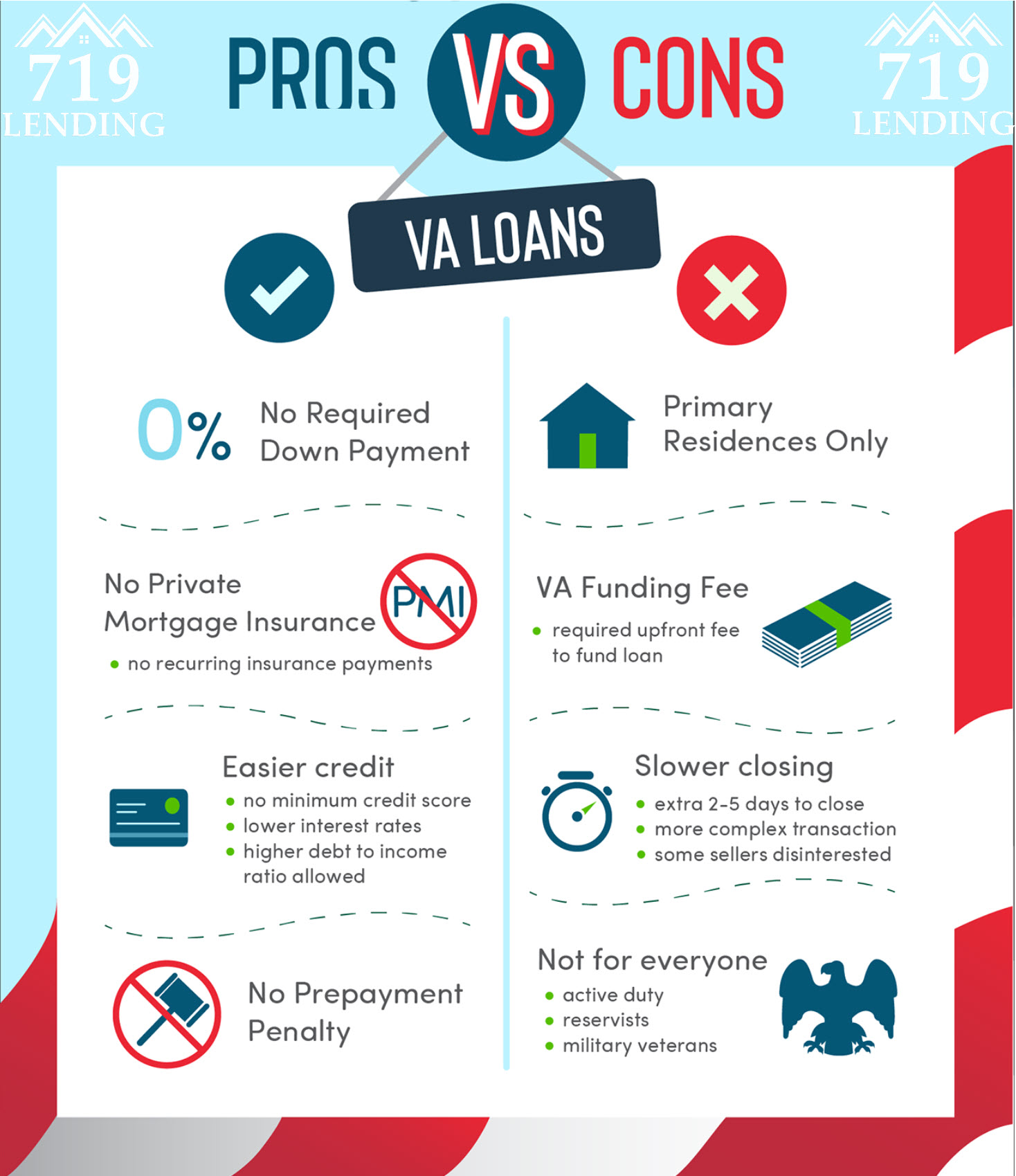

Primary Residence Requirement for Active Duty Service Members

VA loans are exclusively for primary residences. They cannot be used to purchase investment properties or vacation homes. However, buying a duplex or multiunit property and living in one of the units is allowed.

5.4 VA Loans and Government Guarantees

The VA does not issue home loans directly. Instead, it provides a guaranty on each qualified mortgage loan, which is often referred to as a VA direct loan, reducing the risk for lenders and enabling them to offer favorable terms and rates to borrowers.

