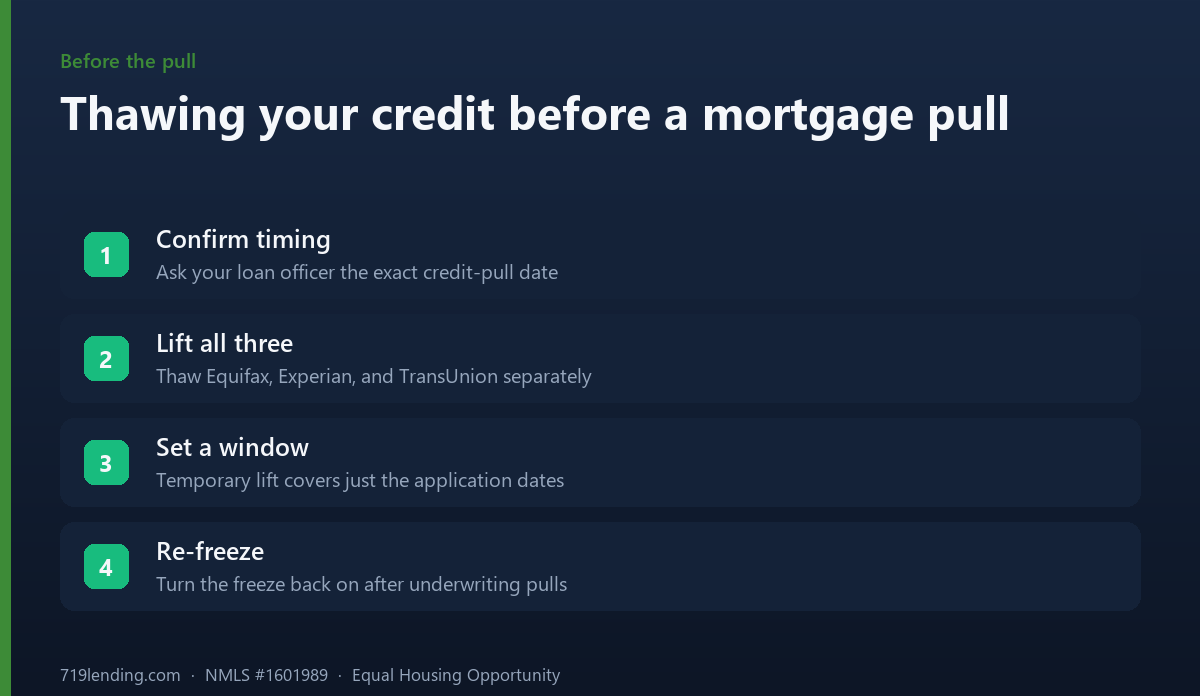

A security freeze blocks your mortgage credit pull at that bureau, so you must thaw all three before a tri-merge. Fraud alerts don't block a pull. How and when to lift.

Buying a House After Divorce: Untangling Joint Credit

Buying a house after divorce is possible, but a divorce decree alone does not untangle your joint credit — you stay legally liable to the original lender on every joint account until it is refinanced, assumed, closed, or the creditor formally releases you. That gap between what the decree says and what your creditors can still do is the single most misunderstood part of buying after divorce. A judge can order your ex to pay the car loan or the old mortgage, but the credit card company, the auto lender, and the servicer were never parties to your divorce — their contract with you is untouched. If your ex pays late, that late payment can still land on your credit report and follow you into a new loan application. This guide walks through why that happens, how mortgage underwriters actually treat assigned debts and support payments, and the concrete steps to separate your credit before you shop.

Why a divorce decree does not release you from your creditors

A divorce is a legal event between two spouses. It reallocates assets and debts between the two of you. It does not rewrite the contracts either of you signed with a bank, a card issuer, or a mortgage servicer. The Consumer Financial Protection Bureau puts it plainly: “Divorce changes the relationship between spouses, but it doesn’t automatically change their relationship with creditors,” and “sending creditors a copy of your divorce decree doesn’t end your responsibility on a joint account.”

The practical consequences flow directly from that:

- Joint liability is full liability. On a joint account, each holder is responsible for the entire balance — not half. The CFPB states that “each account holder is responsible for the full amount of the balance,” and “the credit card company can seek to collect the amount due from either account holder.”

- The decree binds your ex, not the lender. A property settlement can order your former spouse to pay a debt, but the creditor “can still collect from anyone whose name appears as a borrower on the loan or debt.”

