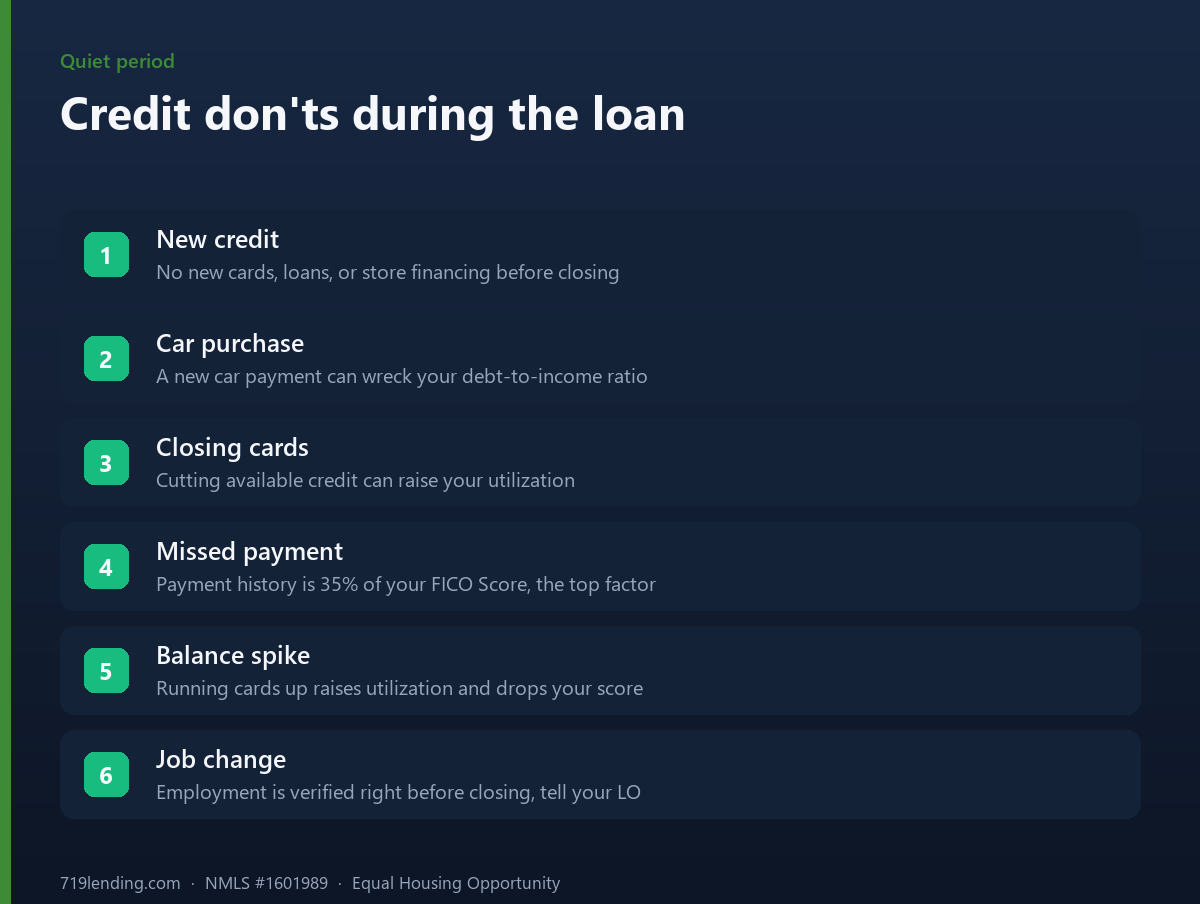

The credit dos and don'ts between mortgage application and closing. Protect your loan during the quiet period: keep balances low, pay on time, don't open new credit.

How Student Loans Affect Qualifying for a Mortgage

Student loans affect qualifying for a mortgage almost entirely through your debt-to-income (DTI) ratio, and each loan program counts a deferred or $0-payment loan differently. Your credit score matters too, but the bigger swing usually comes from how much monthly student-loan payment the underwriter is required to assume you owe. That assumed payment can be your real payment, a percentage of your balance, or in some cases zero, depending on whether you use a Conventional, FHA, VA, or USDA loan. When you carry a large deferred balance, the program you choose can change your qualifying DTI dramatically, even though nothing about your actual life has changed.

This guide walks through what DTI is, how each program treats student debt today, and what you can document to lower the payment an underwriter counts against you. The rules below were updated across 2021 through 2023 and continue to shift as federal repayment plans change, so treat every figure as general and confirm the current version with a lender before you rely on it.