5.5 VA Loans and Foreclosure/Bankruptcy History

Even if you have a history of foreclosure or bankruptcy, you may still be eligible for a VA loan. The VA loan program provides options for service members with a troubled financial past.

No Private Mortgage Insurance with VA Loans

Unlike many other loan programs, VA loans do not require mortgage insurance. The VA’s guaranty eliminates the need for this additional expense, allowing borrowers to save money each month.

5.7 VA Funding Fee

VA loans come with a mandatory funding fee. This fee, which helps the VA sustain the loan program, is required on both purchase and refinance loans. However, veterans with service-connected disabilities may be eligible for a waiver of the funding fee, as the va regional loan center can provide further assistance.

5.8 Loan Limits and Borrowing Capacity

There is no limit to how much you can borrow with a VA loan, as long as the lender is willing to provide the loan amount. Veterans with their full entitlement do not have to worry about loan limits or the need for a down payment.

5.9 Prepayment Penalty

VA loans do not have a prepayment penalty. Borrowers can make extra payments anytime, reducing the amount of interest paid over the life of the loan.

6. Types of VA Home Loans

VA home loans come in several types, each designed to meet the unique needs of eligible borrowers. The most common types of VA home loans include:

- Purchase Loans: These loans are used to purchase a primary residence, and they offer favorable terms, such as no down payment requirements and lower interest rates.

- Streamline Refinance Loans: Also known as Interest Rate Reduction Refinance Loans (IRRRL), these loans are used to refinance an existing VA loan, offering a streamlined process with reduced documentation requirements and potentially lower monthly payments.

- Cash-Out Refinance Loans: These loans allow you to refinance an existing mortgage and take out cash from the equity in your home, providing funds for various needs such as home improvements or debt consolidation.

By following this plan, I will ensure that the new sections are informative, engaging, and seamlessly integrated into the existing article.

6. The Best VA Lenders of 2023

Choosing the right lender is crucial when applying for a VA loan. Here are some of the top VA lenders in 2023, and understanding how to use va home loan, how to use va loan, or how to use a va loan can be pivotal in this process:

6.1 719 Lending

Mortgage companies, like 719 Lending, specialize in VA Mortgages and are known for their quick service, strong communication, and customer-first approach. They accept credit scores as low as 500 and offer various loan programs, including VA loans, to accommodate borrowers with lower credit scores.

7. VA Loan Requirements

To discover how to get a VA home loan, you must meet certain requirements. These include a minimum service period, obtaining a Certificate of Eligibility, having a steady employment history, maintaining a good credit score, and staying within VA loan limits. Factors such as residual income, reserve funds, property requirements, and more also influence the eligibility process.

Conclusion

VA home loans offer a significant opportunity for veterans and active-duty service members to achieve homeownership. With benefits like no down payment requirement, absence of mortgage insurance, and competitive interest rates, VA home loans make owning a home more attainable. It’s crucial to understand the VA loan process, eligibility requirements, and important details about VA loans for a successful homebuying journey. One important aspect to note is the VA loan funding fee, a one-time charge paid to the Department of Veterans Affairs, which is utilized to support the VA loan program and mitigate costs associated with borrowers who default on their loans. If you’re eligible for a VA loan, consider partnering with a reputable lender, such as 719 Lending, to realize your homeownership aspirations.

About 719 Lending

719 Lending is a premier mortgage lender located in Colorado Springs, specializing in VA loans and providing a seamless, personalized homebuying experience for veterans and active-duty service members. Our expertise in VA loans and dedication to customer satisfaction set us apart, and we’re also knowledgeable about the Native American Direct Loan program. We strive to make the homebuying process as smooth as possible. To assist prospective homebuyers, 719 Lending offers a comprehensive VA home loan buyer’s guide. Visit our websitewww.719lending.com, to learn more and start your journey towards homeownership.

References

- Reference Article 1: A VA loan is a $0-down mortgage option issued by private lenders and partially backed, or guaranteed, by the Department of Veterans Affairs (VA). Eligible borrowers can use a VA loan to purchase a property as their primary residence or refinance an existing mortgage.

- Reference Article 2: Military service members and veterans earn many special benefits, but one of the most useful is eligibility for a VA loan. This mortgage program features lenient credit requirements and allows buyers to finance a home without a down payment or mortgage insurance.

Related Posts