- Their late payments become your late payments. As long as your name is on the account, delinquencies report to your credit — even when the decree says the debt is “theirs.”

- You usually cannot just remove your name. To stop being responsible for future charges on a joint card, the CFPB’s guidance is that “you may have to close the account” — not simply drop your name while it stays open.

Our take: In our experience helping newly single buyers in Colorado Springs, the decree is a promise between exes, not a shield against creditors. Treat it as the starting point for cleanup, never the finish line. If a debt is “assigned” to your ex but still open in both names, assume it can hurt your score until it is refinanced out or closed.

How mortgage underwriters treat a debt assigned to your ex

Here is the good news for qualifying: if a debt was assigned to your ex-spouse by a court order, mortgage underwriters can often leave that monthly payment out of your debt-to-income (DTI) ratio — the calculation that decides how much house you can afford. The agencies call this a contingent liability.

Under the current Fannie Mae Selling Guide (B3-6-05, effective June 3, 2026), when a debt was “assigned to another party by court order (such as under a divorce decree or separation agreement)” and the creditor has not released you, “the lender is not required to count this contingent liability as part of the borrower’s recurring monthly debt obligations.” A copy of the court order documenting the assignment is required in the loan file.

But there is a critical catch that trips up borrowers who relied on the decree alone. Fannie Mae’s guide is explicit: “The lender cannot disregard the borrower’s payment history for the debt before its assignment.” In plain terms, the payment may drop out of your DTI going forward, but any late payments that already hit your report — before or after the divorce — are still visible to the underwriter and still weigh on your credit score. Excluding the payment from DTI does not erase the damage on the credit report.

FHA treats decree-assigned debt the same way at a high level. Under HUD Handbook 4000.1, when a debt on the credit report was assigned to another party by a divorce decree or court order and the creditor did not release the borrower, the contingent liability does not have to be included in the monthly debt, provided the lender obtains a copy of the decree or court order. A 2021 update to the handbook removed the earlier requirement to document 12 months of on-time payments by the responsible party specifically for decree-created contingent liabilities — though the court order itself is still required.

Freddie Mac aligns as well. Under Section 5401.2, and following Bulletin 2022-25 (effective December 7, 2022), Freddie Mac removed the requirement that the debt be secured in order to exclude it from your DTI when the obligation to pay has been assigned to another party by a documented court order. The monthly payment amount must be documented with a copy of the signed court order, separation agreement, and/or final divorce decree, or equivalent documentation.

Contrast that with a debt that is not assigned by a decree but is simply “being paid by someone else.” To exclude a non-mortgage debt someone else pays voluntarily, Fannie Mae requires “the most recent 12 months’ canceled checks (or bank statements) from the other party making the payments that document a 12-month payment history with no delinquent payments.” A single missed payment inside that window and the debt goes right back into your ratios. The decree route is cleaner precisely because it does not lean on your ex’s payment record — but it still leaves the credit-report scars in place.

Alimony and child support: income on one side, a bill on the other

Support payments cut both ways in a mortgage file, and which side you land on depends entirely on whether you receive or pay them.

If you receive support, it can count as qualifying income — but underwriters test durability first. Under Fannie Mae’s income rules (B3-3.4-02 and B3-3.1-09), the payments generally must be expected to continue for at least three years after the loan application, and you must document the amount and prior receipt with a copy of the signed court order, separation agreement, or final divorce decree, plus evidence of recent receipt (commonly the most recent six months). Support that ends in a year or two typically cannot be used to qualify, because it will not last the distance.

If you pay support, it is a monthly obligation. Fannie Mae’s B3-6-05 requires that alimony, child support, equalization, or separate maintenance payments be counted in your recurring debts when they continue for “more than ten months.” A copy of the divorce decree, separation agreement, court order, or equivalent documentation confirming the amount must be retained in the file.

There is one meaningful nuance for people who pay alimony (as opposed to child support). Fannie Mae gives the lender the option, for alimony, equalization, and separate maintenance obligations, “to reduce the qualifying income by the amount of the obligation in lieu of including it as a monthly payment.” Reducing income rather than adding a liability can produce a slightly stronger DTI in some scenarios, so it is worth asking your loan officer to model both.

| Support scenario | How the mortgage file treats it |

|---|---|

| You receive alimony or child support | May count as income if it will continue ~3+ years, documented by decree plus recent receipt history |

| You pay child support (>10 months left) | Counted as a monthly debt in your DTI |

| You pay alimony or separate maintenance (>10 months left) | Counted as a monthly debt, or the lender may instead reduce your qualifying income by that amount |

Removing your name: refinance, assumption, or closing the account

Because the decree does not release you, the only durable ways to get off a joint obligation are to change the underlying contract or end it. There are essentially four paths, and which one applies depends on the debt.

