Your Social Security check is worth more than its face value when you buy a house. Lenders are allowed to "gross up" tax-free income, but the rule changes by loan program and most online calculators get the FHA math wrong. Here is how it actually works.

Why your $95K salary qualifies as $78K: how lenders calculate W-2 income

Last updated: June 30, 2026 — figures, gross-up percentages, and DTI guidance are illustrative general examples; confirm current agency rules and your qualifying number with a licensed loan officer.

A mortgage underwriter rarely counts your full salary. For W-2 wage earners, lenders calculate base pay three ways and use the lowest defensible figure, then hold bonus and overtime to their weakest year and net commission against tax write-offs. That math can turn a $95,000 salary into roughly $78,000 of qualifying income (an illustrative example). Our W-2 income calculator runs that exact logic so you see the real number first.

Why doesn’t a lender just count my full salary?

Because conservative Fannie Mae, Freddie Mac, FHA, and VA wage-earner rules don’t ask “what do you make?” — they ask “what can we safely count for the life of this loan?” Those are different questions.

For your base pay, the calculator computes income three ways and lets the lowest one win:

- Your current pay rate — salary, or hourly multiplied by your hours.

- Your year-to-date pace — YTD gross divided by the exact days elapsed (÷30.44 per month), so it’s measured by real dates, not rounded months.

- Last year’s W-2 — Box 1 divided by 12.

The tool shows all three candidates on a base-pay card with a “counted” badge on whichever one is lowest. No hidden math — you see which number won and why.

An example: the $95K salary that counts as $78K

Say you earn a $95,000 salary ($7,917/mo on paper), but you started mid-year, took unpaid leave, and last year’s W-2 reflected a lower role. Here is how the three candidates might shake out (illustrative numbers):

| Base-pay candidate | Monthly figure | Counted? |

|---|---|---|

| Current pay rate ($95K salary) | $7,917 | No |

| YTD pace (by exact dates) | $6,900 | No |

| Last year’s W-2 Box 1 ÷ 12 | $6,500 | Yes — lowest |

Anchor to the lowest and you’re qualifying on about $78,000 a year, not $95,000. It feels harsh, but it’s the same rule every underwriter applies — better to know it now than at the closing table.

Why would one year of bonus count as $0?

Variable income — bonus, overtime, and “other” pay — has to prove it’s stable and likely to continue. The rules want a two-year track record. So the calculator includes a two-year-history guard: if you can only document one year of bonus or overtime, it counts that income as $0 and raises a warning. One good year isn’t a trend; it’s a data point.

When you do have the history, variable income still gets the conservative treatment. The tool takes the minimum of three figures: your YTD pace, your recent year divided by 12, and your prior year divided by 12. The practical effect is important — if your bonus is shrinking year over year, that declining trend pulls your qualifying number down, not up. Lenders won’t average a falling line and call it stable.

How does commission shrink after my tax write-offs?

This one surprises commission earners every time. If you write off unreimbursed business expenses on IRS Form 2106, those write-offs come straight back out of your qualifying commission. The calculator nets commission against 2106 expenses and floors the result at $0 — it can reduce or zero out your commission, but it never goes negative.

The logic is consistent: for tax season you wanted those expenses to look as large as possible to lower your tax bill. For a mortgage, the IRS already knows your “real” take-home was lower, so the underwriter uses that lower figure. You can’t have it both ways. The same applies to unreimbursed business expenses across the file — they’re subtracted from the total before a qualifying number is set.

