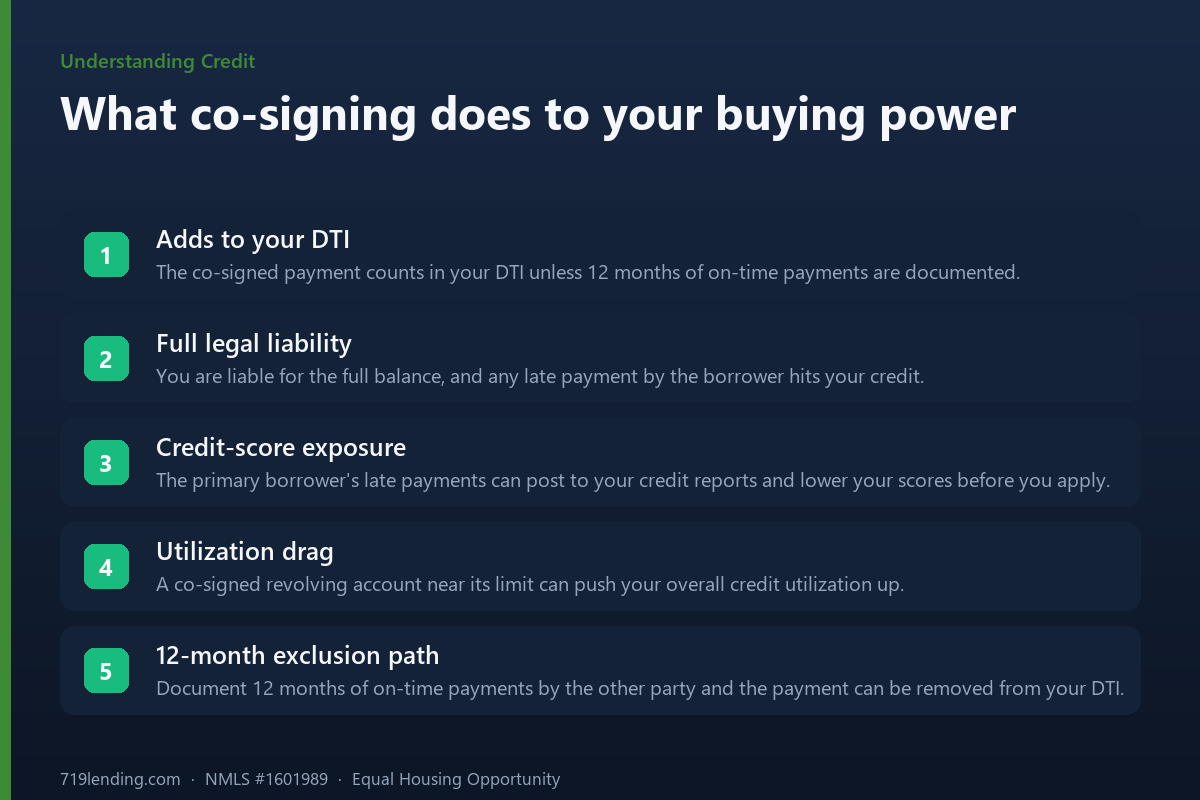

Co-signing a loan can count against your debt-to-income ratio and dent your credit before you buy a home. Here's how it works and how to clear it, per Fannie Mae, Freddie Mac, FHA and the CFPB.

Should You Pay Off Your Car Before Buying a House?

In most cases you should not drain your savings to pay off a car loan before buying a house — but there are specific situations where paying the loan down can meaningfully increase how much home you qualify for. The decision is not really about the car. It is about three competing levers: your debt-to-income ratio, your credit score, and the cash you have left after closing. Paying off a car helps one of those levers and can quietly hurt the other two. The right move depends on which lever is actually blocking your approval, and that is something to model with a loan officer before you write a check.

The three levers: DTI, credit score, and cash

Every dollar you put toward a car loan does three things at once, and they do not all pull in the same direction. Understanding each one is the difference between a smart pay-down and an expensive mistake.

- Debt-to-income ratio (DTI). Retiring the car payment removes it from your monthly obligations, which lowers your DTI and raises your buying power. This is the lever most people are thinking about.