Why DTI is where student loans hit hardest

Debt-to-income ratio is the share of your gross monthly income consumed by required debt payments, including the new mortgage. Lenders look at it because it is one of the strongest signals of whether you can absorb a house payment. The Consumer Financial Protection Bureau explains that your debt-to-income ratio is one way lenders measure your ability to manage monthly payments, and in the broader market a DTI at or below 43% is a commonly cited benchmark above which qualifying often gets harder.

Here is the mechanic that trips people up. When your student loans are deferred, in forbearance, or on an income-driven plan showing a $0 payment, you might expect underwriting to count $0. Most programs do not. Instead they substitute a placeholder payment, because a $0 payment today is temporary and the underwriter has to plan for the day it resets. That placeholder is where the programs diverge, and where a broker can help you shop the treatment.

How each mortgage program counts a student loan payment

Every program starts from the same place: if your credit report or loan statement shows a real monthly payment above zero, that is usually the number used. The differences appear when the reported payment is $0 or the loan is deferred. The table below summarizes the current agency rules. Percentages are of the outstanding balance unless noted.

| Program | Payment above $0 on credit | If payment is $0 / deferred / non-amortizing |

|---|---|---|

| Conventional (Fannie Mae) | Use the reported payment | 1% of balance, or a documented fully amortizing payment; documented $0 on an income-driven plan may be used |

| Conventional (Freddie Mac) | Use the reported payment | 0.5% of balance when the reported payment is $0 |

| FHA | Use the reported/documented payment | 0.5% of the outstanding balance when the reported payment is $0 |

| VA | Greater of the reported payment or 5% of balance ÷ 12 | Excluded if deferred at least 12 months beyond closing |

| USDA | Fixed documented amortizing payment, if provable | Greater of 0.5% of balance or the reported payment |

Conventional loans: Fannie Mae and Freddie Mac differ

The two conventional rulebooks are not identical, which surprises many borrowers. Fannie Mae’s Selling Guide B3-6-05 says that if a monthly student loan payment is provided on the credit report, the lender may use that amount. If the report shows $0 or no payment, and the loan is deferred or in forbearance, the lender may calculate a payment equal to 1% of the outstanding balance or a fully amortizing payment using the documented repayment terms. If you are on an income-driven plan and can document that the actual payment is $0, Fannie Mae permits qualifying with that $0.

Freddie Mac is friendlier on the placeholder. Its Seller/Servicer Guide directs that when the reported payment is $0, the seller must use 0.5% of the outstanding balance unless other documentation supports a different payment greater than zero. On a large balance, the gap between Fannie’s 1% and Freddie’s 0.5% is real money in your ratio, which is one reason a broker who can place a loan with either investor is useful.

FHA loans

FHA changed its rule in 2021. Under HUD Handbook 4000.1, as revised by Mortgagee Letter 2021-13, the lender uses the payment amount reported on the credit report or the actual documented payment when that amount is above zero. When the monthly payment reported on the borrower’s credit report is zero, the lender uses 0.5% of the outstanding loan balance. This replaced the older 1% placeholder and made FHA meaningfully more forgiving for borrowers with large deferred balances.

VA loans

VA uses a different math. Per the VA Lender’s Handbook, the counted payment is the greater of the payment on the credit report or 5% of the loan balance divided by 12. On a $60,000 balance that 5%-divided-by-12 figure is $250, which is often higher than a real income-driven payment, so VA is not automatically the softest option. The important VA carve-out: if the borrower provides written evidence that the student loan will be deferred at least 12 months beyond the closing date, no payment needs to be counted at all.

USDA loans

USDA’s Handbook HB-1-3555 lets you use a fixed, fully amortizing payment if you can document that the interest rate, term, and payment are all fixed. If the payment is not fixed, or the loan is deferred, the lender uses the greater of 0.5% of the outstanding balance or the payment reflected on the credit report. USDA loans also carry income limits and a rural-area requirement, so they are not available to every buyer.

A worked example: the same borrower, four programs

Consider a borrower with a $50,000 federal student loan balance showing a $0 payment because of a deferment. The placeholder payment an underwriter must count varies sharply:

- Freddie Mac and FHA (0.5%): $250 per month.

- Fannie Mae (1%): $500 per month, unless a documented amortizing or income-driven payment is used.

- VA (5% ÷ 12): about $208 per month, or $0 if deferred 12+ months past closing.

- USDA (greater of 0.5% or reported): $250 per month, or a lower fixed amortizing payment if documented.

The difference between $500 and $208 on a single debt can move a borrower from denied to approved. Nothing about the borrower’s real budget changed; only the rulebook did. That is the core reason student loans and mortgage qualifying are so program-sensitive.