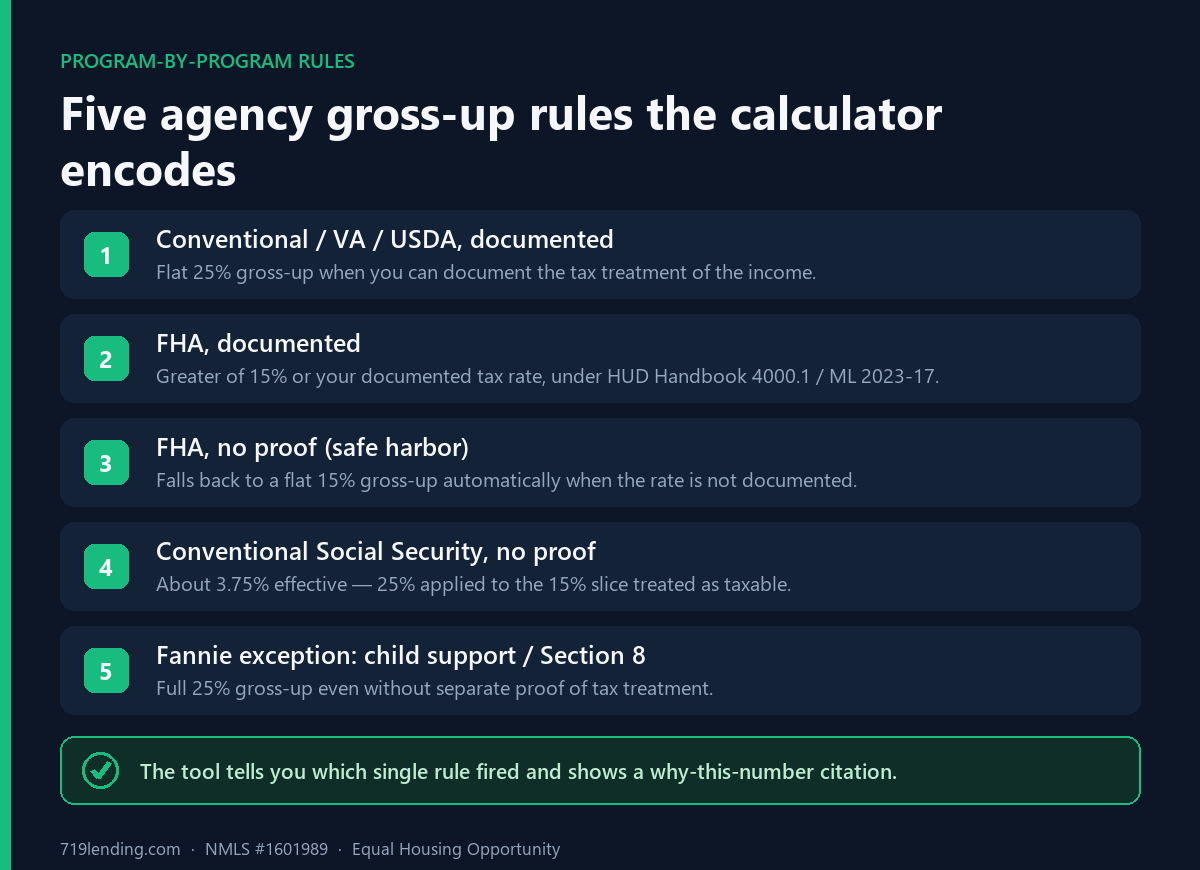

Why is a tax-free dollar worth 25% more?

Non-taxable income — certain Social Security or other tax-free sources — can be “grossed up” because a tax-free dollar goes further than a taxed one. The calculator applies a 25% gross-up, but only when you check the box confirming you can document it. No documentation, no gross-up. That gate keeps the estimate honest rather than inflating a number you can’t back up.

What do the underwriter flags actually tell me?

The tool runs a live underwriter-flag panel as you type, surfacing the exact issues a human underwriter would raise:

| Flag | What triggers it |

|---|---|

| Declining trend | Variable income falling year over year (shown as a %) |

| High volatility | Income swinging more than 25% between periods |

| Heavy commission expenses | 2106 write-offs exceeding 50% of commission |

| Limited data | Less than the two years of history the rules expect |

| Missing docs | A gross-up or income type claimed without documentation checked |

| High expenses | Unreimbursed business expenses materially cutting income |

A clean file shows no flags. A flagged file tells you exactly what to fix — or what to expect — before you sit down with a lender.

How does this connect to my DTI?

Qualifying income is only half the equation; the other half is debt-to-income ratio. Once the calculator settles your qualifying monthly income (never below $0) and your annualized total, it translates that into roughly how much monthly debt a ~45% DTI can support. That’s the bridge between “what counts as income” and “what house payment fits.” It pairs naturally with our full suite of mortgage calculators for affordability and payment scenarios.

What you’ll need to run your own numbers

The calculator handles a single scenario with a transparent, three-way internal comparison on base pay. Have these ready:

- Which income types apply (base, bonus, overtime, commission, other, non-taxable)

- Base pay — hourly rate plus hours, or annual salary

- YTD gross and the pay-period dates

- Recent and prior W-2 Box 1 amounts

- Bonus / OT / other YTD plus months, and recent and prior totals

- Commission gross and any Form 2106 expenses

- Non-taxable amounts with the documentation checkbox

- Unreimbursed business expenses

You’ll get a single qualifying monthly income plus the annualized figure, a per-source breakdown, the base-pay card showing all three candidates and which one counted, the underwriter warnings, and the ~45% DTI debt supported. These results are estimates for planning — a licensed loan officer confirms the final figure against your full documentation.

Ready to see your real qualifying number? Run your numbers in the W-2 income calculator and find out whether your file is clean or flagged before you ever fill out an application. When you’re done, try the W-2 income calculator alongside the rest of our tools to build the full picture.

719 Lending Inc., NMLS #1601989 · Equal Housing Opportunity · This article is educational only, is not a commitment to lend, and not all applicants will qualify. 719 Lending is not affiliated with or endorsed by any government agency.

Frequently asked questions

Why does my $95,000 salary qualify as less? Underwriters calculate base pay three ways — your current pay rate, your year-to-date pace, and last year's W-2 Box 1 divided by 12 — and use the lowest defensible figure. If your YTD pace or last year's W-2 is lower than your stated salary (from a mid-year start, leave, or a prior role), that lower number anchors your qualifying income. The calculator shows all three candidates and badges the one that counts. The $95K-to-$78K figure is an illustrative example.

Why does one year of bonus or overtime count as $0? Variable income needs a two-year track record to be considered stable and likely to continue. The calculator's two-year-history guard counts bonus, overtime, or other variable pay as $0 with a warning when you can only document one year. With a full history, it still uses the minimum of your YTD pace, recent year, and prior year — so a declining trend lowers the number.

How does commission get reduced by Form 2106? Unreimbursed business expenses you claim on IRS Form 2106 are netted against your commission income, floored at $0. The write-offs that lowered your tax bill also lower the commission an underwriter will count. The calculator subtracts them automatically and never lets the result go negative.

Why is non-taxable income grossed up 25%? A tax-free dollar stretches further than a taxed one, so certain non-taxable income can be grossed up by 25%. The calculator applies this only when you check the box confirming you can document the income, keeping the estimate honest rather than inflating a number you can't support.

Are the calculator's results final? No. Every result is an estimate for planning, including the ~45% DTI debt-supported figure. A licensed 719 Lending loan officer confirms your actual qualifying income against your full documentation. Not all applicants will qualify.

Related Posts