- Credit score. Paying off and closing your only installment loan can slightly lower your score by reducing your credit mix and removing an active, on-time account. The effect is usually small and temporary — but it is the opposite of what most buyers expect.

- Cash. Money spent on the car is money not available for your down payment and reserves. For many buyers, cash is the binding constraint, and spending it to kill a payment can do more harm than good.

The Consumer Financial Protection Bureau defines DTI simply as all your monthly debt payments divided by your gross monthly income — “one way lenders measure your ability to manage the monthly payments to repay the money you plan to borrow.” A $500 car payment on $8,000 of gross monthly income adds roughly six percentage points to your DTI. Eliminating it can be the difference between an approval and a decline when you are near a program’s ceiling.

You may not need to pay the car off at all

Here is the rule most buyers never hear: mortgage guidelines let underwriters ignore installment debts that are almost paid off. If your car loan is close to the finish line, the payment may already be invisible to your DTI — no payoff required.

Fannie Mae’s Selling Guide B3-6-05, Monthly Debt Obligations (effective June 3, 2026) states that installment debt “must be considered part of the borrower’s recurring monthly debt obligations if there are more than ten monthly payments remaining.” Read the other way: an installment loan with ten or fewer monthly payments remaining can generally be excluded from your DTI — unless, in the guide’s words, it “significantly affects the borrower’s ability to meet their credit obligations.” Freddie Mac’s Seller/Servicer Guide reaches the same ten-payments-or-fewer result for conventional loans.

The agencies differ in the details, so the exact play depends on your loan type:

| Program | When a car payment can be excluded from DTI |

|---|---|

| Conventional (Fannie Mae / Freddie Mac) | Ten or fewer monthly payments remaining, if it does not significantly affect ability to pay. |

| FHA (HUD Handbook 4000.1) | Ten or fewer months remaining and the combined excluded payments total no more than 5% of gross monthly income. Prepaying the balance to reach the ten-month window is not permitted. |

The FHA condition is the strict one: you cannot make a lump-sum payment simply to shrink the remaining term into the exclusion window, and the payments you exclude cannot exceed 5% of gross monthly income. Note also that leases behave differently. Fannie Mae requires that “lease payments must be considered as recurring monthly debt obligations regardless of the number of months remaining on the lease,” because a lease that ends is typically replaced by another car obligation. If you lease rather than own, the ten-payment logic does not rescue you.

How paying off a car can hurt your credit score

It is counterintuitive, but paying off an installment loan can nudge your score down in the short run. According to myFICO’s breakdown of what is in your FICO Score, the score is built from five categories:

- Payment history — 35%

- Amounts owed — 30%

- Length of credit history — 15%

- Credit mix — 10%

- New credit — 10%

Credit mix is 10% of the score and rewards you for successfully managing different types of credit — revolving accounts like credit cards alongside installment accounts like an auto loan. myFICO notes that closing your only active installment loan can leave you with a less diverse mix, and lenders view a diverse, actively managed mix as lower risk. The effect is generally minor and temporary — myFICO also points out that it is not necessary to have one of every type of account to earn a good score — but in the weeks right before you lock a mortgage rate, even a small, temporary dip is poorly timed.

Our take: if your credit report shows the auto loan as your only installment account and your score is sitting near a pricing threshold, we would rather see you keep making the normal monthly payment through closing than pay it off and risk a mix-related dip at the worst possible moment. Talk to your loan officer about the timing before you act.

The cash lever: your down payment and reserves come first

This is where most “just pay off the car” advice falls apart. Every dollar you throw at the loan is a dollar removed from the two piles lenders care about most at the closing table: your down payment and your reserves.

Reserves are the cushion of liquid assets you have left after the loan closes. Fannie Mae’s Selling Guide measures reserves as the number of months of the qualifying payment — principal, interest, taxes, insurance, and any association dues (PITIA) — that you could cover from remaining assets after paying your down payment and closing costs. Drain that cushion to zero out a car loan, and you can trade a manageable monthly payment for a weaker, riskier file — sometimes weak enough to jeopardize the approval you were trying to protect.

Separately, the CFPB’s guide to building an emergency fund notes that the right amount to keep on hand depends on your situation — a useful starting point is the kind of unexpected expenses you have faced before and what they cost — and that even a modest cushion provides real financial security for the car repairs, medical bills, and income disruptions that do not stop coming just because you bought a house. New homeownership tends to add unexpected costs, not remove them. Emptying your account the month before you take on a mortgage runs directly against that guidance.