- Refinance the joint mortgage into your ex’s name. If your ex is keeping the marital home, a refinance replaces the old joint loan with a new loan in their name only — the cleanest way to remove your liability. Until that refinance closes, the old mortgage remains yours too, and a late payment on it can block your own approval.

- Loan assumption. Some government-backed loans (FHA, VA, USDA) can be assumable, letting your ex formally take over the existing mortgage and release you, subject to lender approval and their ability to qualify. Assumption is not automatic and not available on every loan — confirm with the servicer.

- Close the joint account. For credit cards and lines of credit, the practical move is to close the account, ideally at a zero balance, so no new charges accrue. Remember that closing an account with a balance still leaves both holders on the hook for that balance.

- Authorized-user removal. If you were only an authorized user (not a joint owner) on your ex’s card, you can ask the issuer to remove you, which generally takes the account off your credit report going forward. This is different from joint ownership, where removal usually is not possible without closing.

Our take: Do this in a deliberate order. Pull all three bureaus early, list every single joint account — mortgages, autos, cards, personal loans, even utilities — and get each liability either refinanced out or formally assigned before you shop for your new home. Do not rely on the decree alone to protect your score. We have seen approvals stall because an ex quietly missed a payment on a car loan the decree “gave” them; the borrower found out only when their own credit was pulled.

A practical order of operations before you apply

Sequencing matters more than most people expect. A clean paper trail turns a messy split into a straightforward file.

- Get your decree finalized and specific. Underwriters need documentation that clearly assigns each debt and states any support amounts and durations. Vague language creates problems.

- Pull all three credit bureaus. Scores and accounts can differ across Equifax, Experian, and TransUnion. Verify every joint tradeline appears the way you expect.

- Inventory joint debts and route each one. Refinance, assume, close, or assign — every joint account needs a plan, not a hope.

- Document support both ways. Keep the decree and proof of payments (received or paid). Six months of receipt history is a common threshold for using support as income.

- Dispute anything inaccurate promptly. If a late payment is genuinely an error, correcting it before you apply is far easier than mid-underwriting.

Timing is everything here. The earlier you separate the accounts, the more time any repaired credit has to mature before an underwriter looks at it — and the less exposure you carry to an ex’s missed payment.

Frequently asked questions

Does my divorce decree remove me from a joint mortgage or car loan? No. A decree allocates responsibility between you and your ex, but the lender was not a party to it. You remain liable to the creditor until the loan is refinanced, assumed, paid off, or you are formally released. The CFPB is explicit that sending a decree to a creditor does not end your responsibility on a joint account.

Can a mortgage underwriter ignore a debt the decree assigned to my ex? Often, yes. Fannie Mae, Freddie Mac, and FHA all allow a decree-assigned debt to be excluded from your DTI as a contingent liability when you provide the court order. But Fannie Mae also states the lender cannot disregard your payment history on that debt before it was assigned — so past late payments still affect your credit even if the payment drops out of your ratios. General, confirm current.

Will my ex’s late payments still hurt my credit after the divorce? Yes, as long as your name remains on the joint account. Delinquencies report to every borrower on the account regardless of what the decree says. This is the main reason to refinance or close joint accounts rather than trusting the decree to protect your score.

Can I use child support or alimony to qualify for a mortgage? Potentially. Support can count as qualifying income if it is expected to continue for roughly three years or more and you document the decree plus recent receipt (commonly six months). Support ending sooner generally cannot be used. General, confirm current.

If I pay child support, does it count against me? Yes. Under Fannie Mae’s guidance, child support with more than ten months remaining is counted as a monthly debt in your DTI. For alimony or separate maintenance, the lender may instead reduce your qualifying income by that amount. General, confirm current.

How do I actually get my name off a joint account? Refinance the loan into your ex’s name, pursue a formal loan assumption (available on some FHA, VA, or USDA loans with lender approval), or close a joint credit card — ideally at a zero balance. If you were only an authorized user, you can ask the issuer to remove you, which usually takes it off your report going forward.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, and this content is not endorsed by, HUD, the FHA, the VA, the USDA, or any government agency. Loan program guidelines, rates, figures, and thresholds referenced here are general and subject to change — confirm current requirements with a licensed loan officer for your specific situation. This article is educational and not financial, legal, or tax advice. Last updated: June 2026.

Related Posts