The moving target: SAVE, IDR, and the payment restart

Federal income-driven repayment is in flux, and that directly affects the “reported payment” underwriters see. The SAVE plan was found unlawful by the courts, and the U.S. Department of Education has been winding it down and moving borrowers into legal repayment plans, with a new Repayment Assistance Plan (RAP) coming online. Interest on loans that had been sitting in the SAVE forbearance resumed accruing, and servicers are notifying borrowers to exit SAVE and pick a legal plan.

The practical takeaway for a homebuyer: a $0 or artificially low income-driven payment may not stay that way, and an underwriter is required to account for that. If your payment is scheduled to change, most guides tell the lender to use the higher, going-forward figure rather than the temporary one. Because this area keeps changing, treat any specific plan status as “confirm current” and get a fresh loan statement before you apply.

How to document your way to a lower counted payment

You are not powerless here. The counted payment is driven by documentation, and better documentation often produces a lower number. Practical levers include the following:

- Get a current statement showing your real payment. If your credit report shows $0 or an outdated figure, a statement with a true amortizing payment can replace the placeholder in most programs.

- Document an income-driven $0 for Fannie Mae. Fannie permits a documented $0 income-driven payment; Freddie, FHA, and USDA generally do not, so this is a Fannie-specific play.

- Prove fixed, fully amortizing terms for USDA. A fixed rate, fixed term, and fixed payment let USDA use the real payment instead of 0.5%.

- Line up a 12-month deferment for VA. Written evidence of deferment 12+ months beyond closing can remove the payment entirely on a VA loan.

- Compare Fannie versus Freddie on large balances. The 1% versus 0.5% placeholder gap is largest when your balance is high.

Our take: in our experience at 719 Lending, the program you choose can swing your qualifying DTI by hundreds of dollars a month when you carry a large deferred balance, and that swing is often the difference between approval and denial. This is 719’s judgment, not an agency rule: because the treatments differ so much, a broker who can place your loan with Fannie Mae, Freddie Mac, FHA, VA, or USDA can effectively shop the student-loan treatment for you rather than being stuck with whatever a single lender’s overlay dictates.

Beyond DTI: the smaller ways student loans matter

DTI is the headline, but student loans touch qualifying in two quieter ways. First, payment history: on-time student-loan payments build the credit profile lenders price against, and a single missed payment can hurt more than the balance does. Second, credit utilization on your revolving accounts is separate from installment student debt but is scored alongside it, so managing both matters before you apply. Neither of these is unique to student loans, but they compound with the DTI effect.

Frequently asked questions

Do student loans stop me from buying a house? Not by themselves. Student loans reduce how much house you qualify for by raising your DTI, but millions of borrowers with student debt buy homes every year. The question is how large a payment the program counts, not whether the debt exists.

Why does my lender count a payment when my student loans show $0? Because a $0 payment is usually temporary. Deferment, forbearance, and some income-driven plans reset later, so most programs substitute a placeholder, such as 0.5% or 1% of your balance, to plan for that reset. Fannie Mae is the main program that will accept a documented income-driven $0.

Which loan program is best if I have big deferred student loans? It depends on the numbers. FHA and Freddie Mac use a 0.5% placeholder, VA can exclude a loan deferred 12+ months past closing, and USDA can use a documented fixed payment. There is no universal winner, which is exactly why comparing programs helps.

Can I qualify with a $0 income-driven payment? On a conventional Fannie Mae loan you may, if you document that the actual income-driven payment is $0. FHA, USDA, and Freddie Mac generally will not count $0 and will use a percentage-of-balance placeholder instead. Confirm current rules with your lender.

How do the SAVE plan changes affect my mortgage application? The SAVE plan is being wound down and borrowers are moving to other repayment plans, so a $0 or very low payment may rise. Underwriters may use the higher going-forward payment, so pull a fresh statement before applying and treat plan status as something to confirm at the time.

Should I pay off my student loans before applying for a mortgage? Sometimes, but not always. Paying a loan to $0 removes its counted payment, but so can paying it down enough to lower the placeholder or documenting a lower real payment. Cash used to pay debt is cash not available for down payment and reserves, so run the trade-off with a loan officer first.

This article is general education from 719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, endorsed by, or acting on behalf of the FHA, VA, USDA, HUD, or any government agency. All rates, percentages, and thresholds described here are general, subject to change, and lender and investor overlays may apply; confirm current guidelines and your specific numbers with a licensed loan officer before relying on them. Last updated: June 2026.

Related Posts