When paying down (not off) is the smart move

There is a middle path that captures the DTI benefit without the full cash hit. If DTI is genuinely the thing blocking your approval and you have surplus cash beyond a healthy down payment and reserves, paying the loan down to the exclusion threshold can remove the payment from your ratio for far less money than paying it off entirely.

The mechanics differ by program, which is exactly why you model it first:

- Conventional: paying the balance down to ten or fewer remaining payments can let the underwriter exclude the payment from DTI, so you spend only what it takes to reach that window rather than the whole balance.

- FHA: the pay-down-to-ten-payments trick does not work — HUD does not allow prepaying to reach the ten-month window, and the excluded payment must also fall within the 5%-of-gross-income limit. On FHA, plan around the rule rather than trying to engineer it.

Because a $500 car payment on $8,000 of gross monthly income is roughly six points of DTI, freeing it up can move real buying power — but only if the payment was the actual constraint. If your DTI already clears the program limit with room to spare, paying the car down buys you nothing and costs you reserves.

A simple way to decide

Before you touch the loan, walk through these questions with your loan officer, ideally with a live pre-approval scenario in front of you:

- Is DTI actually the blocker? If you already qualify comfortably, leave the car alone and keep your cash.

- How many payments are left? If it is ten or fewer, the payment may already be excludable on a conventional loan — confirm before spending a dollar.

- Is this your only installment account? If so, weigh the small, temporary credit-mix risk of closing it right before you lock.

- What happens to your reserves? Run the numbers with the car paid off and paid down, and check that you still have a healthy cushion after closing.

- Would paying down beat paying off? On conventional loans, hitting the ten-payment window can deliver the DTI win for a fraction of the cash.

The best answer is almost never a reflex. It is the output of a five-minute conversation with someone who can see your full file. A Colorado Springs mortgage broker can model both scenarios side by side and tell you which lever is really holding you back — before you spend money you may need at the closing table.

Frequently asked questions

Will paying off my car help me qualify for a bigger mortgage? It can, because removing the payment lowers your debt-to-income ratio and frees up borrowing capacity. But it only helps if DTI is the constraint. If you already qualify and the payoff drains your down payment or reserves, it can hurt your file more than the lower DTI helps.

Does paying off a car loan lower my credit score? Sometimes, slightly and temporarily. myFICO notes that paying off your only active installment loan can reduce your credit mix, which is about 10% of your FICO Score. The dip is usually minor and short-lived, but the timing right before a mortgage matters.

Do I have to pay the car off completely to remove it from my DTI? Not always. Fannie Mae and Freddie Mac generally allow underwriters to exclude an installment loan with ten or fewer monthly payments remaining. FHA also requires the excluded payments to total no more than 5% of gross monthly income and does not allow prepaying to reach that window. Confirm the current rules for your program with your lender.

Should I use my down payment money to pay off my car? Usually not. Your down payment and reserves are what lenders weigh most heavily at closing, and the CFPB advises keeping an emergency cushion sized to your own situation. Spending that cash to eliminate a monthly payment can weaken your approval rather than strengthen it.

Is it better to pay the car down instead of paying it off? On a conventional loan, paying down to ten or fewer remaining payments can remove the payment from your DTI for far less cash than paying off the full balance — if DTI is your blocker and you have surplus cash. On FHA this does not work, because prepaying to reach the ten-month window is not permitted.

What if I lease my car instead of financing it? Lease payments are treated differently. Fannie Mae requires lease payments to count as recurring monthly debt regardless of how many months remain, because an expiring lease is usually replaced by another car obligation. The ten-payment exclusion does not apply to leases.

719 Lending, NMLS #1601989. Equal Housing Opportunity. 719 Lending is not affiliated with, endorsed by, or acting on behalf of the FHA, HUD, VA, USDA, or any government agency. Guidelines, ratios, thresholds, and figures referenced here are general and subject to change — confirm the current requirements for your loan program with a licensed loan officer. This article is educational and not a commitment to lend, credit decision, or promise of any specific credit-score change, approval, or rate. Last updated: June 2026.

Related Posts